Key Findings

There’s a widening gap between the headline climate commitments made by India’s major steel companies and their actual progress in building the operational, technological, and financial infrastructure required to meet their decarbonisation ambitions.

While global peers have achieved reductions, emissions intensity for most Indian steel companies has worsened over the last three years despite ambitious targets, exposing a credibility gap between stated commitments and actual performance.

Progress is slowest in financial alignment. From a sample of seven Indian steel producers and three global peers, no company scored above 43%, indicating that capital allocation and alignment decisions across the sector have not kept up with stated climate strategies.

Indian companies are showing meaningful proactiveness despite the absence of effective carbon pricing or large-scale public financial support. Nonetheless, international experience confirms that the economics of green steel will not work without coordinated government intervention, making the Green Steel Mission and targeted fiscal instruments essential to converting corporate intent into execution.

With a looming spike in blast furnace capacity due for relining before 2030, and over two-thirds of planned additions employing conventional, emissions-intensive technology, every year of deferred action deepens carbon lock-in and narrows the window for cost-effective technology substitution.

India will shape the future of global steel emissions more than any other nation. It is the world’s second-largest steel producer, with capacity projected to reach 300 million tonnes (Mt) by 2030.1 Yet a fundamental question remains: are Indian steel companies genuinely prepared for a low-carbon transition, or do their climate commitments mask a widening gap between ambition and action?

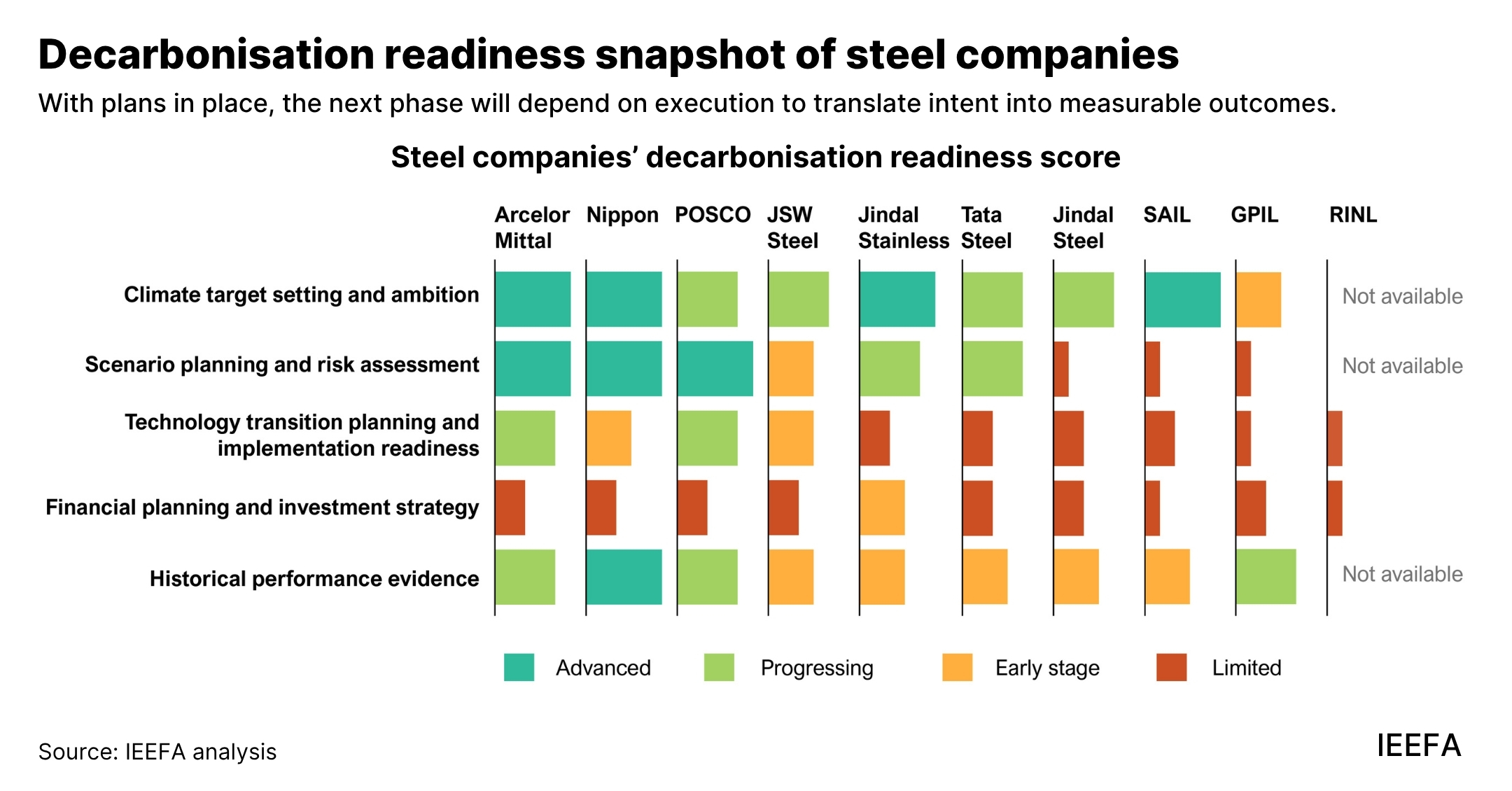

This report evaluates the decarbonisation readiness of seven major Indian steel producers against three global peers, using a structured framework that assesses the connection between stated targets to examine strategic planning, operational capabilities, and financial alignment. The Indian companies include JSW Steel, Tata Steel, Steel Authority of India Limited (SAIL), Jindal Steel, Rashtriya Ispat Nigam Limited (RINL), Jindal Stainless Limited, and Godawari Power and Ispat Limited (GPIL), while the global companies are ArcelorMittal, POSCO, and Nippon Steel. Drawing on established methodologies and frameworks, we have assessed companies across three layers:

• Strategic foundation: Climate target setting and ambition; and scenario planning and risk assessment.

