‘Golden age’ or energy dependence? Evaluating the Indonesia-US trade deal amid Middle East turmoil

Download Briefing Note

Key Findings

In February 2026, Indonesia and the United States (US) signed the Agreement on Reciprocal Trade (ART), which eliminated tariffs on 1,819 Indonesian products. However, an underlying clause obliges Indonesia to import approximately USD15 billion worth of US energy commodities annually, nearly half of its total oil and gas imports.

The risks embedded in the ART energy clause may constrain Indonesia’s energy planning flexibility and undermine its long-term energy security and economic resilience. They also expose the country to energy transition setbacks, fossil fuel price volatility, US policy dependence, reliance on a single partner, and higher costs from long-distance transportation.

The ART’s energy clause, combined with turmoil in the Middle East, heightens Indonesia’s vulnerability to external shocks. To safeguard national interests, Indonesia should balance short-term gains with long-term resilience by accelerating renewable energy development, expanding electric vehicle (EV) adoption, strengthening domestic clean energy supply chains, and diversifying its trade partners.

On 19 February 2026, Indonesia and the United States (US) signed an Agreement on Reciprocal Trade (ART) called the “Implementation of the Agreement Toward a NEW GOLDEN AGE for the US-Indonesian Alliance”. The agreement eliminates tariffs on 1,819 Indonesian products, facilitating greater access to the US market.

