Indian States' Electricity Transition (SET) 2026

Download Full Report

View Press Release

Key Findings

SET 2026 underscores that progress in individual dimensions does not automatically translate into a system-wide electricity transition. However, across the 21 states assessed, advancements have been made on multiple fronts, even as the pace and focus vary across key areas of evaluation.

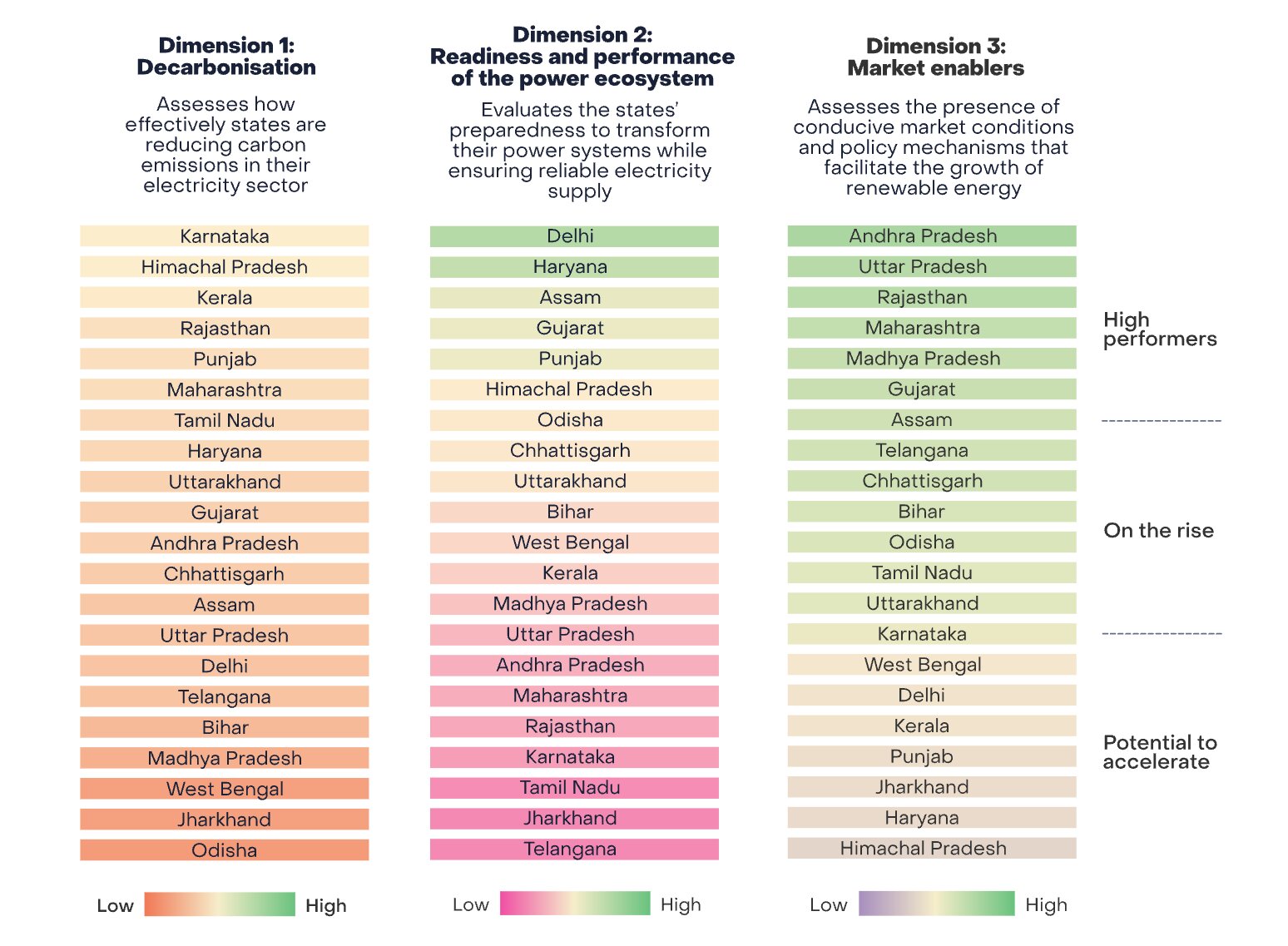

Karnataka, Himachal Pradesh and Kerala showcase consistent leadership in the decarbonisation dimension of the SET 2026 evaluation, emerging as strong performers. This dimension assesses states’ progress in shifting to renewable electricity, improving energy efficiency, and decoupling growth from emissions. Tamil Nadu, Maharashtra and Rajasthan also show progress through energy efficiency interventions.

Delhi and Haryana continue to perform strongly in terms of how prepared and well-functioning their power ecosystems are, driven by factors like robust distributed solar adoption, reliable power supply, and relatively sound DISCOM performance. Chhattisgarh and Bihar stand out due to improvements in their DISCOM performance.