• Implementation readiness: Technology transition planning and implementation readiness; and financial planning and investment strategy.

• Credibility validation: Historical performance and execution track records.

This assessment is not a call for expanded transition planning disclosure. For sectors like steel, disclosure frameworks — however refined — cannot substitute for government interventions, enabling policies, and market structures required to make low-carbon production commercially viable. Commercial financial institutions do not yet assign significant weight to climate disclosures that lack a material impact on near-term financial metrics, and a decade of proliferating disclosure initiatives has not translated into commensurate emissions reductions. The indicators examined here focus specifically on operational and financial readiness that is genuinely material to decarbonisation, not reporting comprehensiveness.

The findings indicate that climate ambition has outpaced implementation. Five of seven Indian companies assessed have adopted Paris Agreement-aligned net-zero targets for 2050, two decades ahead of India’s national commitment. On climate target setting and ambition, most score above 70%. This convergence reflects the growing recognition that decarbonisation has become strategically essential. But setting targets is not the same as preparing to meet them.

The gap becomes visible in scenario planning and risk assessment. While most Indian companies score well on target setting, few have shown any evidence that they possess the analytical infrastructure to stress-test these commitments against different future scenarios. Only Tata Steel, JSW Steel, Jindal Stainless, and Jindal Steel have undertaken any form of scenario analysis, and even their disclosure of results remains limited. Global peers demonstrate more systematic scenario integration, though this remains a developmental area across the industry.

Implementation readiness reveals further gaps, though not for India alone. Global peers score between 60% and 73% on technology transition planning and implementation readiness, supported by quantified abatement levers, asset-level blast furnace (BF) relining schedules, and contingency plans for technology delays. JSW Steel performs closest to global peers among Indian companies, with relatively stronger technology planning and comparably financial alignment, reflecting stronger planning frameworks than most Indian companies. However, the parameter captures the rigour of stated plans, not the status of their execution. On that front, a gap is emerging: Several high-profile European and North American projects have been cancelled or delayed due to prohibitive energy costs and inadequate hydrogen supply, indicating that even well-articulated transition plans face significant delivery risk.

The roughly USD24 billion (INR2.25 lakh crore)2 investments globally in steel decarbonisation to date have been overwhelmingly enabled by public capital, underscoring a basic reality: The economics of green steel do not yet work without substantial public support, regardless of geography.

Within India, JSW Steel and Tata Steel lead among domestic producers on technology planning, with pilot projects covering about 18% and 20% of their respective projected capacity. But gaps persist across the sector in quantification of targets for each transition lever across planning horizons. According to the Transition Plan Taskforce (TPT), transition levers are broadly defined as the range of approaches available to an organisation to facilitate its climate transition, including capital investment, skills and training, and industry or government engagement.3 Gaps also remain in relining schedule disclosure and contingency planning. Steel Authority of India Limited (SAIL), Godawari Power and Ispat Limited (GPIL), and Rashtriya Ispat Nigam Limited (RINL) show limited progress in translating climate commitments into operational planning.

Financial alignment is the weakest dimension across the entire sample, including global peers. No company scores above 43% for financial allocation, indicating that capital allocation decisions have not yet caught up with stated climate strategies. This reflects the underlying commercial reality: With green steel carrying a cost premium of approximately USD210 per tonne (INR19,740 per tonne) over conventional production, and with technology pathways still maturing, capital competes against conventional expansion projects that offer more certain near-term returns. This is a sector-wide challenge globally, not an India-specific one.

What deserves recognition is that Indian steel companies are showing meaningful proactiveness on decarbonisation even in the absence of effective carbon pricing signals or large-scale public financial support. Steel-specific intensity targets under India’s Carbon Credit Trading Scheme (CCTS) are yet to be defined, the Green Steel Mission remains in formulation, and Indian producers receive a fraction of the fiscal incentives available to their global counterparts. Against that backdrop, the fact that most private Indian producers have set Paris-aligned targets, begun identifying technology pathways and, in some cases, initiated pilot projects reflect genuine strategic intent. The challenge is converting that intent into execution at the pace and scale the transition demands.

Bridging this gap will require coordinated government action. International experience demonstrates that carbon pricing alone cannot drive the steel transition. Even in Europe’s relatively mature carbon market, green steel projects require public support far beyond what the carbon price signal provides. For India, where the policy architecture is still being assembled, targeted public capital deployment through instruments such as credit guarantee facilities, competitive contracts for difference, and green public procurement mandates will be needed to shift the risk-reward calculus for producers and unlock private investment at scale.

The indicators developed in this assessment provide a basis for distinguishing those companies whose transition strategies are operationally grounded from those whose commitments remain largely aspirational. What separates leaders from laggards across both Indian and global producers is not the ambition of their targets but the depth of operational and financial planning behind those targets. On that measure, the sector as a whole — in India and globally — has considerable ground to cover.

Related Content