Iran conflict exposes Thailand’s LNG vulnerability

Key Findings

The Iran conflict poses heightened risks for gas-dependent Thailand, which relies on gas for 66% of its power output. Liquefied natural gas (LNG) accounts for 27% of its gas supply, and 28% of its cargo deliveries traverse the now-closed Strait of Hormuz.

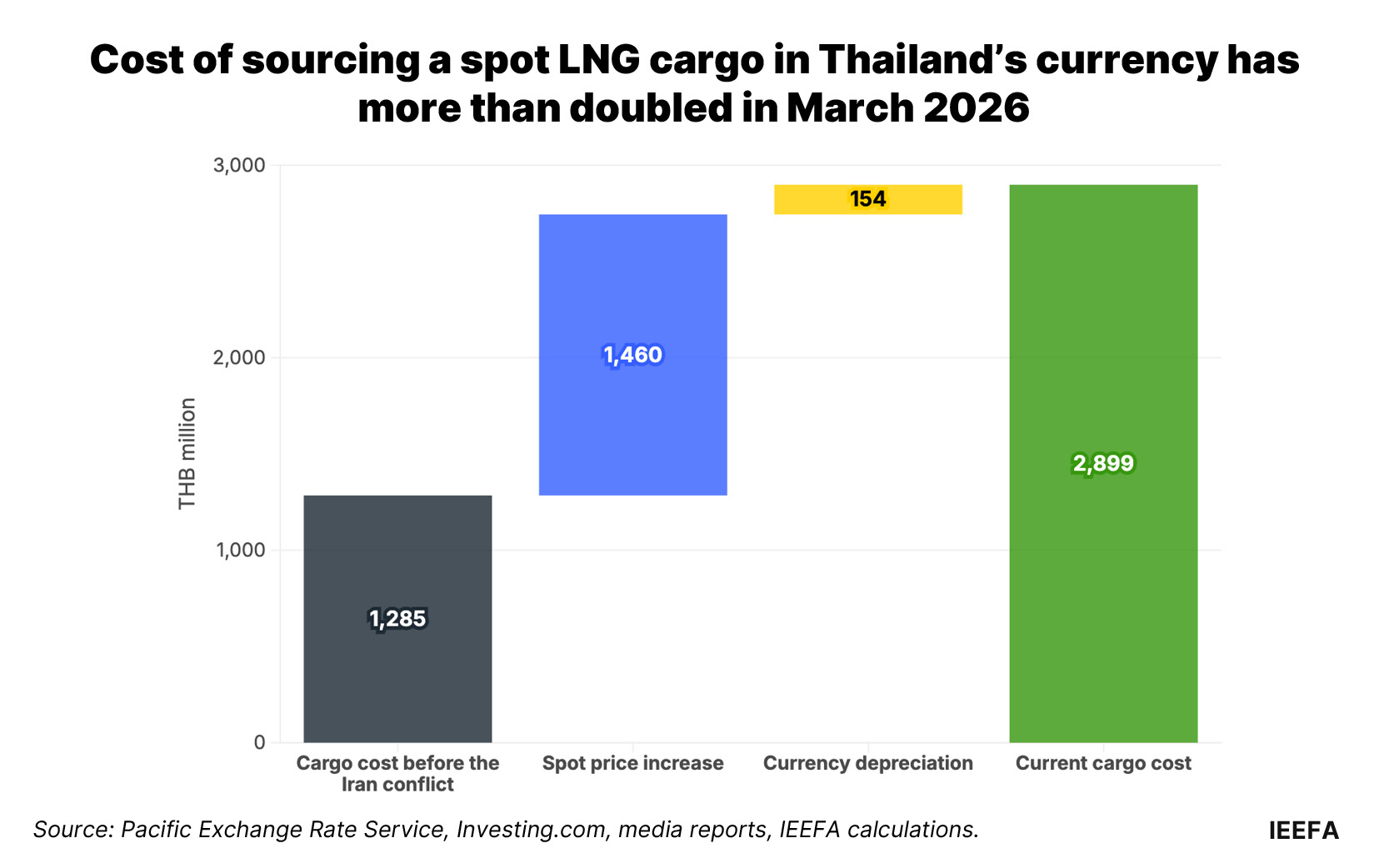

The fallout from the recent Middle East turmoil has increased Thailand’s cost of sourcing a spot LNG cargo by an estimated 125%. This increase is attributed to LNG prices rising from USD11 to USD23.50 per million British thermal units (MMBtu) and a 5.3% depreciation of the Thai Baht.

