CalSTRS trims fossil fuel holdings to mitigate climate risk

Key Findings

The California State Teachers’ Retirement System is reducing its exposure to fossil fuels.

The fund has moved $30 billion into a low-carbon public equity portfolio, highlighting the maturity of such investment strategies.

This move is in line with growing evidence of the financial risk facing the most carbon-intensive investments and occurs alongside other steps to protect the fund from climate risk.

A more ambitious approach is needed to mitigate future risks caused by climate change.

One of the nation’s largest pension funds is reducing its exposure to the fossil fuel industry. The move, which is part of a broader program to defend long-term portfolio value against the financial risks of climate change, provides yet more evidence that underweighting the fossil fuel sector is consistent with broadly diversified, growth-oriented investment strategies.

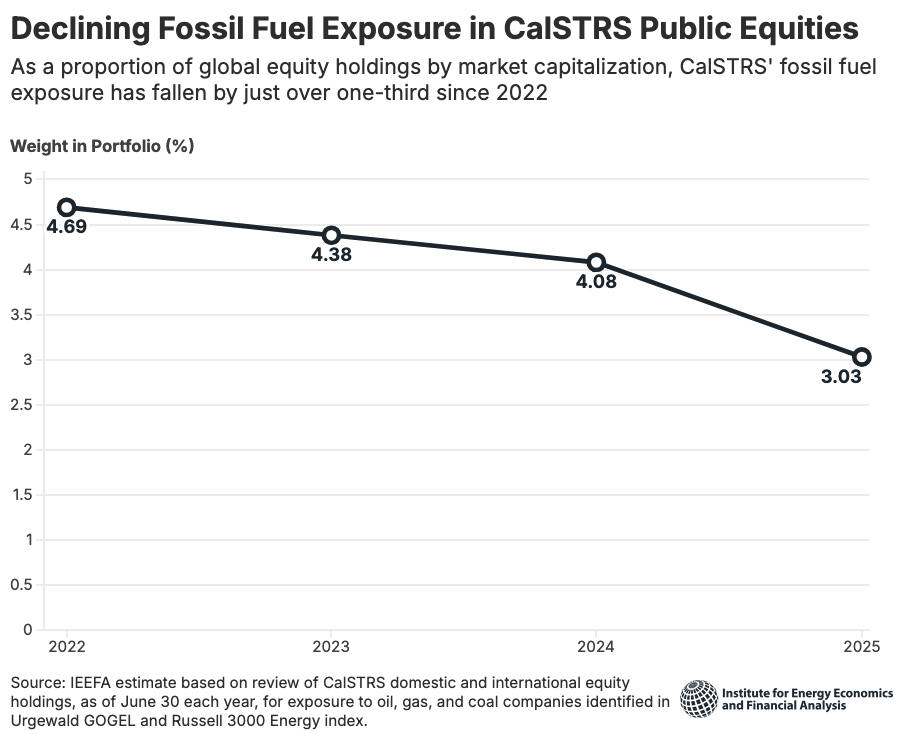

The weight of the traditional energy sector in the California State Teachers' Retirement System (CalSTRS) public equity portfolio has fallen by one-third, from 4.7% in 2022 to about 3% in 2025, according to an estimate by the Institute for Energy Economics and Financial Analysis (IEEFA).