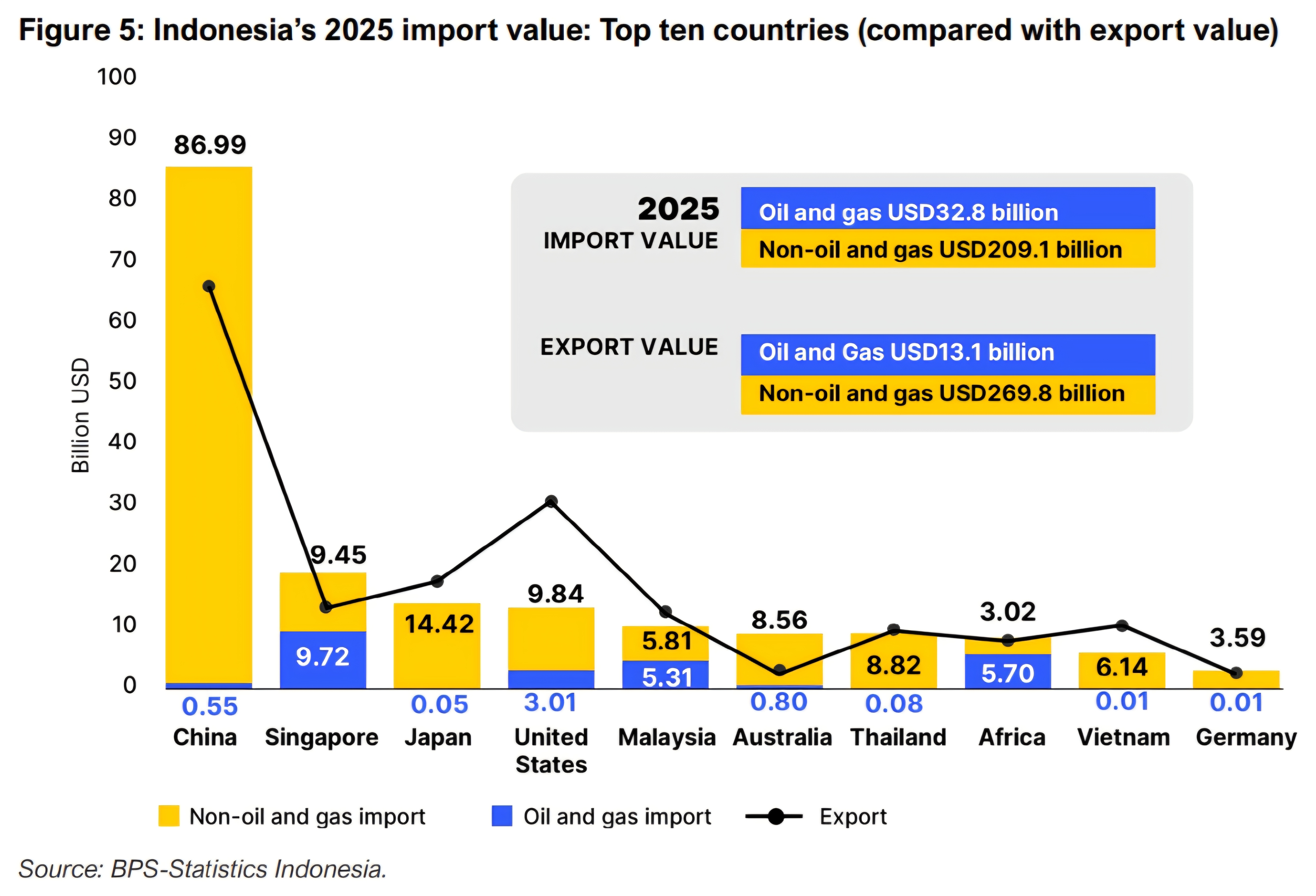

At first glance, the USD33 billion investment and trade deal appears mutually beneficial — Indonesia gains easier access to the world’s largest consumer market, and the US secures expanded commercial opportunities in Indonesia’s agriculture, aerospace, and energy sectors. However, an underlying clause could fundamentally reshape Indonesia’s energy trajectory. The agreement obliges Indonesia to import approximately USD15 billion worth of US energy commodities annually (approximately IDR253.2 trillion). This includes USD3.5 billion of liquefied petroleum gas (LPG), USD4.5 billion of crude oil, and USD7 billions of refined gasoline. In 2025, imports of these commodities cost Indonesia USD32.8 billion. A USD15 billion commitment would account for almost half of the country’s total oil and gas imports, significantly concentrating purchases with the US.