With gas-fired power becoming increasingly expensive and underutilized, the current Middle East crisis could prompt Thailand to set more ambitious renewable energy targets in its upcoming Power Development Plan (PDP), alongside policies to accelerate renewables deployment.

Output from Thailand’s 7.1 gigawatts (GW) of solar capacity could displace an estimated 1.3 LNG cargoes per month, avoiding nearly USD119 million in fuel costs at current prices.

For the second time in four years, Thailand is grappling with the macroeconomic fallout of managing a gas-reliant economy that is increasingly exposed to global commodity market volatility.

The Iran conflict has effectively closed the Strait of Hormuz, removing 21% of liquefied natural gas (LNG) from the global market. Asian spot prices jumped by 51% as of 9 March 2026, while oil-indexed deliveries rose by 35%.

Hope for a quick solution rapidly faded following attacks targeting the world’s largest gas field in Iran and the main gas liquefaction plant in Qatar on 18 March. QatarEnergy announced that two of its liquefaction trains sustained extensive damage. Repairing the facilities — responsible for over 3% of global LNG supply — will take three to five years, and an expansion could be delayed by a year.

The long lead time required to replace this capacity is likely to exert sustained upward pressure on LNG prices as buyers compete for limited replacement supplies. Past experience suggests that some Asian buyers could struggle to secure cargoes in these bidding wars.

The LNG supply shortage is particularly concerning for Thailand, which relies on gas for 66% of its power output. LNG imports account for 27% of its gas requirements, and 28% of its deliveries traverse the Persian Gulf. Moreover, the country spends more than 7% of its gross domestic product (GDP) on oil and gas imports. This share is highly likely to rise with Thailand reportedly paying upwards of USD23 per million British thermal units (MMBtu) for replacement cargoes, up from USD11 per MMBtu before the conflict.

Additionally, currency depreciation — a common occurrence during economic crises — exacerbates affordability challenges. Following the 5.3% depreciation of the Thai Baht in March 2026, the Institute for Energy Economics and Financial Analysis (IEEFA) estimates that the cost of purchasing an LNG cargo has increased by 125% in local currency terms.

