Getting the price signal right early is key to the credibility of India’s carbon market: IEEFA

New report examines how benchmark calibration, power sector sequencing, and companion policy coordination will shape price formation in the Carbon Credit Trading Scheme.

Key Takeaways:

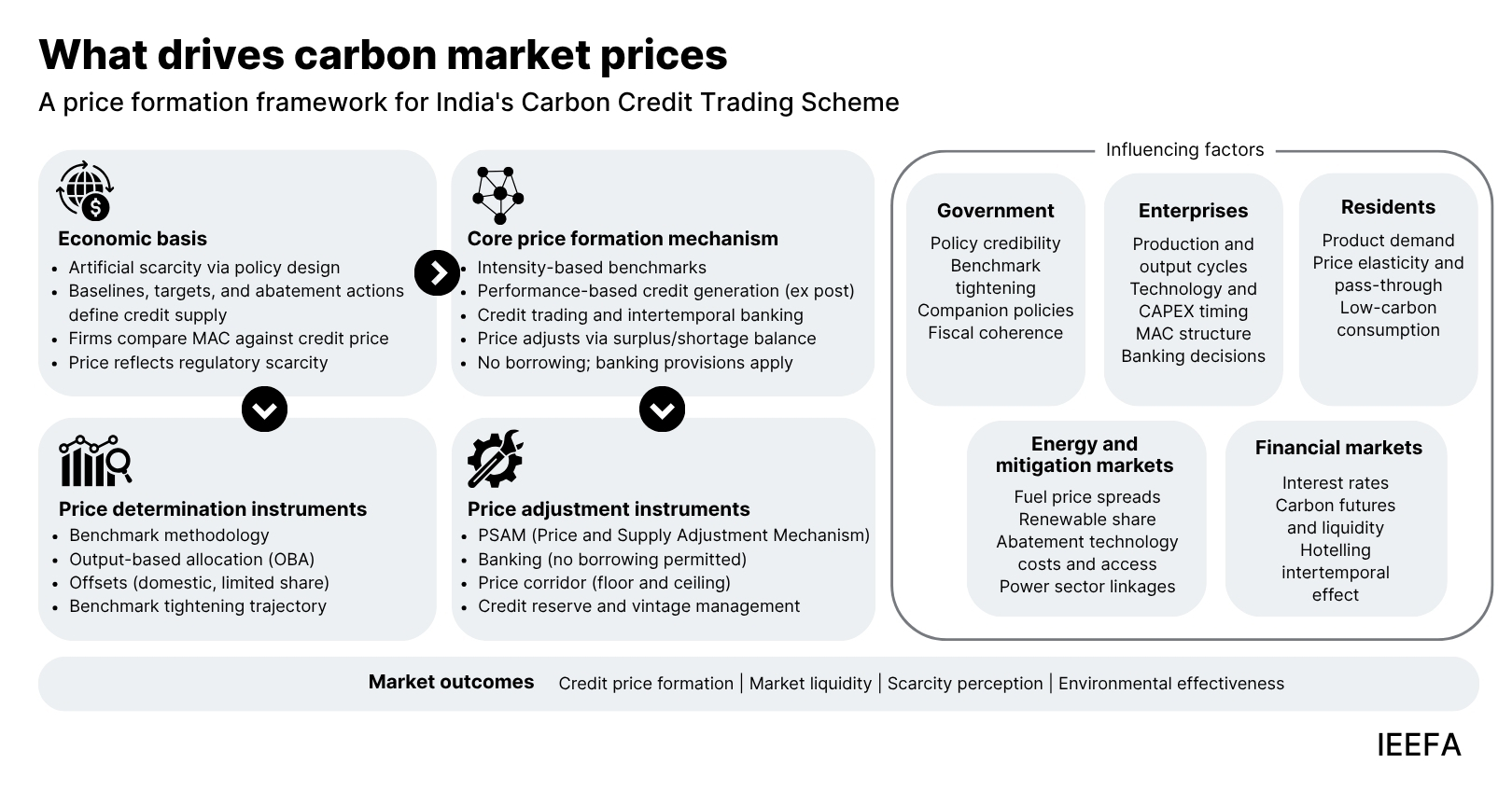

In India’s intensity-based targets and baseline and credit issuance, the relationship between output growth and market scarcity is more nuanced than in absolute cap systems. As production expansion can generate either credit supply or credit demand, benchmark design and calibration play a central role in shaping the price signal over time.

Understanding the distinct profiles of covered sectors will be central to how the Carbon Credit Trading Scheme (CCTS) develops, and sequencing decisions offer an opportunity to build the market thoughtfully over time. Sectors differ meaningfully in their abatement options, capital replacement cycles, exposure to international competition, and ability to pass carbon costs through to product prices.

