Japan’s grid-scale BESS market: Turning market hype into reality

Key Findings

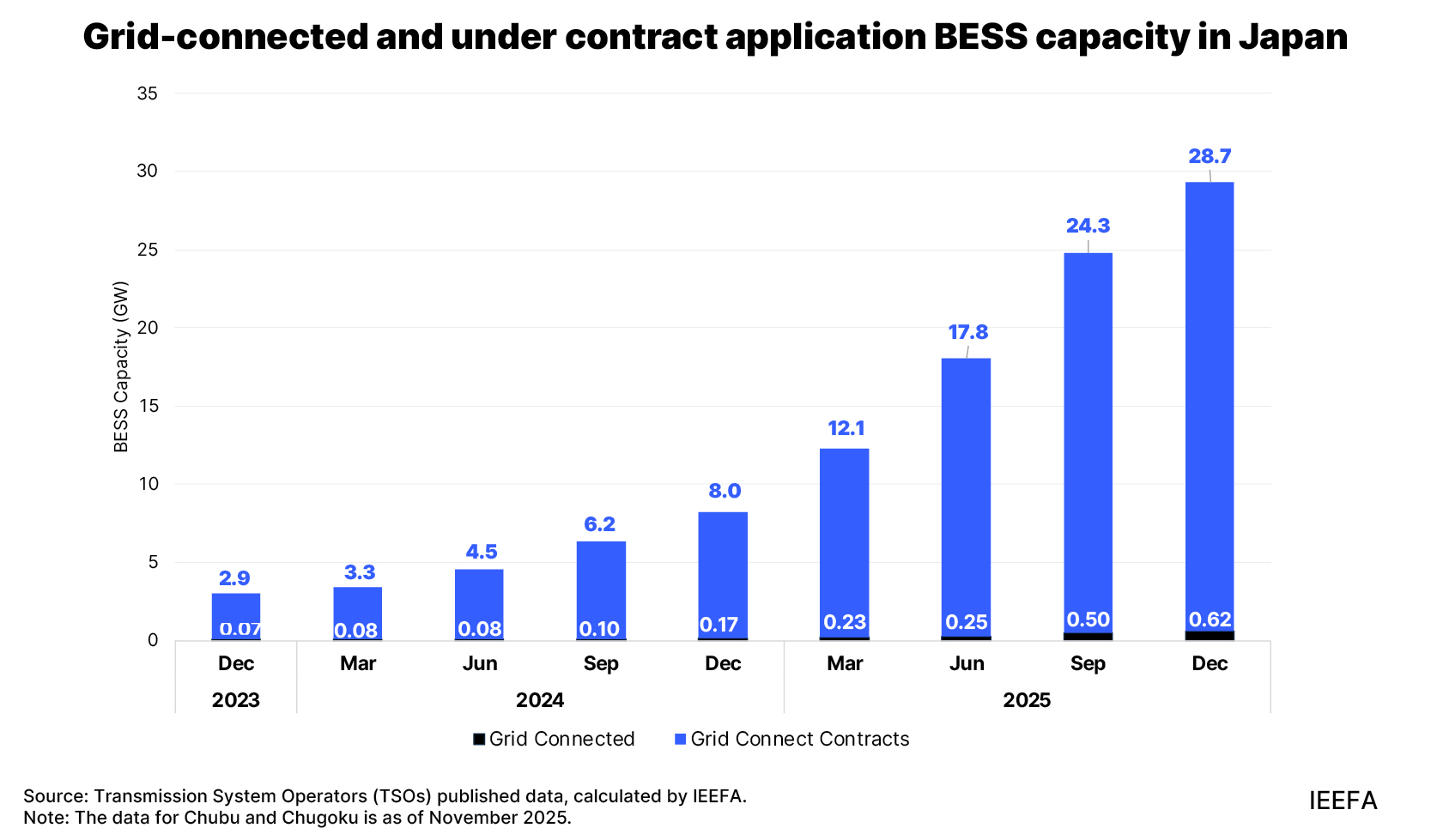

Japan’s growth in Battery Energy Storage Systems (BESS) reflects strong investor enthusiasm, but physical deployment remains minimal. BESS project applications have surged from 70 gigawatts (GW) to 170.8GW since mid-2024, yet only 0.62GW is connected, revealing a significant gap between project interest and system integration.

Grid connection bottlenecks and policy instability are the primary barriers to BESS implementation. Speculative grid applications, firm charging-side requirements, slow interconnection reforms, and shifting auction volumes are constraining deployment and undermining revenue certainty.

BESS costs in Japan remain structurally high, and domestic supply chain policies may influence long-term competitiveness. Battery system costs in the country are 2.5–3 times higher than global benchmarks, and local content rules combined with domestic manufacturing subsidies could shape future cost trajectories.

