Potential drivers of carbon price formation in the CCTS: Design and market dynamics in the Indian carbon market

Download Full Report

View Press Release

Key Findings

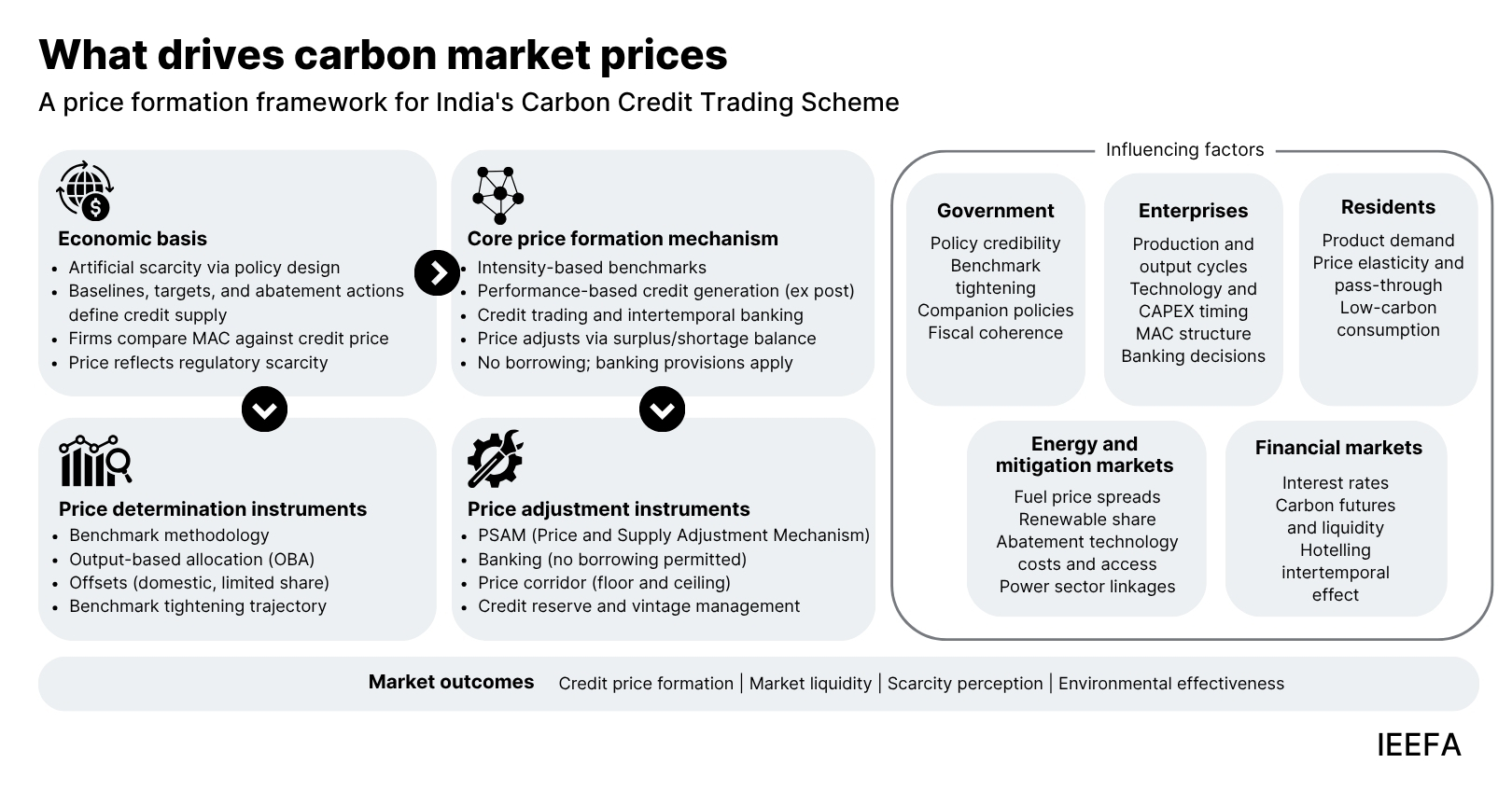

In India's intensity-based system, output growth can generate both credit supply and credit demand depending on which firms drive growth. This makes benchmark calibration the central mechanism for shaping the price signal. Output-based allocation also mutes the transmission of carbon costs into product prices, weakening demand-side signals even when the carbon price is positive. Credible, pre-committed tightening trajectories and rule-based supply adjustment mechanisms are essential to sustain scarcity.

Covered sectors differ meaningfully in abatement options, capital cycles, trade exposure, and ability to pass through carbon costs. The power sector's initial exclusion removes the single largest emission source, the primary fuel-switching channel, and a class of participants that trade continuously. Future integration will need to address how carbon costs interact with India's electricity regulatory framework, particularly dispatch and merit-order decisions. Without a credible integration roadmap, the CCTS will lack the primary channel through which carbon pricing shapes energy investment.

Instruments such as ESCerts, RCOs, PLI schemes, and the National Green Hydrogen Mission affect emissions in covered sectors independently of the carbon price. Without periodic baseline revisions reflecting their cumulative impact, the resulting surpluses can depress prices and blur what the CCTS price signals about in-sector abatement costs. International experience, particularly the EU-ETS waterbed effect, underscores the importance of dynamic baseline revision and unified registries to prevent double counting.