Andhra Pradesh, Uttar Pradesh and Rajasthan do well under market enablers, regulatory initiatives that accelerate renewable energy adoption, such as up-to-date policies, adoption of green tariffs and green open access mechanism, and progress on solar-hour-aligned time-of-day (ToD) tariffs. Bihar and Assam, too, stand out in this dimension, driven by improvement in their electric vehicle ecosystem, availability of attractive green tariffs, introduction of solar-hour-aligned ToD tariffs and updates to their renewable energy policies in 2025.

Executive summary

India’s electricity demand continues to rise rapidly, driven by sustained economic growth, urbanisation and the electrification of transport, industry and emerging digital infrastructure. With the power sector accounting for nearly half of India’s total carbon dioxide emissions, accelerating the transition to clean electricity is critical to achieving the climate objectives laid out in India’s National Determined Contribution (NDCs). Beyond emissions reduction, this transition will also offer other benefits, such as increased affordability and energy security. And while national policies set the overall direction, state governments ultimately shape outcomes through power procurement choices, performance of distribution companies (DISCOMs), market enablers and grid preparedness.

The transition, however, is unfolding differently across states, shaped by variations in resource endowments, development pathways, and institutional capacities. While some states are already leading in renewable energy deployment and grid readiness, others are building momentum, presenting significant opportunities for accelerated progress through targeted, state-specific policy interventions.

This third edition of the State Electricity Transition (SET) 2026 report evaluates 21 Indian states across three key dimensions: ‘Decarbonisation’; ‘readiness and performance of the power ecosystem’; and ‘market enablers’.

Dimension 1, decarbonisation, assesses states’ progress in shifting to renewable electricity and decoupling economic growth from emissions. The second dimension looks at the readiness and performance of states’ power ecosystem, examining factors such as the uptake of distributed solar, the reliability of power supply, and the health of DISCOMs. The third dimension, market enablers, evaluates state-level initiatives that facilitate the adoption of electric vehicles (EV) and green hydrogen, as well as measures such as green tariffs, green energy open access, energy storage deployment, and solar-hour-aligned time-of-day (ToD) tariffs to accelerate the transition to renewable energy.

Building on the 2023 and 2024 editions, the 2026 assessment incorporates recent developments, emerging trends, and stakeholder consultations to reflect on-ground realities. The report does not consider socio-economic or Just Transition considerations such as livelihoods, fiscal dependence, or workforce impacts, which fall beyond the scope of this edition. Table 1 in the methodology section outlines the rationale for the selected dimensions and parameters, while Figure 2 presents the macro performance of states based on their dimension-level performance.

A dimension-level analysis highlights states that have demonstrated consistent progress, as well as those facing structural challenges in advancing the electricity transition. A cross-dimensional analysis further shows that progress in one area does not automatically translate into a comprehensive, system-wide transition. While all 21 states assessed have made progress across multiple fronts, the pace and depth vary significantly across dimensions. The sections below highlight key insights emerging from both dimension-wise and cross-dimensional assessment.

Dimension-level insights:

- Decarbonisation: Karnataka, Himachal Pradesh and Kerala have showcased consistent leadership in the decarbonisation dimension of the SET 2026 and SET 2024 analysis, emerging as strong performers. Karnataka continued to lead, supported by relatively lower power sector emissions intensity and a renewable energy share of around 37% in its power procurement mix. Hydropower-dominated Himachal Pradesh recorded the highest renewable share (~65%) and the lowest emissions intensity, though utilisation of its renewable potential remained moderate and energy efficiency performance presented scope for strengthening. Kerala’s performance was driven by low emissions intensity and steady renewable potential utilisation. Tamil Nadu, Maharashtra and Rajasthan also showed progress, particularly through strengthened energy efficiency interventions.

- Readiness and performance of the power ecosystem: Delhi and Haryana continued to perform strongly in terms of their preparedness and overall well-functioning power ecosystems. The states’ progress was supported by robust distributed solar adoption (76% and 73%, respectively, of total renewable installed capacity), alongside reliable power supply and relatively sound DISCOM performance. Chhattisgarh and Bihar stood out due to improvements in their DISCOM performance since the SET 2024 analysis, reflecting strengthened operational efficiency in the distribution segment.

- Market enablers: Andhra Pradesh, Uttar Pradesh and Rajasthan did well under market enablers, reflecting regulatory initiatives that accelerated renewable energy adoption. Their performance was supported by updated renewable energy policies, adoption of green tariffs and green open access mechanisms, and progress on solar-hour-aligned time-of-day (ToD) tariffs. Uttar Pradesh demonstrated strong momentum in EV deployment, while Andhra Pradesh and Rajasthan also made moderate progress in this area. Bihar and Assam stood out in this dimension as well, driven by improvement in their EV ecosystem, availability of attractive green tariffs, introduction of solar-hour-aligned ToD tariffs, and renewable energy policy updates in 2025.

