Renewable supply chain presents investment opportunities in seven Asian markets that could exceed US$1.1 trillion by 2050

Solar and offshore wind investments can unlock the localization of manufacturing and job opportunities, benefiting economies and energy consumers while supporting decarbonization targets

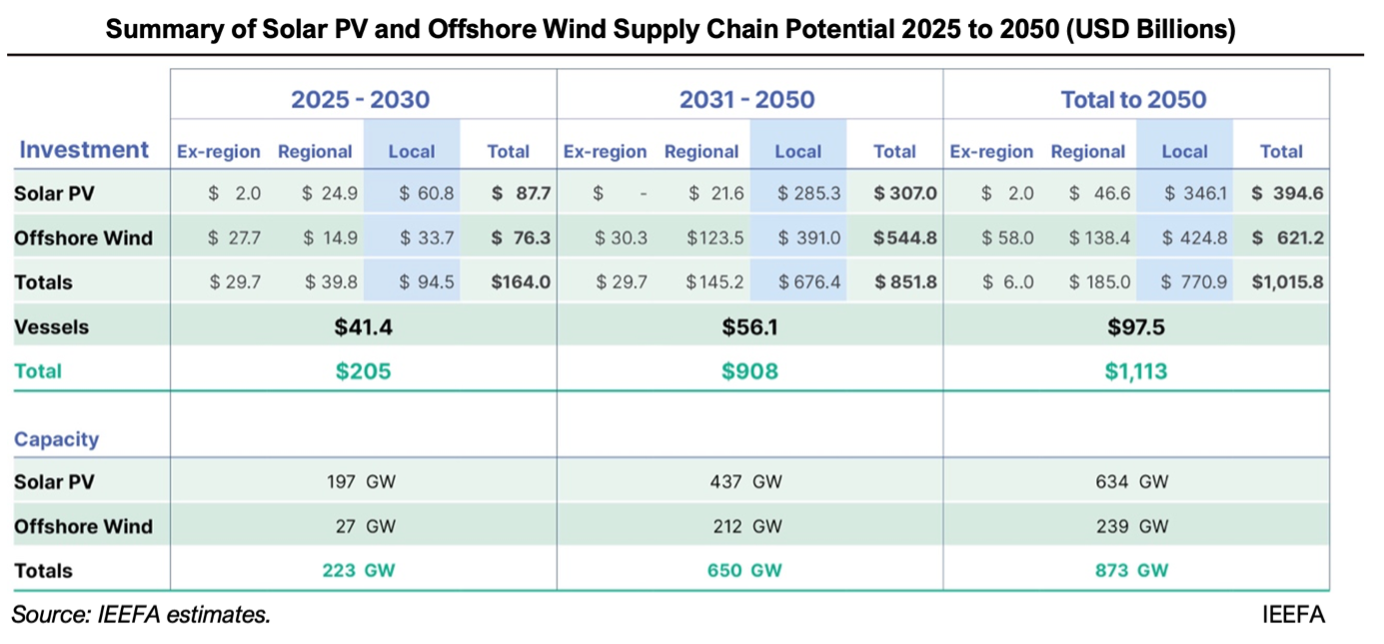

June 27, 2024 (IEEFA Asia): The investment potential for solar and offshore wind power project supply chains exceeds US$1.1 trillion through 2050, with the capacity to generate 873 gigawatts (GW) of clean energy, according to a new report from the Institute for Energy Economics and Financial Analysis (IEEFA).

“This report highlights the here-and-now opportunity to capitalize on the renewable energy supply chain,” says Grant Hauber, IEEFA’s Strategic Energy Finance Advisor, Asia. “Solar energy offers immediate investment benefits to the Asia Pacific, while the advantages of participating in the offshore wind supply chain will develop over the next several years.”

The report focuses on seven Asian markets: Japan, South Korea, Malaysia, Taiwan, Vietnam, Philippines, and Indonesia. IEEFA calculates that up to 2050, solar PV plans aim to achieve 634 GW of capacity, requiring an investment of US$394 billion, with US$346 billion of that amount potentially to be spent on local supply chains. Offshore wind represents a US$621 billion opportunity to deliver 239 GW of capacity, with US$425 billion expected to be localized.

Additionally, there is an opportunity in the maritime sector worth US$72 to US$97 billion to build offshore wind installation and service vessels, with almost all this investment expected to be sourced regionally.