Ex-post credit issuance, the exclusion of financial intermediaries, and capital-intensive industrial abatement mean both supply and demand will remain relatively inelastic in the early years, with trading likely to cluster around settlement deadlines. Communicating clear long-term targets and a predictable path for benchmark tightening is particularly important given that industrial investment decisions span 15 to 30 years. Forward guidance and well-designed stability mechanisms can help firms integrate carbon costs into long-term planning.

This report analyses how carbon prices will take shape in India’s forthcoming Carbon Credit Trading Scheme (CCTS), an intensity-based emissions trading system covering energy-intensive industries.

Price formation in the CCTS reflects the interaction of regulatory design, firm-level abatement decisions, macroeconomic conditions, and companion policy dynamics. These forces interact through feedback loops that will determine whether the CCTS produces a carbon price capable of guiding the capital-intensive, long-term investments that India’s industrial decarbonisation requires.

Supply, demand, and the role of benchmark design

The CCTS regulates emissions intensity rather than imposing an absolute cap like in the European Union-Emissions Trading System (EU-ETS), meaning aggregate allowable emissions will scale with output. This accommodates India’s industrial growth trajectory but creates a structural tension at the heart of price formation. Output expansion simultaneously generates carbon credit supply from efficient firms outperforming their benchmarks, and credit demand from less-efficient firms falling short. Whether the market tightens or loosens in any period depends on which firms are driving growth and how regulators calibrate benchmarks relative to realised sectoral performance. Output-based allocation (OBA) also mutes the transmission of carbon costs into product prices, weakening demand-side signals for material efficiency and substitution even when the underlying carbon price is positive.

As the system issues credits only after verified performance against facility-level benchmarks, tradable supply enters the market with a lag. Banking behaviour, verification timelines, and firms’ willingness to sell all create a gap between what the system can generate and what reaches the market. This makes benchmark design the primary lever through which regulators control scarcity. In jurisdictions where benchmark-setting has relied too heavily on industry-provided estimates without independent verification, allocations have consistently been more generous than necessary.

Credible scarcity requires pre-committed tightening trajectories reinforced by transparent, rule-based supply adjustment mechanisms. The EU-ETS recovered meaningful price signals only after structural reforms, notably the Market Stability Reserve (MSR), replaced ad-hoc interventions with automatic supply correction. India’s CCTS will need equivalent mechanisms to anchor expectations and sustain the forward-looking participation that stable price signals depend on.

Power sector, liquidity, and energy price transmission

The strength of these price signals depends not only on benchmark design, but also on who participates in the market and how actively they trade. The initial exclusion of the power sector is pragmatic but narrows both dimensions considerably. It removes the single largest source of carbon emissions and eliminates the fuel-switching channel, specifically the coal-gas merit-order dynamics that have been among the strongest determinants of allowance demand in systems like the EU-ETS. It also removes utilities, which are a class of participants that in other markets trade continuously to hedge emissions exposure alongside energy prices. Demand concentrates instead among industrial firms whose compliance requirements evolve more slowly and whose trading may cluster around settlement deadlines, weakening the informational content of periodic market-clearing prices.

Any future power sector integration will need to address the statutory tariff determination process under the Electricity Act 2003, which lacks an established framework for treating carbon compliance costs as a legitimate, automatic pass-through. Carbon cost recognition would need to be coordinated across the Central Electricity Regulatory Commission (CERC) and state electricity regulatory commissions (SERCs) to avoid competitive distortions between generators and inconsistent price signals across states. The power sector also differs from typical Emissions-Intensive Trade-Exposed (EITE) sectors in that it faces limited carbon leakage risk given its largely domestic nature. This creates a different set of design questions over time, including how allocation approaches might evolve, and how any associated revenues could be deployed in ways that support the broader energy transition, including the financial sustainability of the distribution segment.

That said, without a credible integration roadmap, the CCTS will continue to operate without the primary transmission channel through which carbon pricing shapes energy investment decisions.

Companion policies and early-stage market conditions

The absence of the power sector in CCTS places greater weight on industrial sectors covered therein to sustain meaningful compliance demand, and on companion policy coordination to preserve the integrity of the carbon price signal. Instruments such as the Perform, Achieve and Trade (PAT) scheme, Renewable Consumption Obligations (RCO), Production-Linked Incentives (PLI) schemes, and the National Green Hydrogen Mission directly affect emissions intensity and output decisions in the sectors covered. When these policies reduce emissions independently of the carbon price, they lower compliance demand and create surpluses without any change to CCTS baselines. If baselines are not periodically revised to reflect these effects, it results in a price depression, blurring what the CCTS price signals about in-sector abatement costs. The risk is compounded when firms receive overlapping subsidies alongside carbon credit revenue, potentially driving their net marginal abatement cost below zero and shifting investment decisions away from the carbon price signal entirely.

These coordination challenges intersect with structural market conditions that are inherently difficult in the formative years. Both supply and demand are likely to remain relatively inelastic. Industrial abatement is large and uneven and capital-intensive, short-run fuel-switching options are limited. Production decisions are governed by asset cycles rather than marginal carbon costs.

The initial exclusion of financial intermediaries, who account for roughly 65% of secondary market activity in the EU-ETS, further constrains liquidity and continuous price discovery. In this scenario, even small differences between benchmark stringency and actual reductions can lead to significant Potential drivers of carbon price formation in the CCTS 10 price fluctuations. This uncertainty makes it difficult for firms to incorporate carbon costs into their investment decisions over the next 15–30 years.

This report also lays the analytical groundwork for subsequent work on international market linkages, Article 6 engagement, and the design of price and supply adjustment mechanisms (PSAM) for the CCTS.

Related Content