The figure below summarises where the states stand in terms of their progress across each dimension.

Figure 1: Dimension-level performance of 21 states

A summary of cross-dimensional insights:

- Some states emerged as leaders in India’s electric transition story, performing strongly in two of the three dimensions. These included Maharashtra, Rajasthan, Gujarat, Assam, Punjab and Himachal Pradesh.

Maharashtra and Rajasthan did well under dimension 1 and dimension 3. However, there remained scope to strengthen the readiness and performance of their power ecosystem (dimension 2), reflecting limitations in DISCOM performance, low short-term market participation, and limited uptake of distributed solar (off grid + rooftop solar + solar pumps) and smart meters. Gujarat and Assam did well across dimensions 2 and 3, but their performance under dimension 1 remained moderate, with Gujarat utilising only 15% of its renewable potential and Assam adding limited renewable capacity over the past five years, constraining the share of renewables in their power procurement mix. Meanwhile, Punjab, and Himachal Pradesh performed strongly in dimensions 1 and 2, but trailed in dimension 3 because of slow adoption of EVs, absence of solar hours aligned ToD tariffs, limited green hydrogen uptake and lack of energy storage additions. Collectively, these gaps constrained their ability to unlock a comprehensive clean electricity transition.

Figure 2: Macro-level performance of 21 states across electricity transition dimensions

- Another group of states showed progress in a single dimension. These included Karnataka, Tamil Nadu, Kerala, Delhi, Uttar Pradesh, and Andhra Pradesh, among others.

- Karnataka, Tamil Nadu, and Kerala demonstrated strong performance in dimension 1 with good energy efficiency interventions and lower emissions intensity. Karnataka led in dimension 1 with low power sector emission intensity, strong SEEI 2024 performance, and good renewable energy share (~37%). The states will now need to address the gaps in their grid readiness, DISCOM health, and market-enabling conditions. Delhi, Odisha, Haryana did well under dimension 2 with good DISCOM health and lower power supply shortage. Delhi remained a high performer under dimension 2, driven by zero power shortage, distributed solar adoption, with 304MW of distributed solar capacity installed as of March 2025, accounting for nearly 97% of its total solar capacity, and strong DISCOM performance. Its weak performance in dimensions 1 and 3 was due to low renewable energy capacity addition, low renewable energy share in procurement mix, limited uptake of ToD tariffs and nascent energy storage deployment. Uttar Pradesh, Madhya Pradesh, Andhra Pradesh showed advancement under market enablers with policy mechanisms in place, green hydrogen progress, and good EV adoption. Andhra Pradesh led in dimension 3 with its integrated clean energy policy, progress in green hydrogen, and 1,440MW of pumped hydro storage capacity, as well as solar-hour-aligned ToD tariffs. These states are yet to translate these into robust renewable shares or strong system performance.

- Chhattisgarh, Uttarakhand and Bihar were among the states that exhibited moderate performance across dimensions. Chhattisgarh’s moderate performance was down to its low renewable procurement (10% in FY2024) and large untapped renewable potential (~92%); low short-term market participation; limited distributed solar uptake (498 megawatt [MW]); and slow smart meter deployment. Meanwhile, Uttarakhand’s strong hydropower base supported a high renewable procurement share (44% in FY2024) and low emissions intensity, even as 84% of its renewable potential remained untapped. Its energy efficiency progress was weak, decentralised solar adoption minimal and metering slow. Bihar performed moderately on dimensions 2 and 3 but lagged in dimension 1, having used only 3% of its renewable potential and sourcing 18% of procurement from renewables. Bihar’s progress, though, was visible in smart metering (78% under the central government’s Revamped Distribution Sector Scheme [RDSS]), implementation of ToD tariffs, and EV uptake (8% in FY2025), even though shortages (0.4% in FY2025), low power market activity and non-operational storage persisted.

- West Bengal, Telangana and Jharkhand remained in the early stages of transitioning and required foundational interventions, including stronger institutions, improved DISCOM finances, updated planning frameworks and clear long-term policy signals. West Bengal’s renewable share was only ~7% of procurement in FY2024 with very low distributed solar and smart metering uptake. Telangana recorded modest renewable energy share in its procurement mix (14% in FY2024), low utilisation of renewable potential (<10% as of March 2025) and weak DISCOM performance. Jharkhand recorded low renewable energy penetration (~8%), minimal market participation and structural challenges in DISCOM performance and EV adoption.

Evidence from across dimensions highlights that accelerating India’s electricity transition will require coordinated national and state-level actions, with targeted, dimension-specific interventions to address gaps in the areas where individual states show slower progress.

Related Content