“The report maps out each element in the project supply chain, quantifies the capital investment potential, and aims to encourage more ambitious and long-term policies, which helps investors and policymakers appreciate the size of the opportunity,” says Hauber.

Looking beyond panels and turbines

In addition to promising low-cost energy, there are opportunities to localize large proportions of the solar and offshore wind supply chains required for fully operational power generation projects.

“A key message for policymakers and industrialists is that you do not need to make solar PV modules or wind turbines to realize huge domestic manufacturing and investment benefits,” says Hauber.

According to the report, non-panel and non-turbine spending will account for at least 75% of total investment through 2050, representing a $770 billion opportunity for domestic industries over the next 25 years.

“There are materials, components, infrastructure, logistics, and services that can provide significant value to the domestic economy over sustained periods and potentially marketed regionally and beyond,” says Hauber.

China currently dominates the global supply chain for solar PV panel manufacturing, delivering nearly 85% of global demand at costs that are unlikely to be matched for at least the rest of this decade. Outside of China, instead of producing PV modules, countries can direct domestic investment towards other project-level components that make up completed solar farms.

Hauber emphasizes the concept of the balance of system (BOS), which comprises all costs and components beyond the solar panel. IEEFA calculates that BOS investments constitute the majority of PV farm costs, which, depending on the market, range from 55% to 75% of total project expenditure.

“Within the solar PV project supply chain, nearly all the project development and financing costs are locally incurred and potentially half or more of the BOS costs could be domestically sourced,” says Hauber.

Meanwhile, offshore wind resources in Asia are abundant, high-quality, and predictable. The region's traditional maritime economies possess inherent advantages in shipbuilding, steel fabrications, marine maintenance, and offshore services, making them well-suited for large-scale offshore wind projects.

“The wind energy capacity available to nearly every country in the Asia Pacific is greater than their current total installed capacity from all sources of generation,” says Hauber. “Wind farms are becoming competitive enough to undercut imported natural gas and coal, even in markets where those prices are subsidized and in the absence of carbon pricing.”

Shipbuilding for offshore wind presents a standalone opportunity worth up to US$97 billion, with most of that investment needed in the near term. Hauber highlights that global wind service fleet additions have not kept pace with the increasing size of turbines and the expanding scale of wind farms.

The global push for offshore wind farms creates substantial opportunities for shipyards throughout the Asia Pacific to meet these growing demands. Currently, there are only a limited number of niche shipyards constructing these vessels, mainly in Norway and China. There is a particular need for specialized wind turbine installation vessels, as only a few can install the largest, next-generation turbines.

Currently, only about 20% of wind farm inputs are locally sourced in the region, but with sustained demand, this could grow to between 66% and 80% of the total investment value. Hauber suggests that the combined offshore wind farm and specialty vessel market represents an investment opportunity of around US$878 billion through 2050.

Untapped potential

The report focuses on currently announced capacity targets for solar and offshore wind, but the market’s potential could be much larger.

If the capital costs for solar PV and offshore wind continue to fall as predicted, these technologies will offer the lowest levelized costs of electricity on each national grid. With such attractive energy costs, capacity targets are likely to expand to capture the economic benefits.

Currently, most Asia Pacific countries appear to be underestimating this opportunity. The report highlights that, despite nearly every country in the region having world-class solar and wind resources, planned renewable capacity additions remain a limited share of electricity supply.

For instance, Indonesia has one of the smallest solar bases in Asia, with the least aggressive additions relative to its available resources. Japan, despite having one of the best wind resources globally, has very modest offshore wind program targets, aiming for less than 5% of total demand by 2050.

According to Hauber, policy alignment is now needed to help countries realize this potential. Focusing on maximizing low-cost capacity additions at scale will create recurring demand, allowing local industries to capitalize on the solar and offshore wind supply chain.

“Ultimately, domestic businesses benefit from higher development volume, consumers benefit from the lowest long-run marginal cost of electricity, and the government benefits from both these wins and significant progress toward decarbonization targets,” says Hauber.

Read the report: The Asia Pacific Renewable Supply Chain Opportunity

Read the factsheet: Race for the trillion-dollar renewables investment opportunities in the Asia Pacific

Author contact: Grant Hauber ([email protected])

Media contact: Alex Yu ([email protected])

About IEEFA:

The Institute for Energy Economics and Financial Analysis (IEEFA) examines issues related to energy markets, trends and policies. The Institute’s mission is to accelerate the transition to a diverse, sustainable and profitable energy economy. (www.ieefa.org)