Iran tensions underscore the urgency of Asia’s renewables pivot for macroeconomic stability

Download Briefing Note

Key Findings

The duration of the Iran conflict is unclear, but Asian countries are already responding with emergency energy security measures and economic interventions. Crude oil and liquefied natural gas (LNG) rose 51% and 77%, respectively, between 27 February and 9 March 2026.

Subsidies and monetary tightening offer short-term inflation relief but can weigh on capital markets and hinder national priorities. Governments may also freeze end-user tariffs, creating margin and working capital pressures for utilities amid rising fuel costs.

The 2022 energy crisis demonstrated the acute financial stress that fuel price shocks can inflict on other key sectors, like agriculture and manufacturing. These risks are most pronounced for emerging Asian economies, which are expected to be the largest fossil fuel growth markets but are often least able to mitigate the economic impacts of fuel price volatility.

At current LNG prices, the levelized cost of electricity from gas-fired power is 3–4 times the global average for solar and wind, and gas-fired power is uncompetitive with solar plus storage in many Asian markets. IEEFA estimates that every 1 gigawatt (GW) of solar could avoid USD3 billion in LNG import costs over 25 years.

For the second time in four years, energy markets in Asia dependent on imported fossil fuels find themselves at the mercy of global commodity markets. Although each country’s immediate exposure to the Iran conflict varies, all face the indirect threat of higher costs driven by tighter fossil fuel markets and elevated geopolitical risk premiums.

The duration of the conflict, the extent of disruptions in the Strait of Hormuz, and outages at key energy infrastructure in the Persian Gulf remain key unknowns. Prolonged escalation could cause energy price spikes to spill over into core economic indicators — including inflation, interest rates, trade balances, and gross domestic product (GDP) growth — derailing fiscal and monetary goals. Budgetary measures like fossil fuel subsidies, along with monetary tightening, provide short-term relief but can present costly longer-term drags on capital markets and other national priorities.

Asian economies are reacting to the current crisis in various ways, but the risks of fossil fuel dependence are forever. Absent an accelerated transition to renewable energy, commodity market volatility will continue to undermine energy and economic plans, elevate borrowing costs, and cloud investor returns. In contrast to volatile imported fuel prices, renewable energy costs have consistently declined over the past two decades, and simple cost metrics underestimate their value by ignoring avoided fuel expenses.

Once again, the urgency of Asia’s clean energy transition for energy security and macroeconomic stability has become unmistakably clear.