Japan’s grid-scale Battery Energy Storage System (BESS) market is poised for rapid growth, driven by policy reforms, falling prices, and access to multiple revenue streams from wholesale, balancing, and capacity markets. However, despite strong investor interest over the last two years, actual project implementation remains limited due to grid connection barriers and regulatory adjustments undermining financial certainty.

BESS technologies are critical for grid stability and renewable energy integration, as the country aims to achieve 40–50% renewable power generation by 2040. Deployment will depend on addressing grid connection barriers, strengthening market design, and lowering long-term costs.

BESS pipeline growth and its drivers

Applications to connect standalone BESS projects to Japan’s transmission and distribution grids have increased from 70 gigawatts (GW) in mid-2024 to 170.8GW by the end of 2025. This surge has placed a substantial burden on system operators to evaluate the high volume of proposals. Approximately 17% of the total (28.7GW) have been awarded grid connection contracts — a 10-fold increase since the start of 2024.

Yet just 0.62GW of BESS capacity, up from 0.07GW in early 2024, has been physically connected to the national grid, according to an analysis of the country’s 10 Transmission System Operators (TSOs) by the Institute for Energy Economics and Financial Analysis (IEEFA).

Government subsidies introduced since 2021 have been a key driver of investor interest in BESS projects. Japan’s Ministry of Economy, Trade and Industry (METI) awards a federal subsidy covering 50% of installation costs for battery systems above 10 megawatts (MW) with discharge times of less than six hours, and 66% of costs for systems with discharge times exceeding six hours. In financial year (FY) 2024, 27 grid-scale projects received JPY34.6 billion (USD226 million), with around JPY40 billion (USD262 million) budgeted for FY2025.

The Tokyo Metropolitan Government also provides subsidies of up to two-thirds of installation costs (capped at JPY2 billion per project), with a total allocation of JPY13 billion (USD85 million) for FY2025.

In 2022, Japan legally classified BESS projects exceeding 10MW as “power generation businesses”, enabling them to participate in wholesale, ancillary services, and capacity markets. This change enabled revenue stacking and improved project bankability.