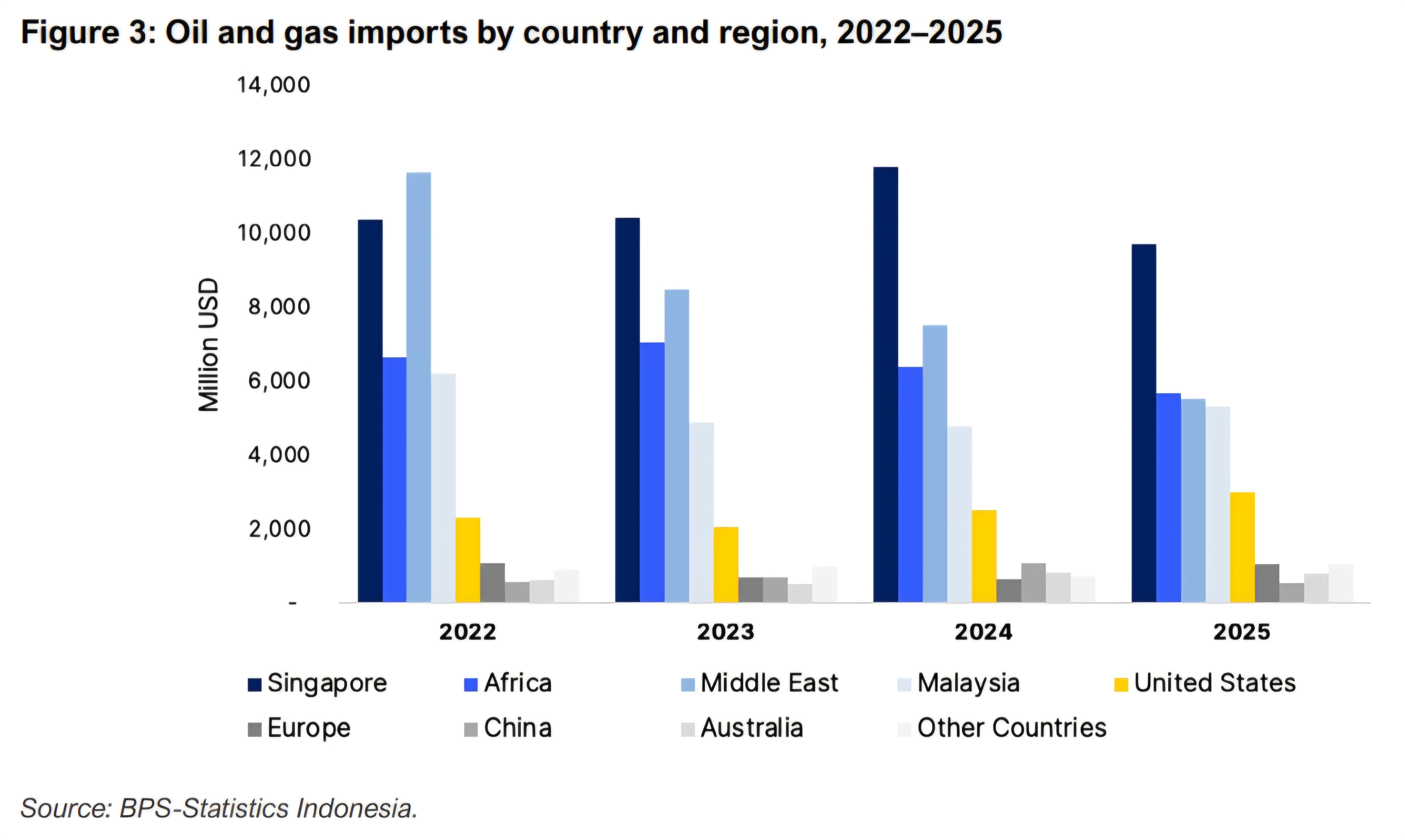

Following the outbreak of conflict in the Middle East, tankers in the Strait of Hormuz, through which roughly 30% of global seaborne crude shipments pass, have faced severe restrictions. According to ship-tracking data from Bloomberg, traffic through the Strait has fallen by over 95% and oil prices have jumped about 13% as of 2 March 2026. This disruption directly affects Indonesia, which in 2025 imported around US5.5 billion worth of oil and gas from the Middle East. In accordance with its obligation under the ART, Indonesia intends to replace these Middle Eastern supplies with US imports. This pivot may help mitigate short-term supply disruptions while allowing Indonesia to fulfil its trade commitments, and could also redefine the country’s energy trajectory. The ART energy clause could potentially increase the value of US oil imports by more than twelvefold.

Such a shift may secure physical import volumes, but it does not mitigate the cost impacts on Indonesia from global oil market prices. If oil prices remain elevated due to prolonged conflict and market volatility, US sellers may be incentivized to divert cargoes to other buyers offering more favorable terms, leaving Indonesia exposed to both price risks and supply competition.

Historical context of Indonesia’s oil and gas imports

Indonesia became a net oil importer in 2003, after domestic demand exceeded local production. Despite several noteworthy oil and gas discoveries between 2023 and 2024, oil production in the country continued to decline, dropping from 606 thousand barrels of oil per day (MBOPD) in 2023 to 580 MBOPD in 2024. This downward trend is primarily due to the diminishing output from many ageing wells and challenging technical factors, such as unplanned shutdowns in oil and gas production areas. Although crude oil demand also declined from 876 MBOPD in 2023 to 789 MBOPD in 2024, the gap between domestic production and demand still remains.

Under the current administration, the government has sought to increase domestic oil and gas production as part of efforts to reduce reliance on imports. In 2025, the country’s oil production rose by 4.3% to 605.3 MBPOD compared to the previous year. This marked the first production increase in the past nine years.

In January 2026, Indonesia inaugurated the Balikpapan Refinery Modification Project (RDMP Balikpapan), which is expected to boost oil processing capacity from 260,000 to 360,000 barrels per day. Additionally, the project will increase LPG production capacity to 336,000 tonnes per year, approximately 4% of current domestic LPG demand. This is a significant step toward localizing production of refined petroleum products. However, a supply-and-demand gap persists. This reality highlights the urgent need to accelerate electrification initiatives and diversify the energy mix to reduce reliance on fossil fuels.

The role of the US in Indonesia’s oil and gas imports

In 2025, Indonesia imported USD32.8 billion worth of oil and gas. The US import share was relatively small (approximately USD3 billion), with LPG as the dominant category.