Exposure of Asian energy markets to the Iran conflict

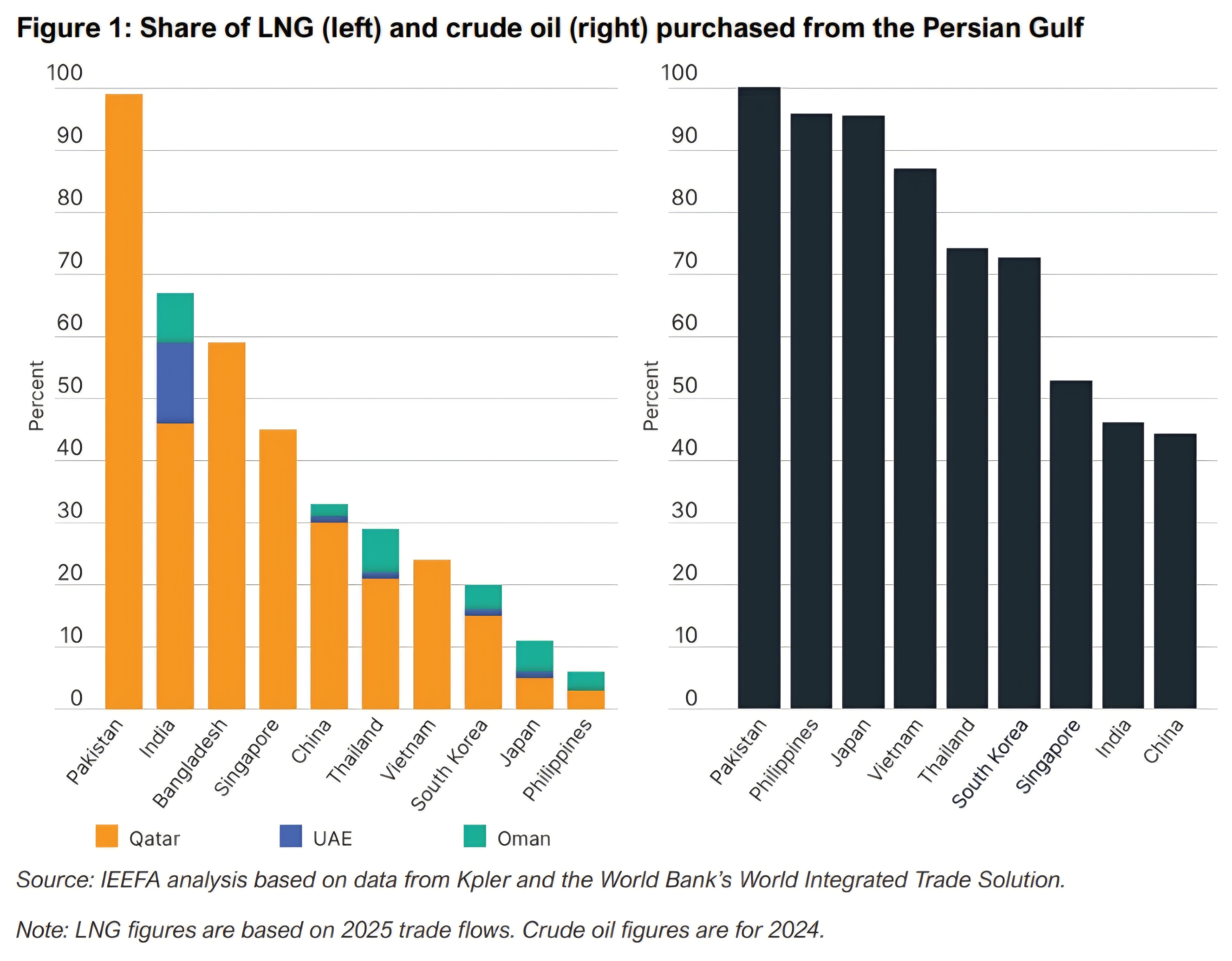

Over 80% of crude oil and liquefied natural gas (LNG) leaving the Strait of Hormuz is destined for Asia, though individual markets face varying levels of exposure to the current conflict. In 2025, Pakistan, India, and Bangladesh sourced the largest share of LNG from Qatar and the United Arab Emirates, while Pakistan, Japan, and the Philippines each sourced over 90% of their crude oil supplies from the Persian Gulf (Figure 1).

Immediate exposure to the conflict depends on many factors, including the availability of oil and gas storage, long-term fuel purchase contracts, and alternative energy sources. For instance, Japan has petroleum reserves equivalent to 254 days of demand, while Vietnam has less than 20.