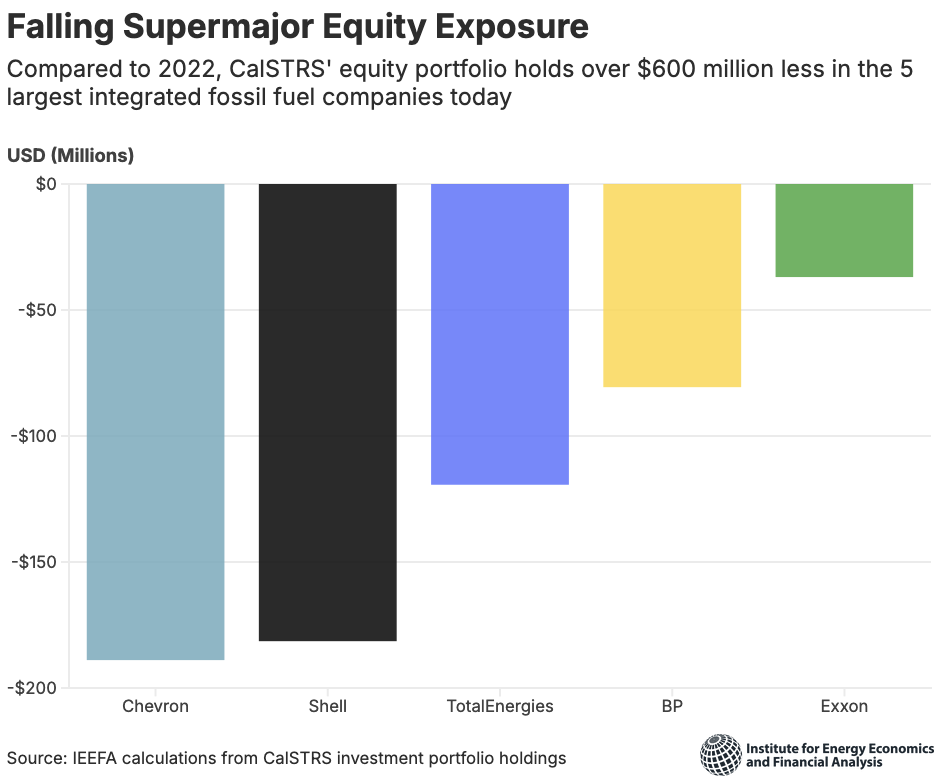

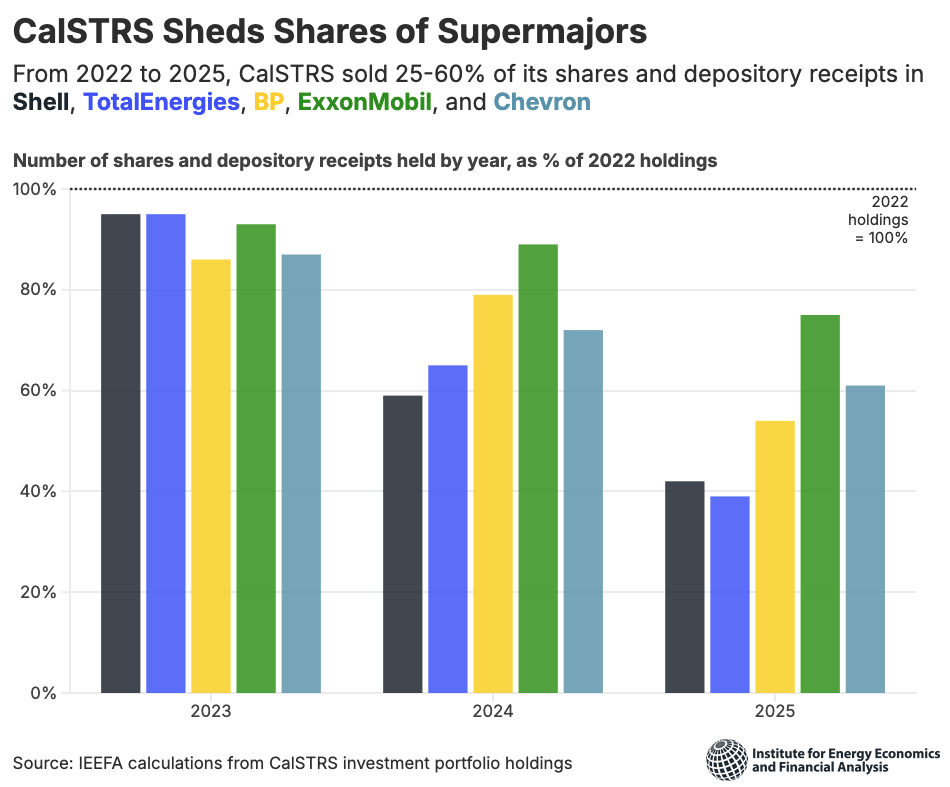

The change reflects an outright decline of about $600 million in exposure to the five largest integrated oil and gas companies, or “supermajors”—ExxonMobil, Chevron, Shell, BP, and TotalEnergies. CalSTRS's holdings of shares and depository receipts of each company declined by 25% to 60%, and holdings in the sector fell by about $750 million during the four-year period. Public equities are CalSTRS’s largest allocation and grew from $116 billion to $151 billion in that time, representing approximately 40% of the fund’s total portfolio.

These are significant shifts at one of the world’s largest institutional investors. They stem from CalSTRS decisions that have led to more than $30 billion flowing into a low-carbon passive public equity strategy, and are supported by the fossil fuel sector’s volatile stock market performance and clouded outlook.

The path to the CalSTRS decision

CalSTRS has sparred with advocates over its climate commitments in recent years, including over a 2022 bill in the California Legislature that would have mandated a 2030 phaseout of fossil fuel holdings. The pension fund warned that a shift away from oil and gas could adversely affect investment returns and prevent it from advancing low-carbon business models through shareholder engagement. Advocates of the legislation said it would be imprudent to rely on hydrocarbon producers to drive decarbonization and that long-term exposure would itself create substantive financial risks for the fund.