Indonesia imported USD2.6 billion worth of LPG from the US in 2025, accounting for 69% of total LPG imports (USD3.8 billion). By contrast, crude oil imports from the US were minimal. Indonesia’s total crude oil import bill was USD8.3 billion, with Nigeria (USD2.4 billion), Angola (USD1.9 billion), and Saudi Arabia (USD1.6 billion) as the primary suppliers. Imports from the US totaled only USD367 million, or about 4% of total crude oil imports.

Similarly, Indonesia imported USD21.3 billion in refined petroleum in 2024, making it the 12th largest global importer. Refined petroleum was the country’s highest imported product that year. The bulk of supply came from Singapore (USD11.4 billion), Malaysia (USD4.4 billion), China (USD1.04 billion), Saudi Arabia (USD825 million), and India (USD755 million), with the US playing only a marginal role (USD16.1 million, equal to 0.075% of the total refined petroleum imports).

Evaluating the ART’s opportunities and risks

The ART presents several non-energy trade opportunities for Indonesia. Tariff-free access will make Indonesian goods more competitive in the US market, particularly in sectors such as textiles, footwear, and agriculture, potentially leading to significant increases in export volumes and revenues. The deal may also encourage greater US investment in Indonesia’s manufacturing and technology industries, creating jobs and facilitating knowledge transfer. The Agreement also strengthens Indonesia’s strategic import diversification by deepening ties with the US. Historically, Indonesia’s imports have been heavily dominated by China, reaching approximately USD87 billion, accounting for 36% of Indonesia’s total imports.

Risks to Indonesia’s energy security and economic resilience

Amid ongoing uncertainty and disruptions in the Middle Eastern energy supply chains, the ART offers Indonesia an opportunity to reduce exposure by increasing imports from the US. However, the risks embedded in the Agreement’s energy clause may constrain Indonesia’s energy planning flexibility and undermine its long-term energy security and economic resilience.

Indonesia has been striving to strengthen energy security through the expansion of renewable energy, as stated in the Electricity Supply Business Plan (RUPTL 2025–2034), by accelerating its electric vehicle (EV) push, advancing electrification, improving energy efficiency, and establishing a foundation for national and international carbon markets. Oil and gas imports have been declining as part of this effort. In 2022, the crude oil import bill was USD40.4 billion. By 2025, the import value fell by around 19% to USD32.8 billion, underscoring Indonesia’s effort to achieve greater energy independence.

The ART could reverse this trajectory. Under the Agreement, total oil and gas imports from the US are expected to rise to USD15 billion annually, an increase of more than fivefold from 2025, signaling a dramatic shift toward US dominance in Indonesia’s energy supply. By committing to this substantial yearly import, Indonesia risks undermining its efforts to achieve energy independence, while disproportionately increasing its dependence on a single country and shifting away from other suppliers.

Depending on oil and gas supply from a single partner increases vulnerability to external shocks. This risk has several dimensions that require assessment:

- Energy transition setback

Indonesia is currently pursuing energy efficiency, transport electrification, and accelerated renewable energy development to reduce oil demand and import dependence. However, the ART risks locking the country into continued fossil fuel reliance, hindering progress toward the RUPTL 2025–2034 targets, which include increasing the share of renewables to 74% and a 100-gigawatt (GW) solar program. It could also undermine Indonesia’s EV expansion strategy and its ambition to become a regional EV manufacturing hub if the domestic energy sys tem does not align with global sustainability standards.

- Price volatility and supply chain vulnerability

Global oil and gas prices are characteristically volatile, influenced by geopolitical tensions, climate-related factors, shipping bottlenecks, OPEC+ (consisting of the Organization of the Petroleum Exporting Countries [OPEC] members and other oil-producing countries) decisions, and supply disruptions. This volatility is clearly observed by the US-Israel war with Iran, which has caused oil and gas prices to surge. On 2 March 2026, the Brent crude international benchmark rose to USD82 a barrel, marking a 14-month high. Europe's benchmark gas price also increased by 50% before closing 39% higher. Locking in large oil and gas import volumes will likely expose Indonesia to external shocks and fluctuating global energy prices.

- US policy dependency and single partner reliance

Under the Agreement, Indonesia’s economic gains would depend on US trade policy, which could fluctuate within the current and future administrations. What looks like a golden age today could quickly become a liability tomorrow. Moreover, relying on a single partner for Indonesia’s energy supply would constrain strategic flexibility and undermine bargaining power, increasing exposure to asymmetric trade dynamics.