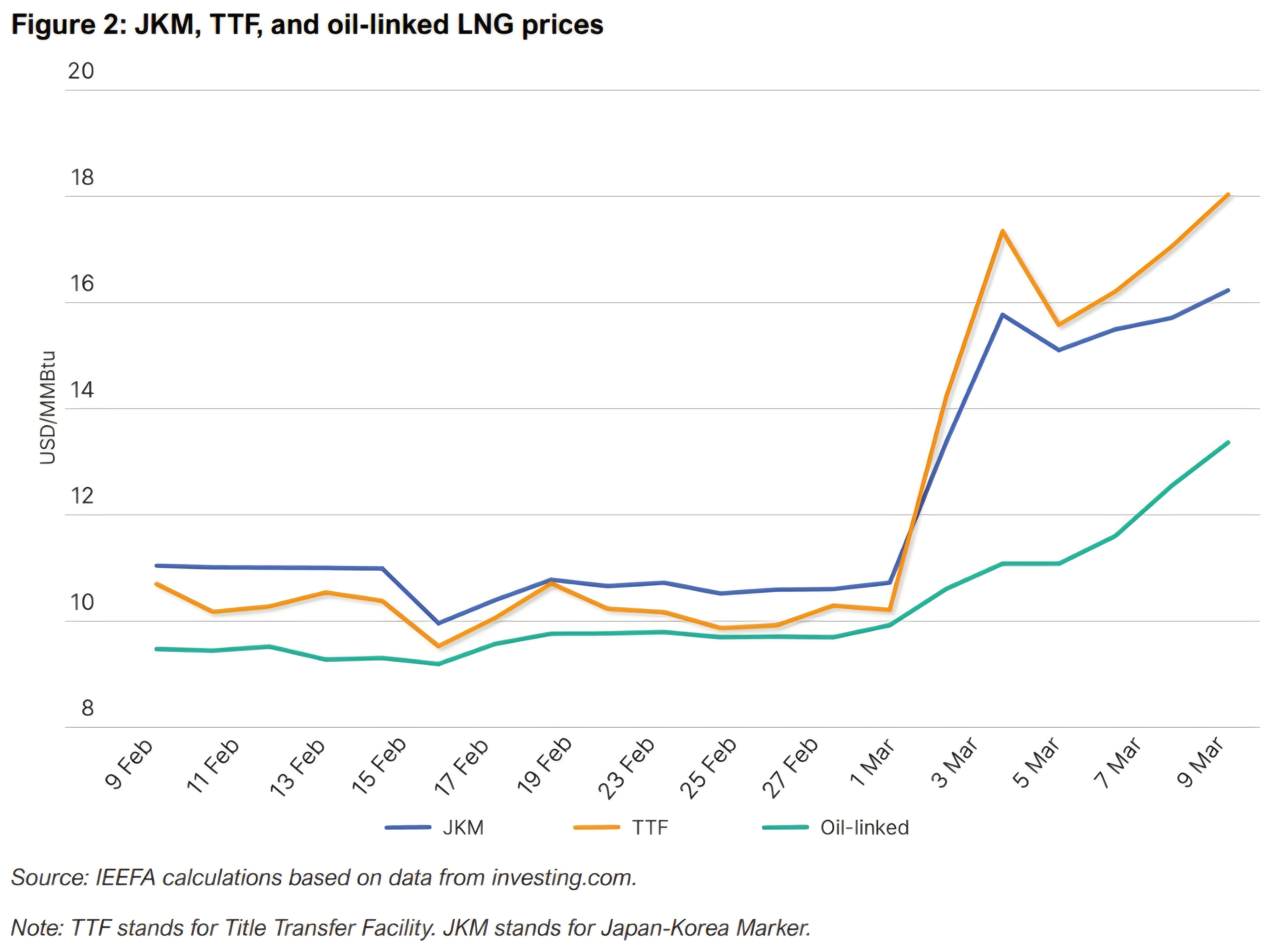

Most countries in Asia lack underground gas storage, exposing them more directly to price spikes in global gas markets. The Japan-Korea Marker (JKM), Asia’s LNG spot benchmark, spiked 50% between 27 February and 9 March 2026 (Figure 2). Bangladesh purchased a cargo at USD28.28 per million British thermal units (MMBtu) — nearly three times JKM prices last month — while Pakistan has halted LNG purchases altogether.

The Philippines and Vietnam began importing LNG in 2023 and purchase most cargoes from spot markets. They are therefore highly exposed to price spikes, despite only buying a small share of LNG from the Middle East.

