LNG exports and U.S. power price

Key Findings

Rising international market exposure increases price volatility, boosting consumer risk.

The U.S. Energy Information Administration’s monthly Short-Term Energy Outlook provides insights into how it expects domestic energy prices and fuel consumption to play out over the next 12-to-24 months. A key topic for EIA this year has been the threat that liquefied natural gas (LNG) exports will raise the cost of electricity and home heating for U.S. consumers, with the data agency warning every month about the impact of LNG exports.

The growing connection between LNG exports and electricity markets in the U.S. is happening because of two long-term trends.

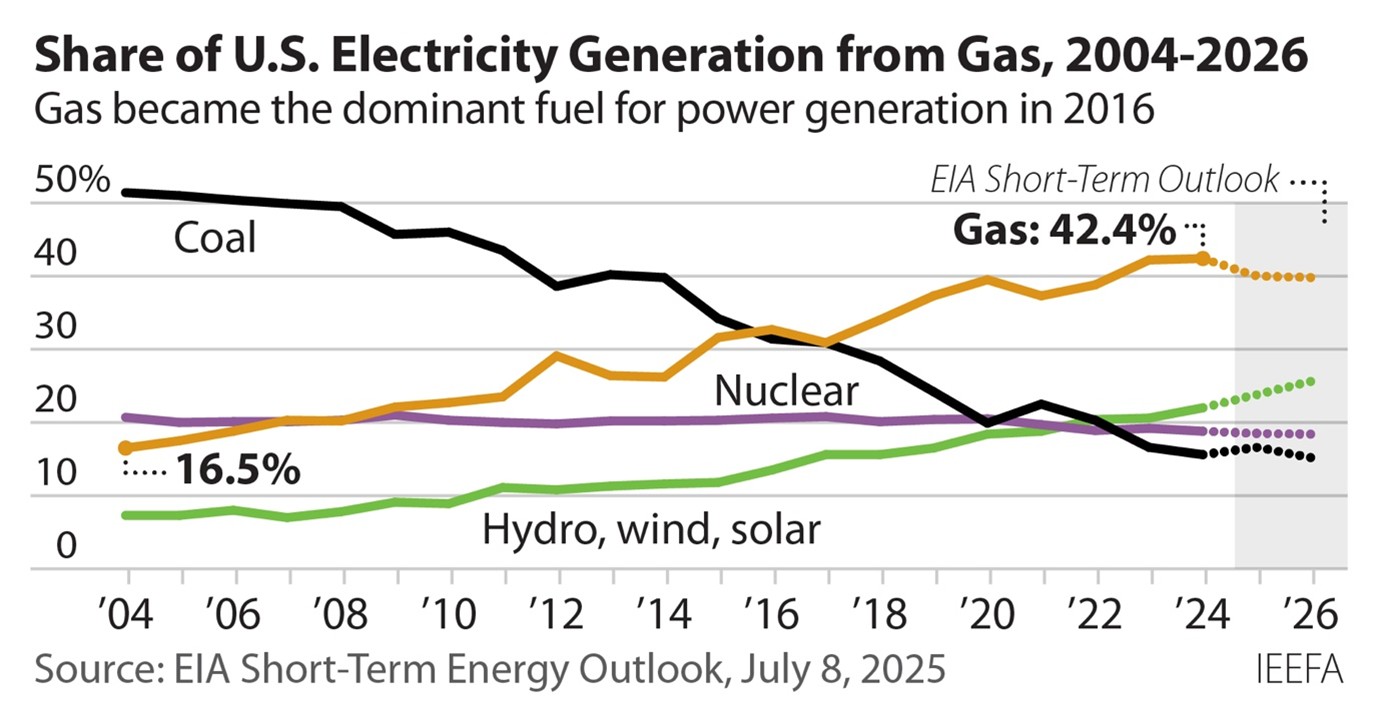

First is the dominant role of gas in electricity generation. Twenty years ago, in 2004, just 16.5% of U.S. electricity was generated using gas, far behind coal (51.4%) or nuclear (20.7%). That balance has shifted dramatically in the years since the fracking boom vastly increased supply while generally lowering and stabilizing prices. In 2016, gas surpassed coal as the leading fuel for producing power, and by 2024, 42.4% of the country’s electricity was generated using gas. Coal had slipped to just 15.6%, behind both nuclear (18.8%), and wind and utility-scale solar (16.2%).