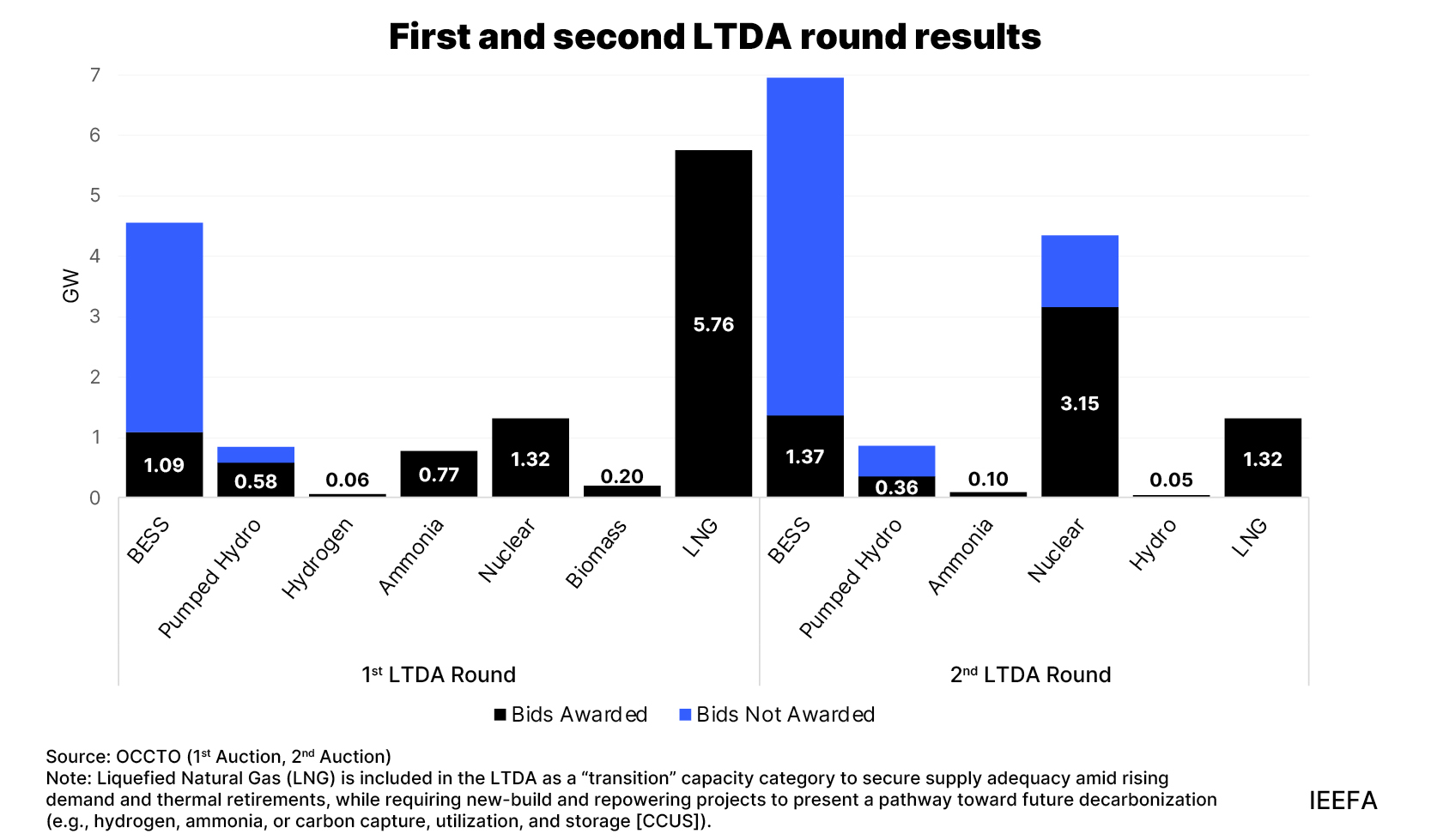

In 2023, Japan launched the Long-Term Decarbonization Electricity Capacity Auction (LTDA), which offers 20-year fixed revenue contracts on a pay-as-bid basis. BESS projects secured 1.1GW in the first round and 1.3GW in the second, with the third round ongoing as of February 2026.

Starting from the third round, the LTDA stipulates that no more than 30% of awarded battery capacity use cells manufactured in any single foreign country. In both the first and second auction rounds, BESS was the most oversubscribed technology.

Barriers to BESS project implementation

Although recent government reforms have stimulated commercial interest in BESS investments, the limited volume of physically connected capacity remains a key concern.

Grid connection remains the primary bottleneck. The capacity under study is nearly 300 times greater than the realized deployment, while contracted capacity is almost 50 times larger. In FY2024, BESS projects accounted for 9,544 of 14,391 grid connection study applications (66%), rising to approximately 83% in FY2025.

Japan’s interconnection framework has historically operated on a first-come, first-served basis with limited upfront screening. Developers were not required to demonstrate full site control or financial readiness before submitting grid connection applications, which may have encouraged speculative proposals.

Participation in government support schemes, including the LTDA, requires proof that bidders have applied for grid connection, which adds an incentive to apply early. Although METI began tightening requirements in January 2026 — introducing mandatory proof of land rights and higher financial security deposits — these reforms are still being phased in.

Moreover, BESS charging requires fixed, “firm” allocations of transmission capacity to alleviate peak-time congestion, which takes longer to secure than non-firm discharging. METI has introduced interim measures to specify prearranged charging restrictions and expedite interconnections. However, establishing a comprehensive non-firm charging framework will require longer-term system upgrades.

Competition in Japan’s ancillary services market has remained weak, partly due to limited BESS connections. While the lack of competition has proven lucrative for early BESS entrants, frequent market design changes have created revenue uncertainty for asset owners and lessees operating under tolling agreements.

The LTDA framework is also evolving. While batteries secured 1.1GW and 1.3GW in the first two auction rounds, the third round will procure a combined 0.8GW across battery storage, pumped hydro, and long-duration storage. Meanwhile, procurement allocations for decarbonized thermal power (0.5GW) and nuclear safety investments (1.5GW) will increase, reducing the share of capacity available to BESS and intensifying competition within the storage segment.

High battery costs in Japan compared to other markets present an additional challenge for new investment. Although limited competition in the balancing market has ensured short payback periods for BESS assets, costs remain 2.5–3 times higher than global benchmarks. Since 2010, global utility-scale battery costs have dropped by 93% to approximately USD192 per kilowatt-hour (kWh) in 2024. In Japan, however, projects averaged around JPY68,000/kWh (USD433/kWh) in FY2024.

Japan is targeting approximately 24 gigawatt-hours (GWh) of domestic battery production capacity by 2030 to strengthen geopolitical and economic security. However, domestically manufactured systems currently carry higher upfront costs, which could compress arbitrage-driven margins and affect overall project economics.

Realizing Japan's BESS potential

Looking ahead, several factors will be critical for ensuring that Japan’s BESS market hype becomes reality. First, timely reviews of grid applications will be necessary and depend on government efforts to reduce speculative proposals, strengthen pre-screening qualifications, and standardize fast-track grid connection procedures.

Rapid grid connections could stimulate competition and put downward pressure on balancing market prices. Currently, frequent changes to market design have complicated project bankability. Future LTDA reforms should aim to capitalize on high investor interest rather than constricting opportunities for BESS projects.

Finally, the trajectory of BESS costs in Japan will depend on the balance between demand and supply-side reforms. Subsidies for domestic manufacturing and local content requirements may lead to longer-term cost reductions but could restrict access to lower-cost foreign equipment in the near term.

While Japan’s grid-scale BESS market has demonstrated significant potential over the last two years, the focus should now shift to turning that potential into long-term implementation.

Related Content