Key Findings

Producers have reduced their contracted volumes by 40% to 2034, highlighting the impact of shrinking thermal coal demand.

This reduction creates a supply-chain cost death spiral as lower volumes drive exponential increases in transport costs, placing further pressure on the economics of remaining mines.

Access to debt finance to fund coal production is increasingly costly and difficult.

These cost impacts should be a key consideration in future approvals for mine lease extensions and expansions.

The Hunter Valley Coal Network (HVCN) is the rail network that connects the coalmines of the Hunter Valley in NSW with the Port of Newcastle. The Australian Rail Track Corporation (ARTC) operates the network under a voluntary access undertaking (HVAU) between ARTC and the Australian Competition and Consumer Commission (ACCC). The undertaking defines the terms under which ARTC provides, and prices, access for the Hunter Valley coal producers (HVCP) to its rail network.

The HVAU expires at the end of the year, and ARTC recently submitted a proposal to extend it to the end of 2031. The HVAU defines the maximum revenue ARTC can recover from all users based on a combination of economic variables, including rate of return and depreciation.

Unlike previous extension applications, ARTC was unable to agree terms with HVCP beforehand. It therefore provides significant detail of ARTC’s views on the key risks facing the coal industry in NSW, in particular:

- Declining contract volumes

- The impact of tighter emission standards on future developments

- Increased financing costs for coal assets

- The cost death spiral that results from this combination.

Declining volumes

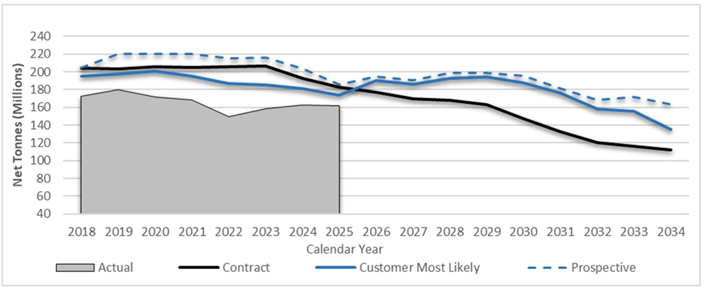

The rail network application charts contracted volumes since 2018 with forecasts and actuals to the end of 2034. Figure 1 highlights that contract volumes were constant at just above 200 million tonnes a year (MTPA) until 2023 and then decline by 40% to 2034.

Figure 1: Coal contract volumes vs prospective, probable and actual volumes (MTPA)

Source: Synergies Depreciation paper on the HVCN.

Figure 1 shows that actual production has been consistently lower than forecast, and always lower than contracted volumes. While producer forecasts may be optimistic, the contracted positions represent the production levels they are financially committed to deliver for export. These contracts demonstrate a clear trend that Hunter Valley coal is in significant volume decline.

More stringent environmental standards

ARTC says the NSW government’s Coal Industry 2026-2050 framework presents an increasing risk to future production, and hence the future utilisation of its rail network. In particular, ARTC cites the NSW government’s decision not to approve coalmine extensions without demonstrated emissions controls as an increasing risk to its rail volumes. These controls include assessment of Scope 1, 2 and 3 emissions as well as requirements for operational abatement to ensure any approval of an application aligns with the state’s net zero targets.

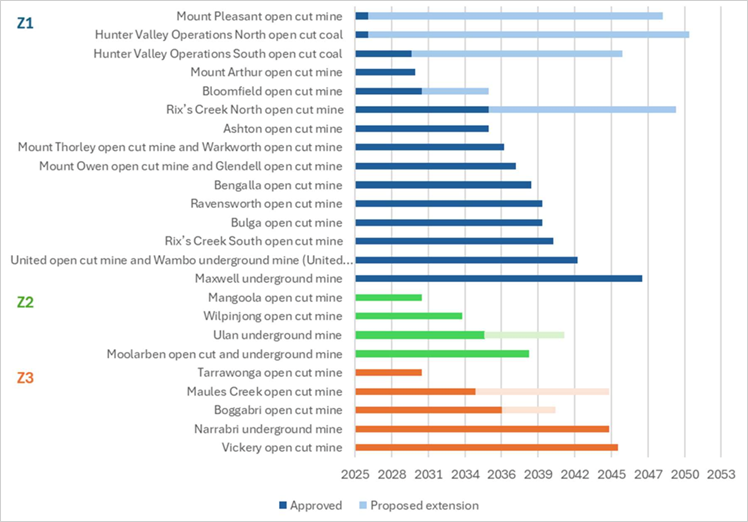

ARTC presents a timeline of lease approvals and extension applications, highlighting the importance of the application processes for the Hunter Valley Operations and Mount Pleasant mines, both of which have extension applications under consideration. This highlights that key mines in Pricing Zone 2 (on the Ulan rail line) will cease operations by 2034, based on the expiry of their mining licences.