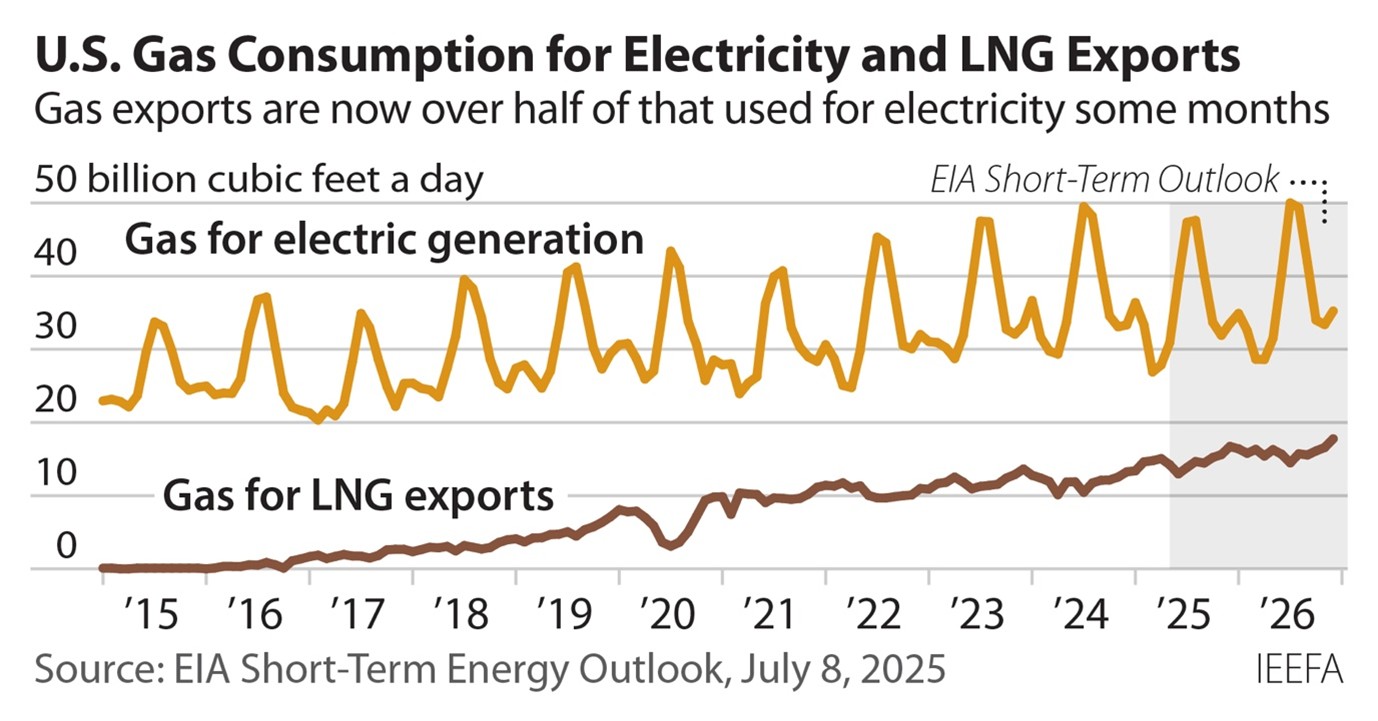

Second, the surge in U.S. gas production also enabled a new option: exporting LNG in specialized cargo ships to global markets. Huge new export facilities have been built, mostly along the Gulf Coast, and more export projects are under construction or in planning. In 2014, LNG exports were a tiny 0.06% of U.S. dry gas production, amounting to just 44.5 million cubic feet per day. By 2024, that had soared to 11.9 billion cubic feet per day (bcf/d), or 11.6% of production, and it is expected to keep rising as additional LNG export facilities come online over the next several years. In March and April, for the first time, the amount of gas going to LNG exports totaled more than 50% of the amount of gas being used to produce electricity in the U.S.