Government aims to spread power costs across the Thai economy

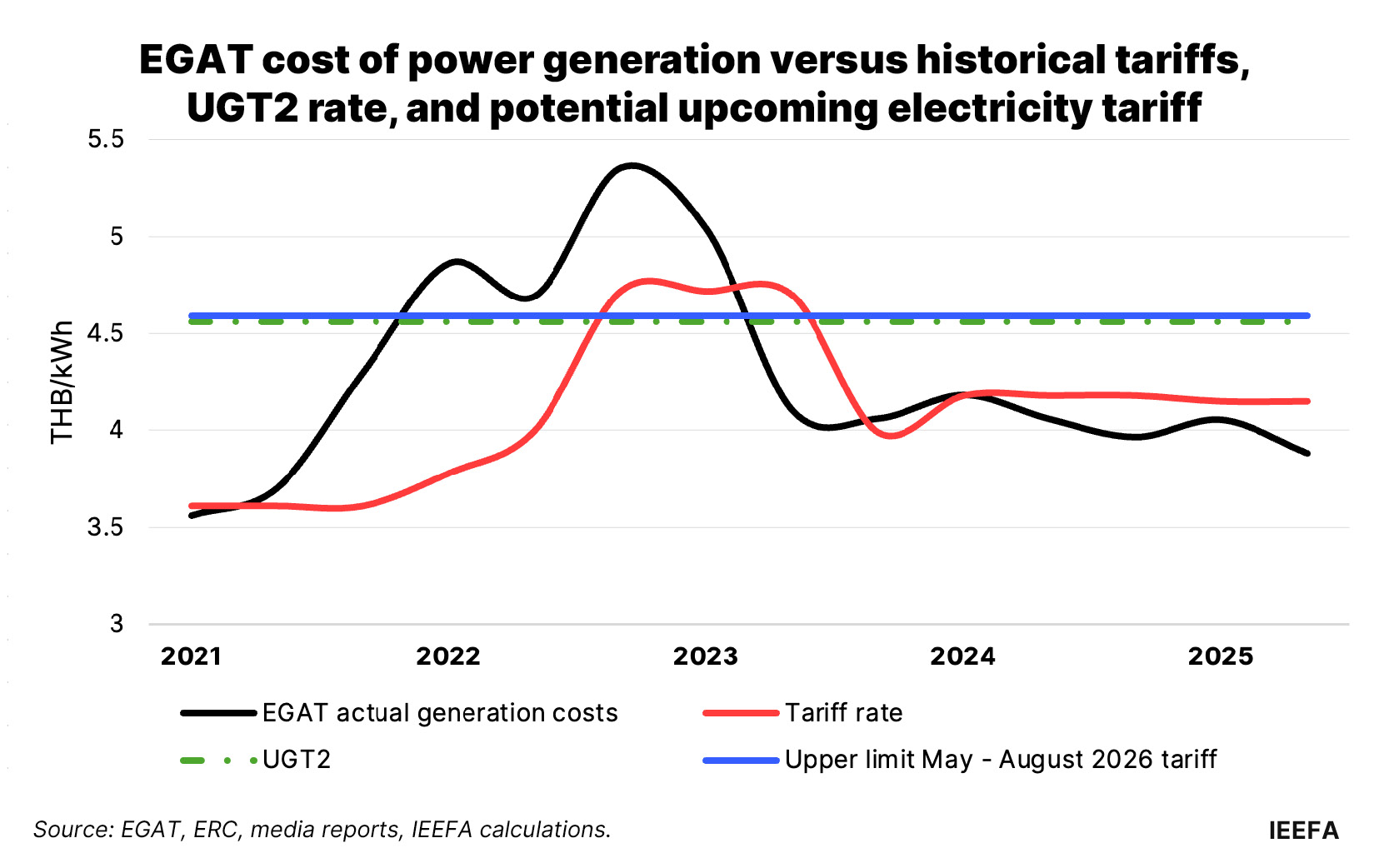

Thailand’s Energy Regulatory Commission (ERC) aims to balance consumer welfare with government debt as it revises the fuel adjustment component of the next electricity tariff. If the government opts to fully repay the national utility Electricity Generating Authority of Thailand’s (EGAT) outstanding debt, the rate could increase from the current THB3.88 per kilowatt-hour (kWh) to 4.59/kWh. Alternatively, deferring repayment and applying a clawback mechanism could limit the increase to around THB3.95/kWh.

EGAT still has an unpaid debt of THB36 billion resulting from the 2021–2023 energy crisis, while the state-owned gas supplier, PTT Public Company Limited (PTT), holds nearly THB13 billion in outstanding debt.

Consumers have limited capacity to absorb further price increases. Thailand’s economy was already enduring a fragile post-pandemic recovery before the current crisis, compounded by domestic structural weaknesses and an uncertainty surrounding United States (US) trade policy. Intensifying competition in export-oriented manufacturers led to 5,000 factory closures between 2021 and May 2025.

In response, the government is prioritizing cheaper options to help manage these priorities. The ERC has ordered the restart of 0.6 gigawatts (GW) of coal power and is exploring higher output from hydroelectricity to limit immediate exposure to LNG markets.

However, a recent IEEFA report found that growing reliance on LNG, alongside gas turbine bottlenecks, was already challenging the economic viability of Thailand’s gas-heavy power ambitions. A more than twofold increase in sourcing costs underscores these challenges and strengthens the case for an accelerated transition to renewable energy.

Thailand’s gas reliance is a strategic vulnerability

Gas expansion projects outlined in previous energy plans ushered in Thailand’s current era of LNG dependence. In the first half of this decade, the country brought 9.7GW of gas-fired power projects online, while the share of gas supply from LNG imports nearly doubled.

The now scrapped Draft Power Development Plan 2024 (Draft PDP 2024) continued this expansion strategy, proposing an additional 6.3GW of new gas-fired capacity. If realized, this could nearly double Thailand’s LNG import requirements.

However, most projects have faced significant delays, with EGAT canceling tenders for three facilities in 2025. The tripling of capital costs for combined-cycle gas turbines (CCGTs) in the last two years is likely a contributing factor to these setbacks.