Currency depreciation and inflation exacerbate energy price spikes

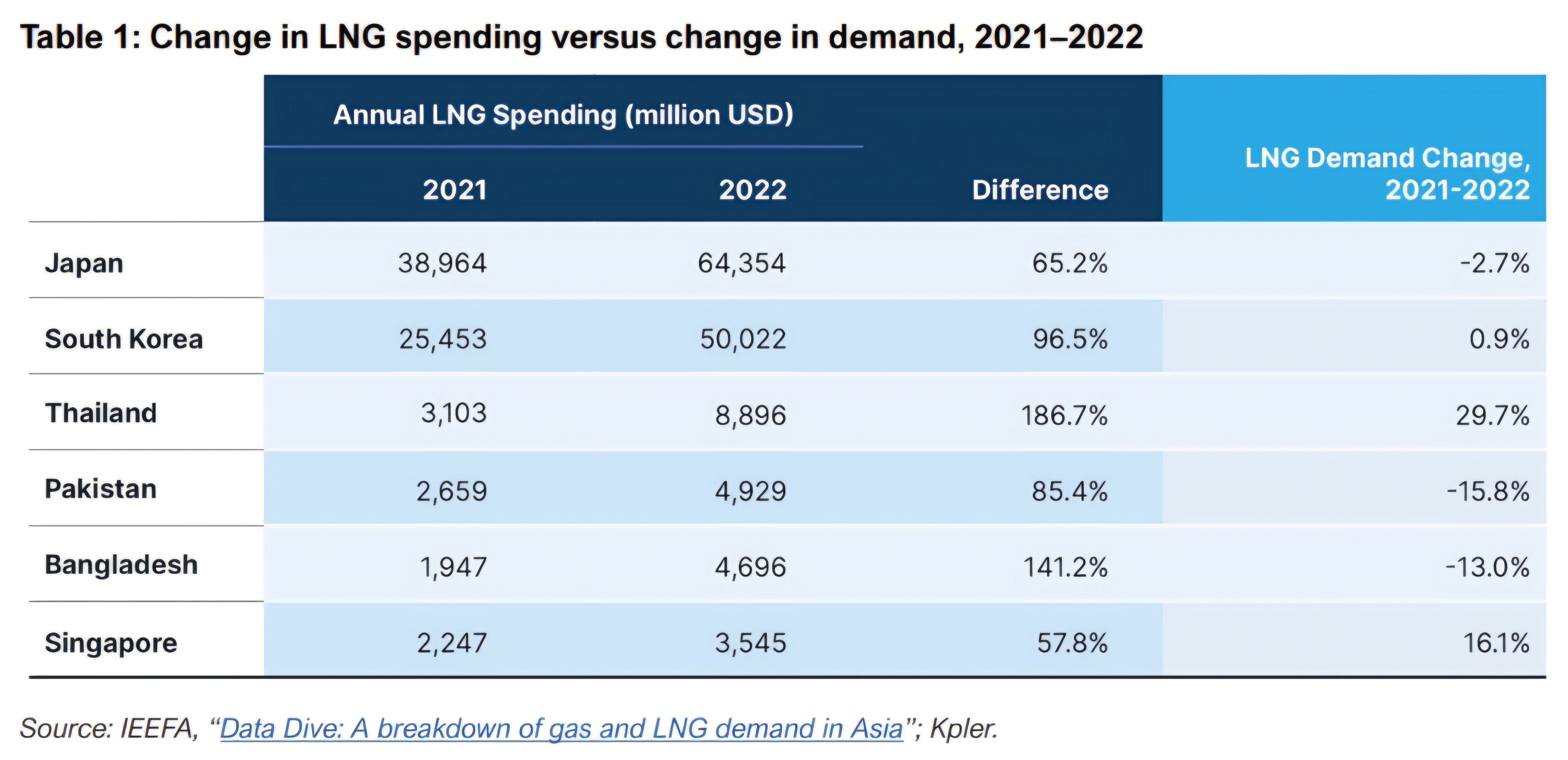

Extended price spikes for US dollar-denominated fossil fuels can cause annual import bills to skyrocket, even if demand declines. Following the Russian invasion of Ukraine in 2022, annual LNG spending in both Pakistan and Bangladesh more than doubled compared to 2021, even though imports declined by 16% and 13%, respectively. In Japan, LNG demand fell by nearly 3%, but annual spending increased 65% (Table 1).

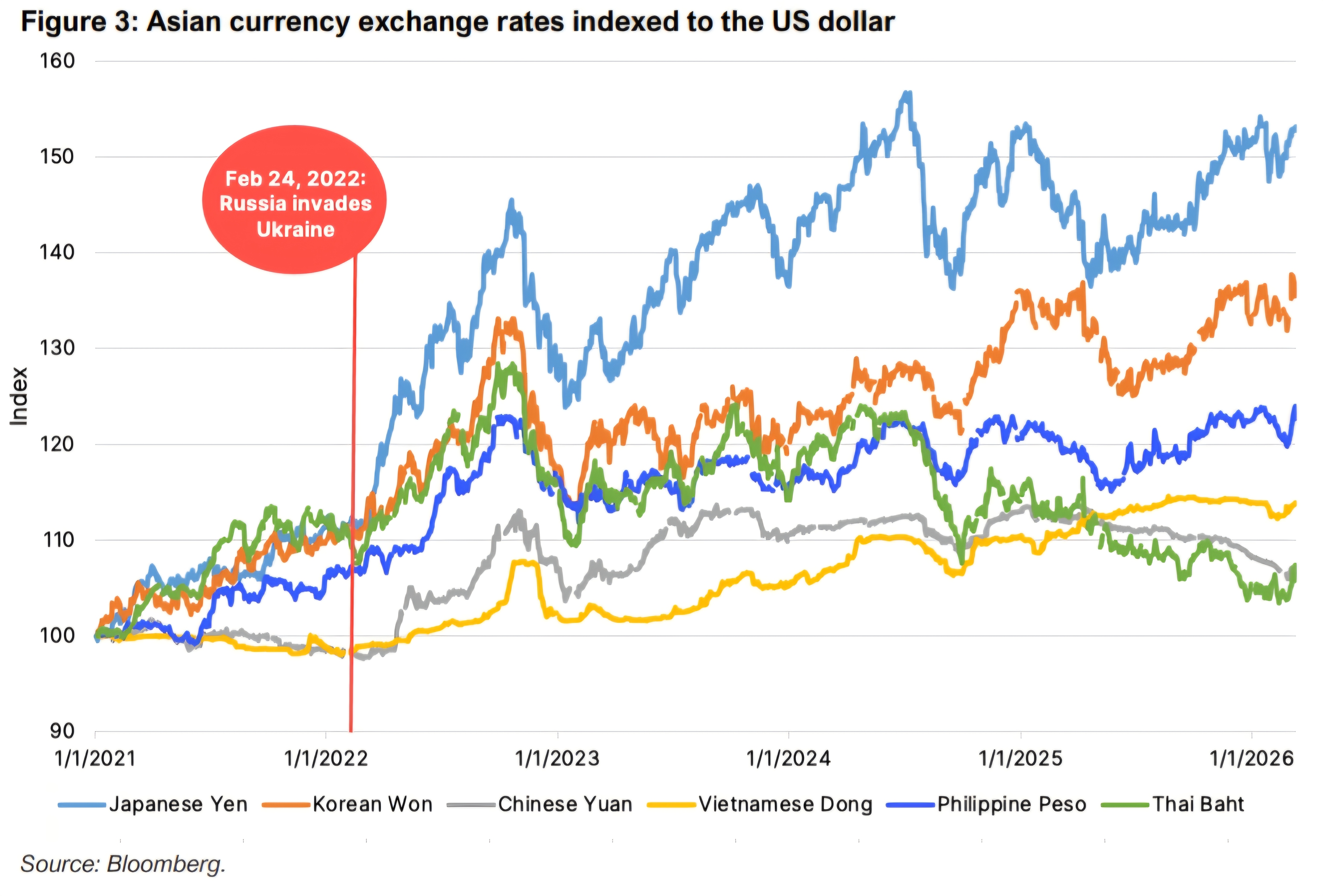

The result is a significant drawdown in foreign exchange reserves and a depreciation of local currencies. All net oil and gas importing countries in Asia experienced currency depreciation against the US dollar in 2022 (Figure 3). In the first seven days of the Iran conflict, emerging market currencies faced their worst week since 2020, as traders flock to safe havens in gold and US dollars.