Yet the CalSTRS portfolio is evolving. Later in 2022, CalSTRS investment staff recommended that the investment committee move 20% of its public equity portfolio to track the MSCI ACWI Low Carbon Target Index. The Low Carbon Target Index (LCTI) is a variant of the fund’s global equity benchmark. It seeks to minimize exposure to carbon emissions and fossil fuel reserves while retaining broad exposure to global equities and limiting tracking error. The index underweights fossil fuels by about 50% relative to the ACWI IMI and excludes the integrated oil “supermajors.”

Some of the decrease in CalSTRS’ fossil fuel exposure is just a reflection of the fossil fuel industry’s broader slippage in global markets over the period. Its decrease, however, has outpaced the market, suggesting that the lower-carbon strategy is translating into portfolio-level decisions. The LCTI’s lower weighting of fossil fuels is likely to be a major contributor to this reduction in exposure, although the holdings of active public equity managers could have also played a small role.

The index’s recommendation and approval followed a deliberative process. CalSTRS investment staff reviewed a range of lower-carbon indexes. After examining fee structures, historical returns, tracking errors, reduction of financed emissions, and implementation details, they determined that the LCTI fit within the fund’s preexisting investment strategy. CalSTRS also faces a 2046 statutory deadline to fully fund its pension liabilities; the staff analysis concluded that investing in the LCTI would support this goal and would not be expected to raise contribution rates.

The Teachers Retirement Board investment committee unanimously voted in favor of allocating money to the Low Carbon Target Index. The fund’s holdings reached $17.5 billion (12.8% of public equities) by March 2024 and hit its target allocation in March 2025 with holdings of $29.7 billion (20.5% of public equities).

The fund’s allocation was almost $31 billion (20.7% of public equities) at the end of the second quarter of 2025. That the LCTI portfolio could receive such a volume of institutional capital speaks to the confidence that CalSTRS staff and board have with the index’s methodology, financial performance, and tracking error, and to the growing maturity of low-carbon investment strategies.

Responding to Market Shifts

CalSTRS’s investment joins those of peer funds that have made similar decisions to reduce holdings in assets that stand to lose from the energy transition. In achieving the 20% allocation to the LCTI, the fund’s investment staff have demonstrated that it is entirely possible for a prudent investor to shift away from fossil fuels while still meeting investment targets.

