Key Findings

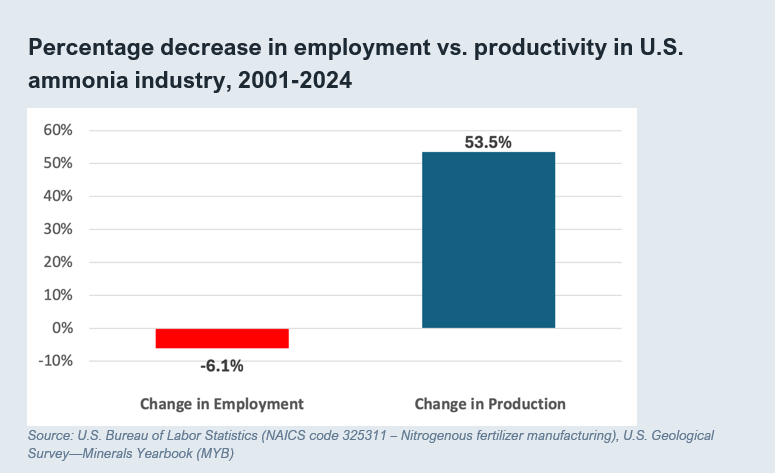

Ammonia build-out would likely have only a limited impact on local jobs, as the ratio of jobs per unit of ammonia production has plummeted—from 2001-2024, production rose by 53.5% while the number of direct jobs dropped by 6.1%.

Rising construction costs and operational expenses, together with market uncertainty, pose financial risks—and have even led to cancellation of some large ammonia projects.

Domestic agriculture is not driving ammonia expansion in the United States—demand is relatively flat, and the United States already produces most of the ammonia used for current domestic purposes.

The U.S. ammonia industry faces multiple challenges and risks in building out ammonia production intended for export to a global energy market that will likely be limited.

Executive Summary

Federal, state, and local agencies have been awarding financial incentives for construction of ammonia production plants that may fail to achieve robust economic benefits for host communities.

Government agencies typically justify awarding tax incentives, grants, or other support based on company predictions that a project will produce a large number of jobs and bolster the local economy. Some support is based on hopes that ammonia will play a big role in energy markets.

This report explains why ammonia production is constricted as a job engine; why energy markets for ammonia will not likely be robust; and why public monies and tax benefits should not be invested in ammonia given the risks of such enterprises. IEEFA’s analysis finds:

- Ammonia build-out would likely have only a limited impact on local jobs: The ratio of jobs per unit of ammonia production has plummeted. From 2001-2024, ammonia production rose by 53.5% but the number of direct jobs dropped by 6.1%.

- Rising construction costs and operational expenses, together with market uncertainty, pose financial risks—and have even led to cancellation of some large ammonia projects.

- Domestic agriculture is not driving the ammonia expansion in the United States. Demand is relatively flat, and the United States already produces most of the ammonia used for current domestic purposes.

- The U.S. ammonia industry faces multiple challenges and risks in building out ammonia production intended for export to a global energy market that will likely be limited.

Meanwhile, ammonia production and transport pose community safety issues that present financial risks to the industry and policy pitfalls for government economic development strategies. Roughly 57% of U.S. ammonia production is concentrated in just three states: Louisiana, Oklahoma, and Texas. The communities targeted to bear the burden of the ammonia production build-out are likely to experience fewer economic benefits than expected and lower tax revenues due to government incentives to private industry—in exchange for increased public health and safety risks.

Related Research