Key Findings

India’s compliance carbon market under the Carbon Credit Trading Scheme (CCTS) is into its operational phase. What determines its trajectory now are design choices on sequencing; and the window to shape them is before path dependencies harden. Priority should be given to foundational elements, including credible stringency, robust monitoring, reporting and verification (MRV) systems, and genuine enforcement. More advanced features should be designed early but introduced only as the market matures.

Every major emissions trading system has begun with compliance entities only, and the CCTS is well placed in doing the same. Financial intermediation is what eventually turns a compliance market into one with continuous price discovery and hedging. The legal framework for it already exists in India and can be designed into the system now for activation once the market’s foundations are established.

The power sector's exclusion from the initial phase of CCTS simplifies implementation while recognising the complexities of electricity market regulation. As the scheme evolves, future integration will call for a view of where carbon pricing fits among the measures available for the sector, alongside careful consideration of electricity market regulation, dispatch decisions, cost recovery mechanisms, and regulatory coordination, drawing on international experience.

Irrespective of the ongoing international discussions around the European Union’s Carbon Border Adjustment Mechanism (CBAM), a credible domestic carbon market can strengthen India’s long-term industrial competitiveness. International experience points to the design choices — from benchmark calibration to the eventual role of auctioning — that shape how much carbon value is recognised and retained at home, as options to weigh over time.