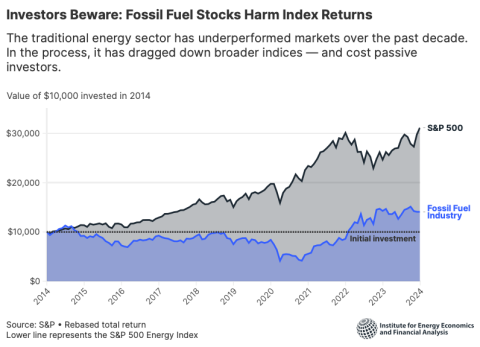

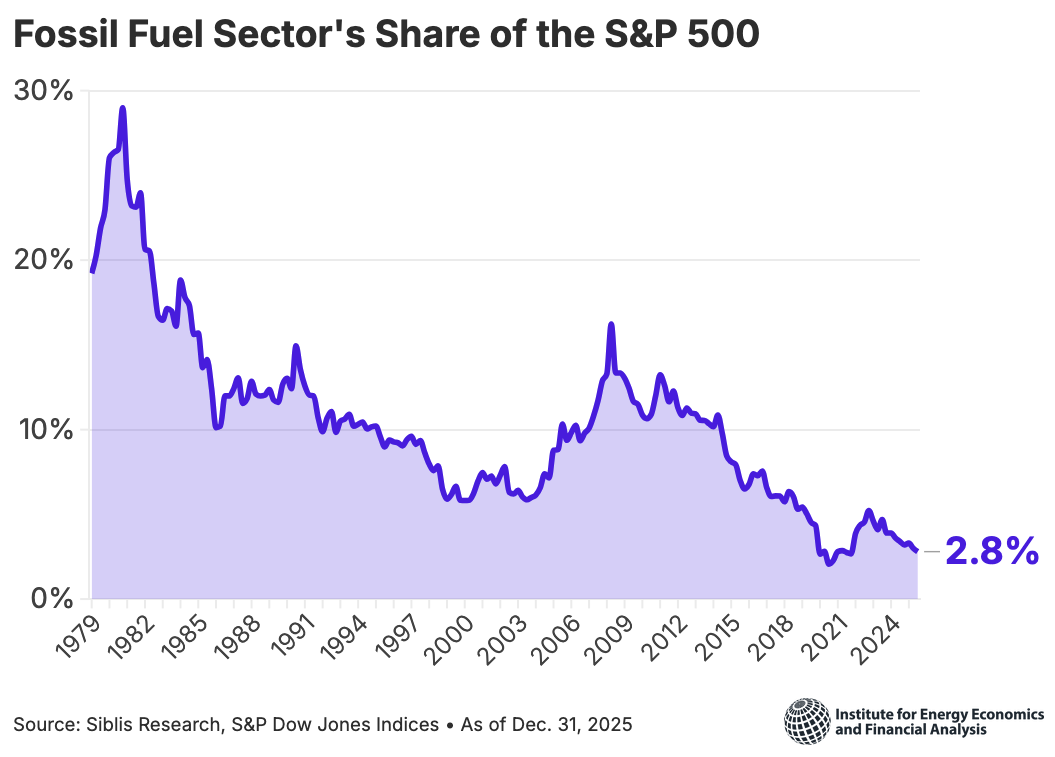

The fiduciary case for action on fossil fuels remains just as strong today as when the board made its initial decision in 2022. For several decades, the fossil fuel sector has struggled to keep pace with the overall market, falling from 30% of the S&P 500 in 1980 to the low single digits today. The sector saw a rash of poor performance, dragging down the stock market in seven years of the past decade.

Even when the fossil fuel sector’s equities have been lifted in the short-term by wars and geopolitical disruptions such as Russia’s invasion of Ukraine in 2022, competitive forces have continued to undermine the sector’s long-term outlook. The current war in the Persian Gulf appears to be reproducing the pattern.

Fossil fuel-importing nations are already resorting to energy conservation measures as ship traffic through the Strait of Hormuz has slowed to a trickle. The bottlenecks in crude oil, gas, and related products have prompted fears of fuel supply shortfalls and rationing.

In the medium term, importers can bolster national energy security by electrifying transport, industry, and heating alongside broader deployment of renewable energy and dispatchable battery storage. The growing supply chains, competitive costs, and long useful lives of these technologies position them to displace increasing amounts of imported fossil fuels, eroding long-term fossil fuel demand while reducing the import bill.

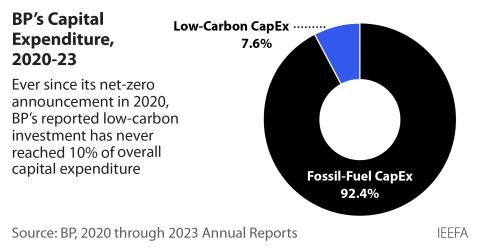

Meanwhile, narrow shareholder engagement-only approaches have so far failed to mitigate the financial risks posed by fossil fuel companies’ core business models. When BP announced a net-zero commitment in 2020, a CalSTRS official hailed the positive first step but warned that the target would need concrete plans and actions to be taken credibly. BP proved the skeptics right, allocating pennies on the dollar to transition investments while ultimately dismantling decarbonization targets and doubling down on long-run fossil fuel expansion. In doing so, the company provided a prime example of what’s long been known in the academic and practitioner literature: Engagement plans need escalation strategies and off-ramps to actually serve investors’ needs.

Of course, equity holdings are only one part of the climate risk puzzle. Importantly, the LCTI adoption has occurred alongside a range of complementary activities to protect portfolio value in a warming world, including tactical shareholder voting and thematic investments in net-zero technologies. Notably, in 2023, the board also voted to allocate 15% of its fixed-income portfolio towards a lower-carbon strategy—an important step for an often-overlooked source of potential climate-related loss. For CalSTRS and many peer funds, the shift away from fossil fuels seems to be actively opening the door to broader portfolio risk management and refocusing stewardship capacity towards the sectors and companies where it can deliver the greatest systemic impact.

When CalSTRS originally decided to adopt the LCTI, it left open the possibility of scaling up the allocation. Now that it has demonstrated that an initial 20% is well within prudent portfolio management, it should reexamine its target and consider aligning a greater share of the public equity portfolio with its risk-management goals. As its low-carbon fixed-income strategy continues to mature, it should formally evaluate the merits of increased ambition there as well.

Having taken these meaningful steps, CalSTRS faces a shifting terrain, buffeted by an energy transition but resilient in the face of political headwinds. Peer funds—including its pension sibling CalPERS, which has yet to take similar steps on the equity and debt fronts—should ask what lessons they can learn from CalSTRS' experience so far. And as it continues down its climate risk management path, CalSTRS has its work cut out for it. Beneficiaries, legislators, and other stakeholders will be closely watching the fund’s direction and speed of travel.

A note on methodology: IEEFA’s estimate of CalSTRS' fossil fuel holdings is based on a review of the fund’s Domestic Equity and International Equity portfolio holdings, as disclosed on the fund’s website and available from webpage archives. Holdings were compared to the oil, gas, and coal sector constituents of the Russell 3000 stock market index, plus a selection of companies primarily involved in the upstream, midstream, and downstream oil and gas industries sourced from German NGO Urgewald’s Global Oil and Gas Exit List.

Related Research