- High costs

Importing large volumes of oil and gas across the Pacific would entail substantial logistical and shipping expenses for Indonesia. Historically, crude oil sourced from the US has also been more expensive than that from other suppliers. In 2025, the average import cost of US crude oil was approximately USD0.54 per kilogram (kg) or about USD72.5 per barrel. This is higher than the import cost from Saudi Arabia (USD69.9 per barrel) and Indonesia’s overall average crude oil import cost in 2025 (USD70.6 per barrel). These higher costs, compounded by long-distance transportation expenses, are likely to strain Indonesia’s trade balance and reduce the competitiveness of imported energy compared to domestic production or regional alternatives.

Strategic considerations for Indonesia

Indonesia stands at a critical crossroad in its energy and trade policy, particularly in light of the global shock triggered by the ongoing Middle East conflict. The challenge extends beyond contracts with other countries: it is about ensuring Indonesia’s energy future is independent, diverse, stable, and sustainable rather than reliant on a partner. To safeguard national interests, Indonesia should adopt a comprehensive strategy that balances short-term gains with long-term resilience:

1. Accelerating renewable energy development

Indonesia should leverage its abundant solar, wind, geothermal, and hydropower resources to reduce reliance on imported hydrocarbons. Renewables primarily have upfront costs with minimal operating expenses, while fossil fuels are constantly exposed to ongoing, unpredictable price volatility. Expanding renewable capacity would strengthen energy independence and reduce the impact of dollar-denominated market-based fluctuations in global fossil fuel markets. Incentivizing private investment, streamlining permitting and procurement process. es, and scaling up grid integration would be critical to unlocking Indonesia’s renewable energy potential.

2. Reducing refined gasoline imports through EV expansion

The largest share of Indonesia’s energy imports is sourced from refined gasoline. To reduce this dependency, the country should accelerate the development of its EV ecosystem, as electrifying transportation would directly reduce refined gasoline demand. Scaling EV adoption is essential. Indonesia has set targets of 2 million electric cars and 13 million electric motorcycles by 2030, supported by a nationwide charging infrastructure.

The country’s electric vehicle count has surged in recent years. By 2025, the total reached 333,561 units, up from just 3,894 units in 2020. Two-wheeled EVs dominated with 225,647 units, while four-wheeled passenger EVs accounted for 106,137 units. However, there is still a significant gap compared with national targets, underscoring the need for stronger policy support and faster adoption.

3. Strengthen domestic industry for renewable energy and EV supply chains

Indonesia should build a strong domestic capacity in renewable energy and EV supply chains for energy security. Expanding local manufacturing of solar panels, wind turbines, and batteries will reduce reliance on imports. Developing a skilled workforce and modernizing infrastructure, such as the power grid and EV charging networks, are equally important to sustain long-term growth. This would require coordinated action across policy, investment, and infrastructure to attract financing.

4. Maintain diversity among trade partners

As the energy transition progresses, Indonesia should maintain a variety of trade relationships to avoid overdependence on the US market. A diversified portfolio of partners enhances bargaining power, stabilizes supply chains, and reduces exposure to policy shifts in any single country.

Conclusion: A complex trade-off

Indonesia’s challenge lies in leveraging the benefits of US market access while safeguarding its energy security, without allowing trade to delay or derail the country’s energy transition. Without careful policy management, the ART could leave Indonesia more exposed than empowered. The government should act decisively by investing in renewables, strengthening domestic industries, and diversifying trade partners to ensure the promise of a “new golden age” remains a reality.

The current turmoil in the Middle East highlights the urgency of Indonesia’s energy security challenge. Recent geopolitical conflicts have already driven oil and gas price to multi‑year highs, underscoring Indonesia’s vulnerability to external shocks if the country remains heavily dependent on imported fossil fuels. Indonesia’s future energy landscape should not be shaped by the terms of a single trade agreement, but by the country’s ability to harness renewable resources, build resilient infrastructure, and chart an independent course in a volatile global energy market. The stakes are high, and energy security is not just an economic issue but a cornerstone of national sovereignty.

Related Content