As energy prices rise and local currencies depreciate, energy imports become even more expensive in local currency terms, creating a potentially vicious feedback loop. Weak exchange rates may even persist when energy costs fall. Research by the Institute for Energy Economics and Financial Analysis (IEEFA) and Transition Zero in 2023 found that the weakening of the Pakistani rupee following the 2022 energy crisis left consumers paying high gas-fired power costs, even as global LNG prices eased.

During major inflationary “risk-off” episodes like the Iran conflict, foreign exchange and capital markets often move in tandem, tied together by investor sentiment. Higher imported energy costs raise operational expenses for local businesses, squeezing profits and equity valuations. Industries dependent on imported inputs pay in US dollars, presenting margin risks if higher costs are not passed through in the sale of finished goods. Companies with US dollar-denominated debt face rising repayments in local currency terms, potentially triggering credit downgrades.

Risks are especially significant for emerging Asian economies, which are simultaneously expected to be the largest growth markets for fossil fuels and often the least able to mitigate economic challenges when prices go haywire.

Governments in Asia are already addressing inflation risks through fiscal and monetary policy measures, along with fossil fuel supply responses. Thailand has capped diesel prices and may slash fuel taxes. China, Thailand, and some Indian refineries have halted exports of crude and refined products to shore up domestic supplies. The Philippines central bank said it may tighten monetary policy to curb inflation risks if oil prices rise above USD100 per barrel, indirectly raising the cost of debt for households, businesses, and the government.

Fiscal measures, such as costly fuel subsidies and tax cuts, provide short-term relief from inflationary shocks. But they can also restrain spending on other national priorities and lead to budget deficits, potentially elevating sovereign bond yields. Between 2022 and 2024, Japan spent JPY11 trillion (USD77 billion) on electricity, gas, and petrol subsidies to mitigate inflation caused by the Russia-Ukraine conflict.

Thailand’s Oil Fuel Fund, which subsidizes domestic fuel prices, recorded a peak deficit of -THB133 billion (-USD3.7 billion) in November 2022, with liabilities exceeding 40% of assets. Although the fund has a current surplus of THB2 billion in reserves, higher energy prices are likely to mean a return to deficit. The fund is reportedly spending THB700 million per day, and the government is preparing to secure more loans from commercial banks to boost liquidity.

Energy subsidies can also be pushed onto the balance sheets of state-owned energy companies by setting regulated end-user tariffs below the cost of fuel and power supply.

In 2022, South Korea’s state-owned utility, the Korea Electric Power Corporation (KEPCO), came perilously close to bankruptcy, as fossil fuel costs skyrocketed while end-user tariffs remained frozen to curb inflation. The company experienced an annual operating loss of KRW32.6 trillion (USD24.4 billion), and total liabilities surged above KRW200 trillion (USD153 billion). Although it narrowly escaped insolvency — through multi-year rate increases starting in late-2022, government-backed debt ceiling hikes, relaxed capital limits, and aggressive restructuring — KEPCO still faces a KRW205 trillion debt burden, soaring interest expenses, and vulnerability to future fuel price shocks that could reignite solvency concerns.