EIA now says, “Higher natural gas prices in 2025 and 2026 are the result of strong export growth that persistently outpaces U.S. natural gas production.” In other words, the high demand for gas exports is also pushing up the price of the gas that supplies 40% of U.S. electricity—a cost that will be passed on to consumers.

Consumers will not just be paying for that higher-priced gas generation, either. Because gas generation is such a large component of the overall electricity market, it now sets the marginal price for all generation in many markets across the U.S., particularly during peak demand periods. This means the rise in gas exports is contributing to higher electricity prices across the board—the costs of which will be passed through to consumers.

EIA is not alone in its concern about the impact of rising LNG exports. Moody’s, one of the major credit rating agencies, has repeatedly said that U.S. LNG exports will lead to higher domestic gas prices.

EIA’s concerns are also not hypothetical. The experience following the Russian invasion of Ukraine in 2022, which sparked a massive global increase in gas prices that hit consumers hard, still reverberates across the U.S. utility sector.

In Virginia, for example, Dominion went through a years-long process at the state corporation commission (SCC) to get approval to collect $1.28 billion in fuel costs amassed from July 2020 to June 2023.

As Dominion executives explained during the regulatory proceedings, the uncertainty following the invasion and the effort by European countries to replace Russian gas supplies “caused liquefied natural gas (LNG) prices in Europe and Asia to increase, leading to increased LNG exports by domestic suppliers.” U.S. exports climbed as high as 18% of total domestic gas production in March 2023, Dominion said, driven by producers seeking “considerably higher prices from overseas (primarily LNG) markets.”

Ultimately, the state approved a plan to securitize the uncollected fuel costs. This plan, adopted in February 2024, allowed Dominion to sell bonds to be repaid via a non-bypassable charge on ratepayers and collected over a 7.25-year period. Given the potential for future international price spikes, Virginia ratepayers may still be paying for the last LNG-driven cost runup when the next one occurs.

Dominion’s experience is not unique. Utilities and regulators in Ohio, Missouri, Alabama, Mississippi, Wyoming, Colorado, and Indiana have gone on record blaming LNG exports for higher energy bills.

Previous IEEFA research (hereand here) also has shown that rising LNG exports leads to greater gas price volatility in the U.S. We believe this rising volatility poses unwarranted risks to consumers and that utilities and regulators must more thoroughly analyze these issues when considering plans for new gas-fired power plants.

This is a particular concern given the significant increase in U.S. LNG exports projected by 2029. IEEFA data shows that current operating LNG export capacity is 15.43 bcf/d. This total rises to 16.49 bcf/d when the gas used in the liquefaction process is included. By 2029 an additional 12.97 bcf/d of export capacity could be online (14.01 bcf/d when the gas used during liquefaction is included). This would be an 84% increase in export capacity in just four years, further exposing domestic consumers to global price volatility.

These new projects will certainly expand U.S. exposure to international events and potential price spikes. And the new export demand, coupled with rising domestic gas consumption driven largely by rising electricity demand for new AI-related infrastructure, is likely to put upward pressure on U.S. gas prices. The upshot for U.S. consumers is that the risks of both greater price volatility and higher prices in general are rising.

As TradingNews summarized recently: “Gas exports have reshaped domestic pricing. U.S. production, once trapped by local constraints, is now fully exposed to global arbitrage. LNG terminals draw down Gulf Coast gas, pressuring the balance for Midwest and Northeast utilities.”

Utilities should be factoring these risks into their proposals for new gas-fired power plants since they could have a major impact on project economics, particularly in comparison to fuel-free renewable alternatives. If those comparisons are not made, regulators would be well-advised to require them, or they risk approving new generation projects that could impose significantly higher costs on ratepayers.