Early-stage market dynamics in any emissions trading system tend to reflect a period of learning, and India’s CCTS is likely to be similar. Factors such as ex-post credit issuance, the gradual development of trading participation, and the capital-intensive nature of industrial abatement suggest that liquidity and price discovery will evolve over successive compliance cycles.

Communicating clear long-term targets and having a predictable path for benchmark changes are particularly important as industrial investment decisions often span 15–30 years and require confidence in the durability of the price signal.

4 June 2026, IEEFA: As India begins to operationalise its carbon market under its Carbon Credit Trading Scheme (CCTS), a new report by the Institute for Energy Economics and Financial Analysis (IEEFA) examines the market dynamics and design choices that will shape how the scheme produces a carbon price signal that can guide industrial decarbonisation in India.

The report, titled ‘Potential drivers of carbon price formation in the CCTS: Design and market dynamics in the Indian carbon market’, analyses how carbon prices will take shape in India’s intensity-based emissions trading system, covering seven sectors and 490 obligated entities in its first compliance cycle. The report draws from the experience of emissions trading systems and programmes in the European Union (EU), South Korea, China, and California in the United States. It identifies how India’s specific design choices create market dynamics in need of careful navigation in the early stages.

“India’s CCTS reflects a pragmatic approach to carbon market design. It accommodates industrial growth while building on existing institutional capabilities,” says Saurabh Trivedi, report author and Lead Specialist, Sustainable Finance & Carbon Markets - South Asia, IEEFA. “Understanding how these design features interact with India’s economic and regulatory context is essential for the scheme to fulfil its potential as an instrument for industrial decarbonisation.”

One of the report’s main findings concerns benchmark calibration. As the CCTS is intensity-based, allowable emissions scale with output, meaning credit supply and demand can both rise simultaneously depending on which firms drive growth. Benchmark design is therefore the primary lever through which regulators will control scarcity. The report notes that transparent, rules-based benchmark methodology and independent verification alongside industry data will be important in navigating this dynamic effectively.

The report also examines the implications of initially excluding India’s power sector, a large source of carbon emissions. In other carbon markets, power utilities are among the most active participants, and fuel-switching dynamics between coal and gas are among the strongest drivers of carbon price movements. Their initial absence will concentrate compliance activity among industrial firms, narrow liquidity, and limit the transmission channel through which carbon pricing most directly shapes energy investment decisions.

“The phased approach to power sector inclusion reflects the importance of working through how carbon costs interact with India’s electricity regulatory framework,” says Subham Shrivastava, report author and Climate Finance Analyst - South Asia, IEEFA. “South Korea’s experience, where reforms from 2022 progressively embedded carbon costs into dispatch decisions even where retail price pass-through remained constrained, illustrates how this integration can be sequenced thoughtfully. A clear roadmap, developed with India’s tariff determination process in mind, would strengthen the scheme’s long-term foundations.”

A further finding concerns the interaction between the CCTS and companion policies including the Perform, Achieve, Trade (PAT) scheme, Renewable Consumption Obligations (RCOs), Production-Linked Incentives (PLI) scheme, and the National Green Hydrogen Mission. Each independently affects emissions in covered sectors. Without periodic baseline revision accounting for their cumulative impact, these instruments risk generating credit surpluses that weaken the market signal, replicating dynamics that undermined the EU scheme’s early price formation.

On early market conditions, the report notes that both supply and demand are likely to remain relatively inelastic in the scheme’s formative years. Industrial abatement in sectors such as steel, cement, and aluminium is capital-intensive and tied to investment cycles of 15–30 years, leaving firms with limited room to respond quickly to price signals.

With financial intermediaries—who account for roughly 65% of secondary market activity in the EU scheme—initially excluded, the market will also have fewer participants to provide liquidity and absorb short-term fluctuations. The report recommends that supply adjustment mechanisms, forward guidance on benchmark tightening, and clear banking rules be built into the scheme’s architecture from the outset, so that stabilising features are in place as the market develops.

“Industrial firms are making capital allocation decisions today that will shape their emissions profiles through the 2030s and beyond,” says Saloni Sachdeva Michael, report author and Lead Energy Specialist, India Clean Energy Transition - South Asia, IEEFA. “Building the CCTS’s credibility in its early years through predictable rules, transparent tightening trajectories, and well-coordinated policy design will be essential to ensuring the scheme fulfils its role in India’s decarbonisation journey.”

Read the report: Potential drivers of carbon price formation in the CCTS: Design and market dynamics in the Indian carbon market

Media contact: Prionka Jha ([email protected]); +91 9818884854

Author contacts: Saurabh Trivedi ([email protected]), Subham Shrivastava ([email protected]), Saloni Sachdeva Michael ([email protected])

About IEEFA: The Institute for Energy Economics and Financial Analysis (IEEFA) examines issues related to energy markets, trends, and policies. The Institute’s mission is to accelerate the transition to a diverse, sustainable and profitable energy economy. (ieefa.org)