Figure 2: Hunter Valley coalmine approvals pending and proposed extensions

Source: Synergies Depreciation paper on the HVCN. Note: The ARTC Network is separated into three pricing zones, with the approval timeline colour coded, Blue = Zone 1: Muswellbrook to the Port; Green = Zone 2: Muswellbrook to Ulan, and; Orange = Zone 3: Muswellbrook to Narrabri.

While individual contract details for specific mines are commercial in confidence and not detailed in the application, the contract decline profile would appear to assume that both Mount Pleasant and HVO applications are approved beyond 2026. However, should ARTC’s concerns that stricter environmental safeguards in the approval process risk future supplies are borne out by the rejection of these applications, the 40% decline in contract volumes could be optimistic.

Cost and access to debt finance

ARTC’s application highlights that the availability of finance for coal assets is declining and, if secured, the cost of that finance is increasing. ARTC is therefore seeking an additional 0.3% in its regulated rate of return to compensate for this increased cost of finance.

Volume-cost death spiral

The cost base for coal supply-chain infrastructure (such as the rail network and port loading terminals) is largely fixed and recovered from the contracted volumes transported on the network. That is, the access cost for coalminers using the network is equal to the total asset cost divided by the volumes transported. Therefore, as those volumes decline, costs rise, making it increasingly difficult to recover costs from the remaining contracted volumes, creating a “death spiral”, as ARTC says in its Explanatory Note:

“These price increases will potentially result in a further reduction in volumes as some of the remaining mines become uneconomic, resulting in further and compounding price increases arising from these reductions in volumes. […] Note: This effect is sometimes referred to as a death spiral.”

This highlights that the cost of infrastructure access is a function of future volumes and, as those volumes decline, costs will rapidly increase, potentially leading to further mine closures as production becomes uneconomic, and driving further cost increases for the remaining mines. This death spiral substantially increases the risk of stranded assets.

Key infrastructure assets are also owned by coal producers, such as the Newcastle Coal Infrastructure Group (NCIG) Terminal at the Port of Newcastle. Faced with a similar death spiral driven by the early closure of BHP’s Mount Arthur coalmine in 2030, the coal producer owners of NCIG were happy to take advantage of higher coal prices to accelerate debt repayments before the closure to avoid the impacts of lower volumes. Financial statements of coal producers indicate the impact of this debt acceleration alone will lower prices by as much as AU$9/tonne once it is removed. That ARTC was unable to reach a negotiated outcome with coal producers in respect of a depreciation mechanism consistent with market risks (i.e. a near-term depreciation premium to offset higher costs in future) suggests producers have profitability concerns due to the volume reductions. This, in turn, raises significant questions about the impact of this death spiral on future volumes falling below the already greatly reduced level of 40%.

Future process and considerations

Stakeholders have until 30 June to respond to an ACCC Issues Paper on ARTC’s application and its view of the risks to the industry. This will provide an insight into coal producers’ views of these risks, but for now, based on ARTC’s application, it appears, based on the evidence that:

- Hunter Valley coal volume commitments are rapidly diminishing.

- More stringent application of environmental requirements is a risk to future mine extension and expansion approvals.

- Finance for coal assets is harder to get and more expensive if secured.

- All of the above drive a cost death spiral that could accelerate further mine closures as remaining production becomes more uneconomic.

In particular, the cost death spiral should be considered in the NSW government’s approval of any mine extension or expansion application as it will likely accelerate mine closure timelines as they become less economic towards the end of their life. This, in turn, has implications for mine rehabilitation. At a minimum, this increased cost profile must be reflected in any cost-benefit analysis submitted as part of the application process.

Related Content