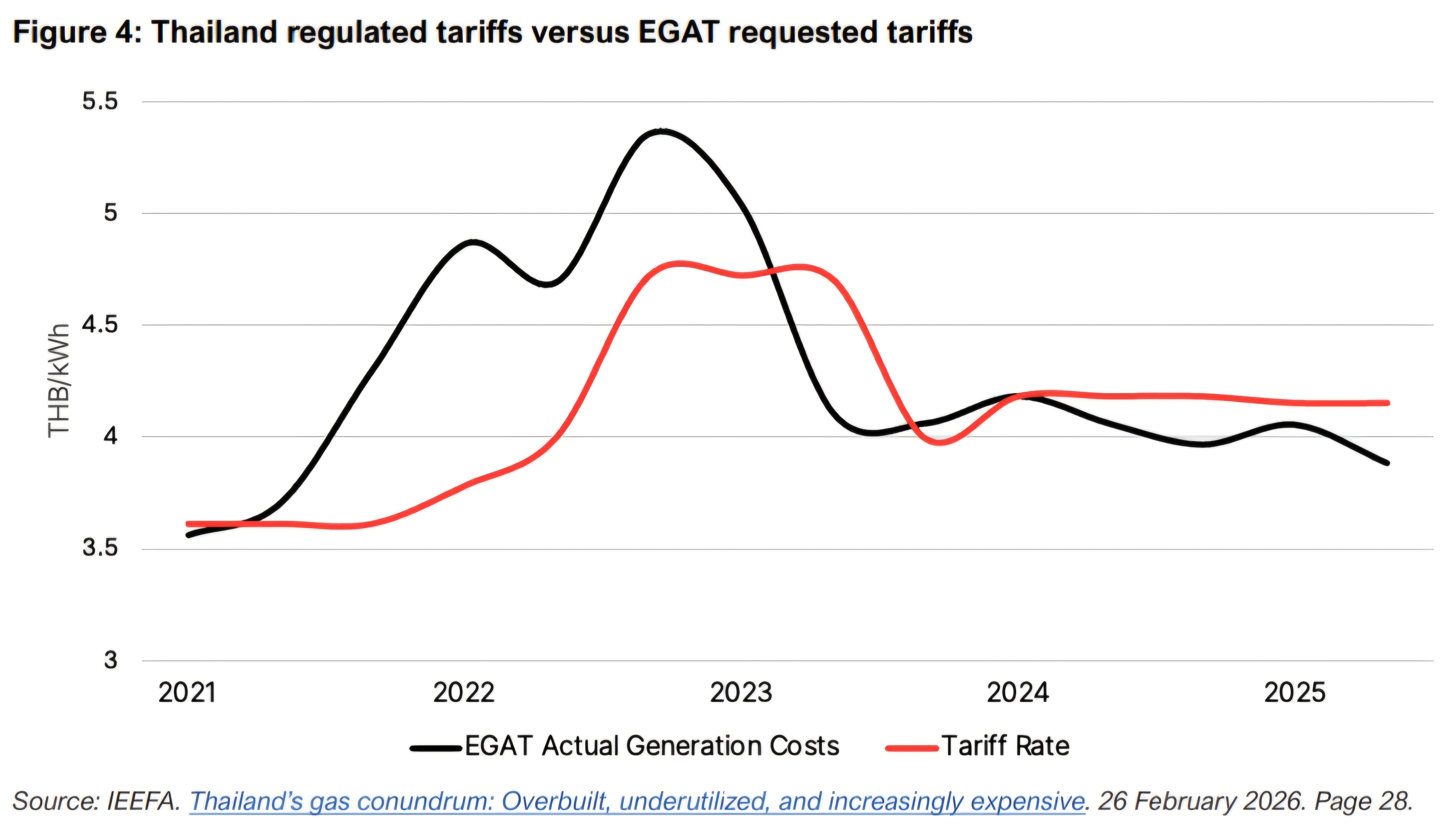

Beginning in 2021, Thai regulators also set power tariffs below the cost of generation, limiting the pass-through of higher electricity prices to end-users and causing debt at the state-owned power utility Electricity Generating Authority of Thailand (EGAT) to rise to USD4.3 billion in 2022 (Figure 4). Although commodity prices have eased, end-user tariffs remain above generation costs to help EGAT recoup deferred revenues, demonstrating the longer-term impact of price spikes on consumers.

The Philippines has a largely privatized energy market, but its largest power generation company, San Miguel Global Power, faced a severe liquidity crunch in 2022 and 2023, resulting from substantial contractual exposure to global fossil fuel prices. The company refinanced existing debt at elevated rates and, in 2024, sold 67% of its LNG assets to strengthen its balance sheet. However, it still faces significant callable obligations through 2030. Monetary tightening in the country could compel another round of refinancing at even wider spreads, further straining the company’s long-term investment plans and financial position.

Renewables are the long-term solution

While fiscal, monetary, and fossil fuel supply measures may help energy importers temporarily withstand price shocks, they do not fundamentally resolve them. The most financially sustainable, long-term solution is to reduce exposure to global market volatility altogether by rapidly deploying renewable energy.

At current JKM prices of USD15/MMBtu, IEEFA estimates that the fuel costs alone of operating a one-gigawatt (GW) gas-fired power plant at baseload levels — not including regasification, pipeline transportation, or generation plant capital cost recovery — would cost nearly USD800 million. The resulting levelized cost of generation would be roughly USD130–140 per megawatt-hour (MWh), comparable to the prices currently demanded by developers of newbuild LNG-to-power projects in Vietnam.

In its latest levelized cost of energy (LCOE) report, Bloomberg New Energy Finance estimated that the costs of onshore wind and solar had fallen globally to USD40/MWh and USD39/MWh, respectively. Meanwhile, average levelized costs for combined cycle gas plants have increased since 2024 due to a global shortage of available turbines. Turbine costs have more than doubled to over USD2,400 per kilowatt in just the last two years.

Levelized cost estimates vary by country, and in many Asian economies, renewable energy costs have remained above global averages. However, IEEFA analysis shows that current LNG prices make gas-fired power uncompetitive with firm solar plus storage, even after accounting for inflation-driven increases in capital costs for renewable projects. If LNG prices remain 50% above 2025 averages, the cost of gas-fired power could increase by an estimated 32–37%. By contrast, solar power costs are expected to rise by just 3%, even after assuming a 100 basis points (bps) increase in the cost of capital to address inflation driven by the energy crisis. Relying on gas, therefore, appears to be a lose-lose proposition — greater energy insecurity at a higher cost.