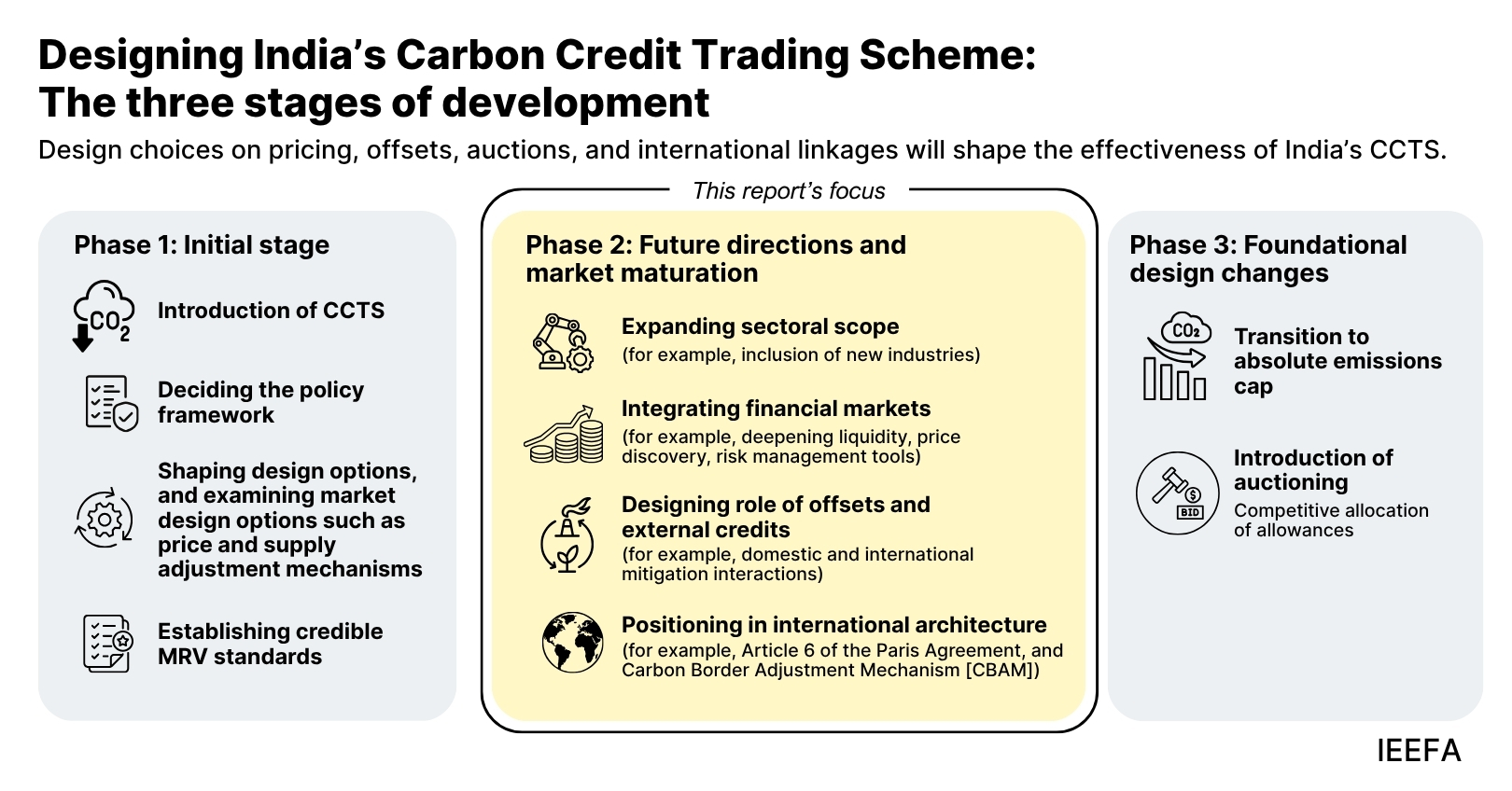

Executive summary

India’s Carbon Credit Trading Scheme (CCTS) is entering a decisive period. With compliance obligations now in effect, the initial architecture of the market — comprising intensity-based targets, baseline-and-credit allocation framework, facility-level benchmarks, and a price corridor — has been laid down. The next phase will now be defined by more consequential questions. How will the market deepen its liquidity and attract the participants needed for robust price discovery? How can the power sector, which accounts for roughly 40% of national emissions, be brought within the compliance boundary without creating new conflicts with electricity tariff regulation? What role should offset mechanisms and international carbon credits play, and at what point? How should baselines evolve as companion policies independently reduce emissions in covered sectors? And how should India position the CCTS to withstand scrutiny under the European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM) while advancing its own strategic interests under Article 6 of the Paris Agreement?

These are not hypothetical questions, but design choices that regulators, policymakers, and market participants will confront over the next two to five years. The answers will determine whether the CCTS produces a carbon price signal strong enough to guide capital-intensive industrial investment over 15- to 30-year horizons, or whether it settles into an administrative compliance exercise with limited influence on India’s decarbonisation trajectory.

This paper serves as a knowledge repository that identifies, discusses, and attempts to answer some of these critical and pertinent questions confronting the design, governance, institutional architecture, and international positioning of India’s compliance carbon market. It does so at a moment when regulatory choices are actively being shaped, path dependencies have not yet hardened, and India retains the advantage of learning from the costly missteps of earlier movers.

The analysis is organised around four themes. On financial market participation, it examines when and how financial intermediaries — whose presence will be critical to improve liquidity and continuous price discovery — can be brought into the market through well-designed market-making rules and oversight, drawing on evidence that such participants account for roughly 65% of secondary market activity in the EU Emissions Trading System (ETS). On power sector integration, it analyses the regulatory and institutional conditions required to embed carbon costs into dispatch and merit-order decisions within India’s statutory tariff determination process, without requiring full retail price pass-through. Recent reforms in the Republic of South Korea have demonstrated that such an approach is both feasible and consequential. On international dimensions, the report assesses how India’s domestic carbon price interacts with the EU’s CBAM, and what the country must do to establish a credible equivalence claim. Lastly, it looks at how the emerging Bharat Methodologies under the offset mechanism could be used for Article 6 cooperation as bilateral agreements take shape.

These four themes represent some of the most consequential open design questions facing the CCTS. Without financial intermediation, the scheme will struggle to produce the continuous, forward-looking price signal that industrial firms need to justify capital commitments spanning decades. Without power sector integration, the market would operate without its largest potential source of compliance demand and exclude the sector where carbon pricing has the most immediate effect on dispatch and investment decisions. Without deliberate alignment between the CCTS design and CBAM’s deduction framework, the architecture mismatch between India’s intensity-based system and CBAM’s per-tonne carbon cost logic could prevent domestic compliance efforts from being translated into meaningful deductions at the EU border. This would leave exporters exposed to the full CBAM liability even as they bear costs under the domestic scheme. And without a deliberately sequenced offset policy, cheap external credits could flood the compliance market before a credible carbon price has been established, while India’s most valuable international asset — the ability to authorise and sell high-integrity carbon credits under Article 6 — goes underleveraged.

In each case, the foundations of a functioning market must come first: Credible stringency; robust monitoring, reporting, and verification (MRV); and genuine enforcement. More advanced features should be designed early but activated only once the foundations are holding firm. The window for shaping these choices is now, before path dependencies harden and the costs of correction rise.

Throughout, the report draws on the conceptual and empirical foundations established in the two preceding papers in this series. The first paper, ‘Strengthening India's carbon market’ (October 2025), argued that CCTS should embed a price or supply adjustment mechanism — comprising consignment auctions, vintage-based credit classification, and a price corridor — from the outset. Drawing on evidence from the EU ETS, Alberta's Technology Innovation and Emissions Reduction (TIER) system, and Australia's Safeguard Mechanism, it showed that delayed intervention invariably proves costlier and more politically contentious than preventive design. The second paper, ‘Potential drivers of carbon price formation in the CCTS’ (June 2026), mapped the supply, demand, and institutional forces that will shape India's carbon price. It identified benchmark calibration, power sector exclusion, companion policy interactions, and early-stage liquidity constraints as the primary determinants of whether the market produces a credible and investment-grade signal. This third and final paper builds on both to examine the questions that will define the CCTS's next phase of evolution and its long-term viability as the centrepiece of India's climate policy architecture.

Related Content