The recent prioritization of lower-cost alternatives — alongside demand responses to policy changes and higher tariffs — could reduce the utilization of gas-generating units. While fuel costs may fall, consumers will continue to pay for idle assets through availability payments. EGAT equated the value of capacity payments at THB0.63/kWh — or 17% of the base electricity tariff — during the first tariff cycle of 2026.

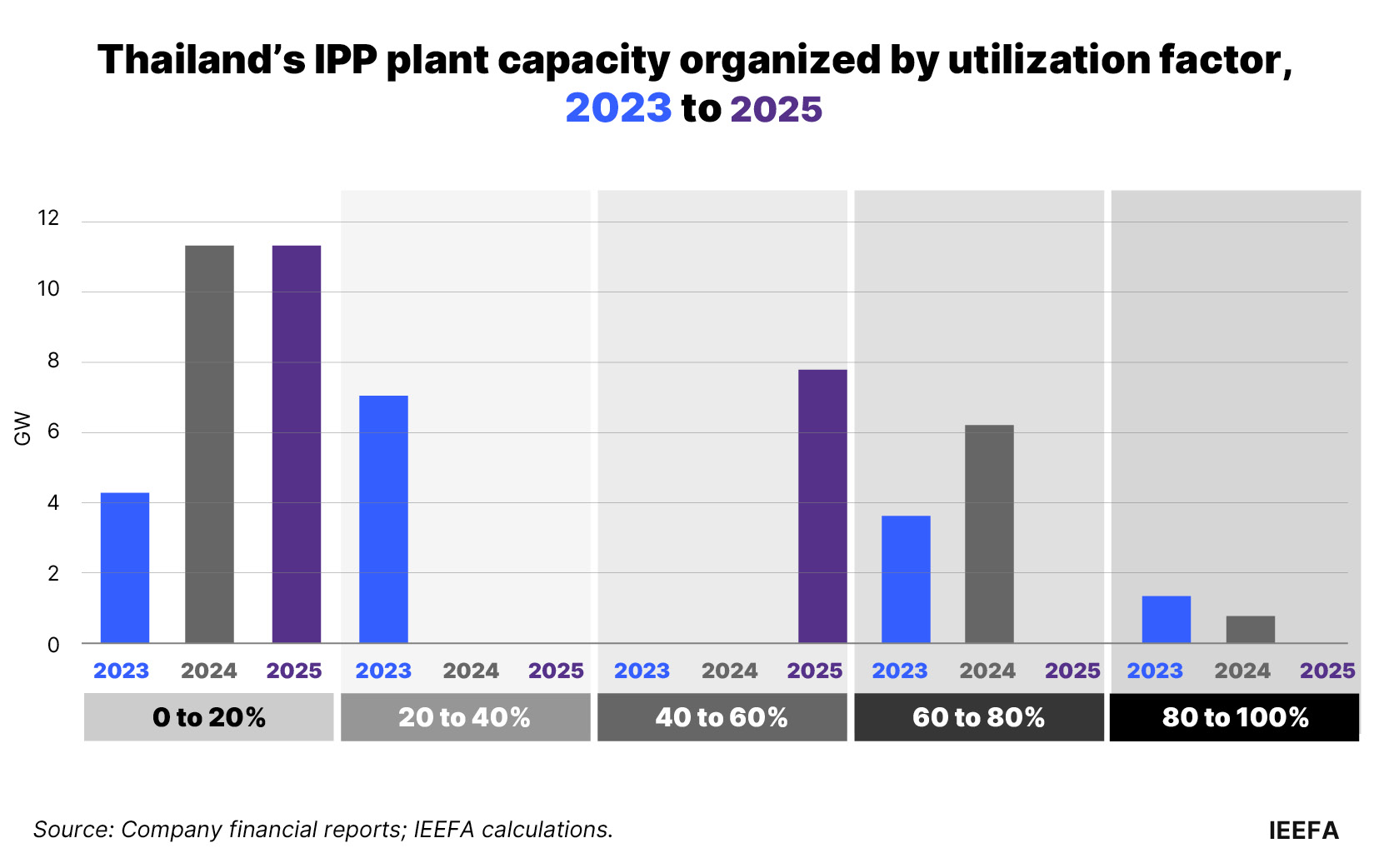

IEEFA’s report also found that, since 2023, seven gas-fired plants totaling over 11GW of capacity have operated at dispatch rates under 30%. A weak post-pandemic recovery, coupled with an overbuild of gas-fired capacity based on overly ambitious economic projections, has resulted in an electricity supply glut. In 2025, dispatch rates at these facilities dropped below 10%, prompting the government to suspend the operation of 4GW of gas plants in October.