Levelized cost metrics are often criticized for privileging renewables by not capturing the dispatchability of various technologies. However, they also overlook the extreme price volatility of LNG-fired power plants by relying on static assumptions. Actual all-in LNG-to-power prices can vary widely depending on global fuel costs, exchange rates, and plant utilization rates.

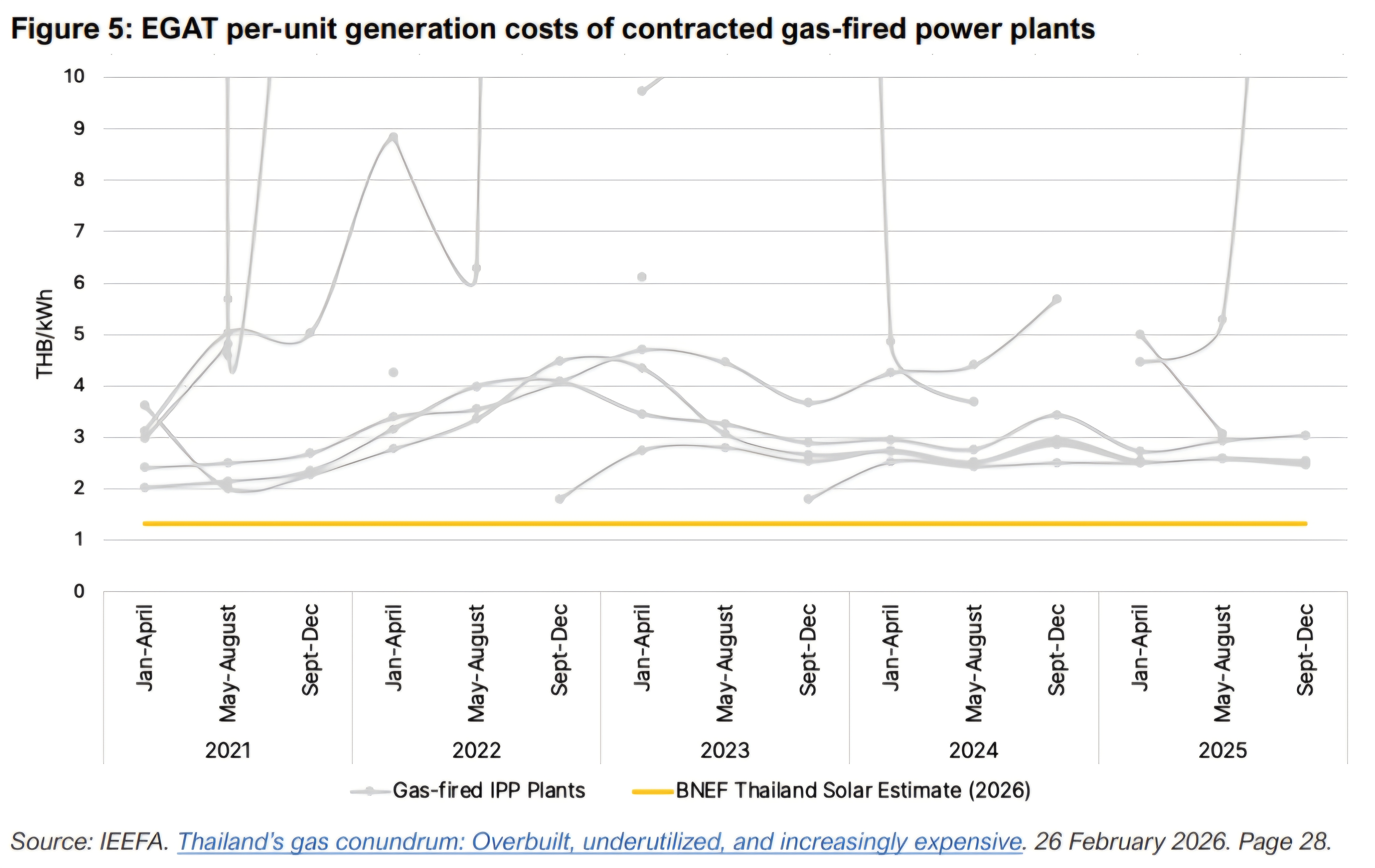

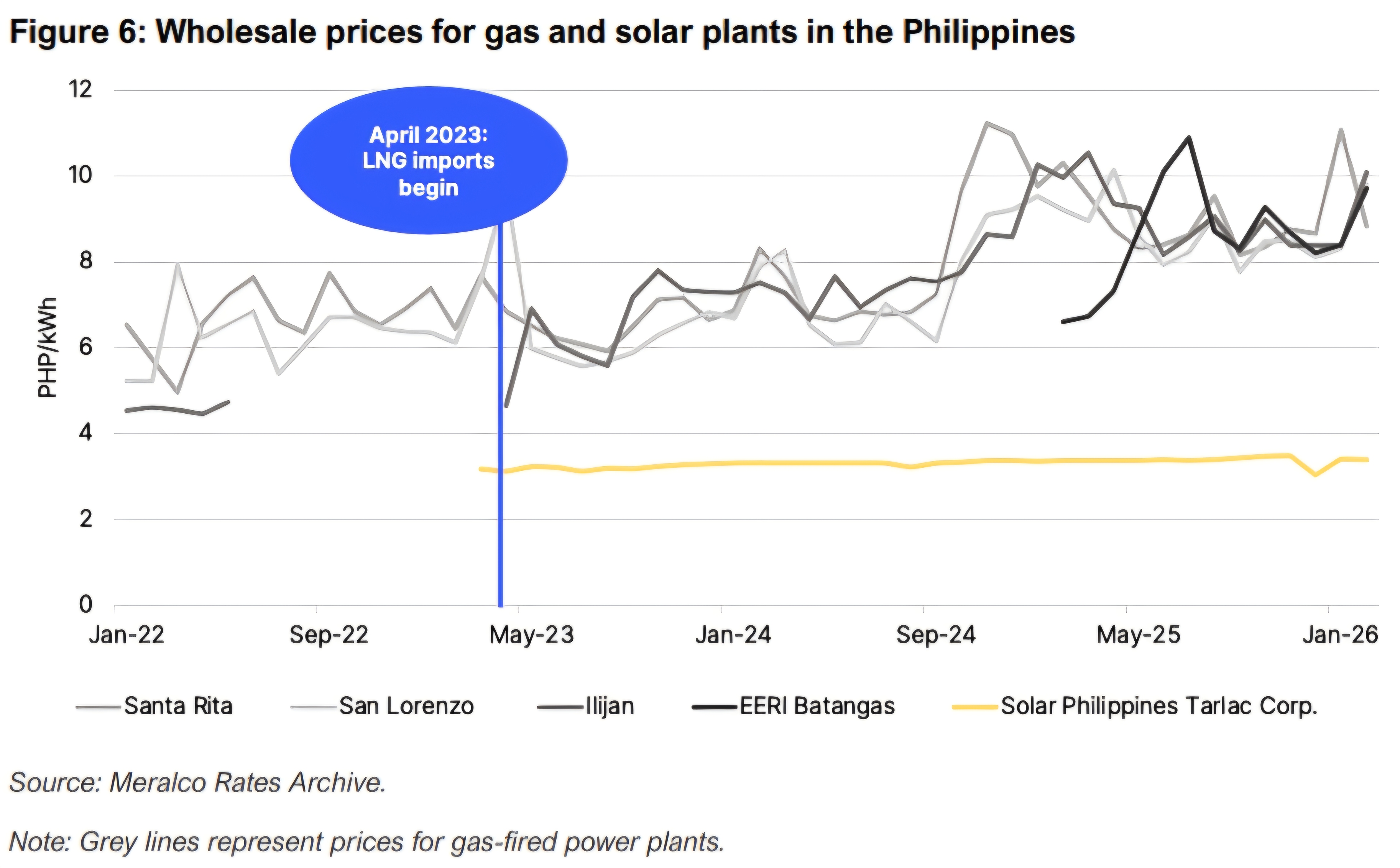

A recent IEEFA analysis of Thailand’s power markets shows the significant variation in gas-fired power prices sold to EGAT (Figure 5). Prices regularly exceed THB4 per kilowatt-hour (USD130/MWh) when plants operate at lower capacity, as fixed capacity payments are amortized over lower output. In the Philippines, the introduction of LNG in 2023 has caused a persistent increase in gas-fired power costs for Meralco, the country’s largest distribution utility, in stark contrast to the stable prices offered by solar (Figure 6).

Additionally, the levelized costs of renewables do not capture the inherent value of avoided fossil fuel import costs. IEEFA estimates that 1GW of solar capacity could potentially replace 0.16 million tonnes per annum (MTPA) of LNG demand, avoiding USD128 million in LNG imports at current prices and more than USD3 billion over the solar plant’s lifetime. While this assumes a direct replacement of LNG with solar that may be complicated in practice, competitive power markets around the world have demonstrated that zero-marginal-cost renewables will displace the highest-cost generator. In Asia, this is typically gas.

Conclusion

All the risks outlined here were on full display in the aftermath of Russia’s invasion of Ukraine. While fossil fuel prices have not reached similar levels in the first two weeks of the Iran conflict, markets are starting to brace for longer-term upheaval. United States President Trump has said the conflict could last “four to five weeks” and called for Tehran’s “unconditional surrender.” Qatar’s energy minister warned that the war could “bring down the economies of the world” and push oil prices to USD150 per barrel. Financial analysts have suggested this could be “a new global inflationary shock in the making.”

Regardless of the length of this conflict, geopolitical risk never disappears. Fossil fuel importing countries will remain perpetually vulnerable to commodity market shocks — a Sword of Damocles hanging over their economic stability. Renewable energy is not only a climate imperative; it is the only permanent solution for energy and economic security.

CORRECTION: This briefing note was amended on 19 May 2026 for two column labels on “Figure 1: Share of LNG (left) and crude oil (right) purchased from the Persian Gulf”. We regret the error.

Related Content