Despite this underutilization, EGAT reportedly paid these plants over THB159 billion (USD5.02 billion), including THB61 billion during periods when the units were scheduled to generate zero electricity. Utilization rates at Thailand’s gas plants could fall further due to the Iran conflict.

While neighboring countries relaxed ownership restrictions to accelerate renewable energy deployment, Thailand imposed a 49% foreign shareholding cap on electricity companies in 2023. In late 2024, the government also delayed signing contracts for more than 2GW of renewable capacity, citing concerns that a flawed auction process could elevate prices. This regulatory uncertainty has eroded investor confidence in renewables, likely delaying or canceling projects that could otherwise help mitigate the impact of the current crisis.

An opportunity to improve resilience by advancing renewable energy

With gas-fired power plants becoming increasingly expensive and underutilized, the Iran conflict provides another reason for Thailand to accelerate its renewable energy transition.

According to the country’s Department of Alternative Energy Development and Energy Conservation (DEDE), domestic solar capacity doubled in 2025 to almost 7.1GW. At a 15% capacity factor, IEEFA estimates that these solar panels could generate enough power to displace 1.3 LNG cargoes per month, avoiding nearly USD119 million in fuel costs at current prices. At lower prices, every 1GW of solar can help avoid USD3 billion in fuel costs over the lifetime of the panels. Deploying renewables can create savings that can fund fiscal initiatives, including mitigating the impact of parallel commodity market disruptions.

The preparation for the next PDP is an opportunity for policymakers to reduce Thailand’s gas exposure by making more ambitious renewable energy commitments. However, this will require reforms to electricity market policy to better incentivize private investment in renewable projects and to give consumers greater agency in selecting energy providers.

Some recent policy initiatives may support this shift. For example, a community solar power initiative launched in October 2025 aims to reduce electricity costs by delivering 1.5GW of ground-mounted solar capacity nationwide at a rate of THB2.24/kWh.

While the upcoming Direct Power Purchase Agreement (DPPA) pilot will procure up to 2GW of renewables for data center developments, the current conflict should serve as an impetus to urgently expand program eligibility to other sectors.

In addition, the upcoming phase of the Utility Green Tariff (UGT2) program will allow large commercial and industrial users to contract 2.1GW of power from solar, wind, and biogas energy for ten years at a rate of THB4.56/kWh.

While expensive compared to recent tariff averages and levelized cost of energy (LCOE) estimates, the UGT2 rate could serve as a hedge for users concerned about the inflationary impact of higher LNG prices. During the previous energy crisis, both retail tariffs and EGAT’s generation costs surpassed this level for prolonged periods. Moreover, the new electricity tariff would compare favorably with the upper limit of THB4.59/kWh currently under consideration by the ERC. However, the government has yet to formally launch the UGT2 program.

Recent policy changes are improving Thailand’s rooftop solar market. In late 2024, factory licensing requirements for installations outside industrial estates were relaxed. In November 2025, a building modification exemption reduced administrative hurdles for roof installations and expanded eligibility beyond residences to include commercial and industrial buildings. On 3 March 2026, the government introduced an income tax relief grant of up to THB200,000 (USD6,200) to finance rooftop solar installations on residential units, effective through to the end of 2028.

Faced with high UGT2 rates and LNG-driven inflation in grid electricity prices, Thailand consumers could improve energy security by investing in rooftop solar, mirroring developments in Pakistan following the 2022 energy crisis. There, low-cost panel imports by consumers in Pakistan increased domestic distributed solar capacity to 34GW, delivering billions in avoided fuel imports and proving that the energy transition can be consumer-driven as well.

Thailand was already struggling to manage its reliance on gas prior to the Iran conflict. Recent disruptions have reinforced the risks associated with LNG as an unreliable and costly fuel source. This crisis should prompt a reassessment of the country’s energy strategy, with the next PDP providing an opportunity towards a more secure, low-carbon power system aligned with its updated Nationally Determined Contribution (NDC).

Establishing a more supportive environment for cheaper renewable energy would not only mitigate the impacts of expensive fuel imports during the current crisis but also enhance Thailand’s resilience in the face of future disruptions.

Related Content