IEEFA update: Under PREPA’s new debt deal, electricity prices will rise 13% by next summer in Puerto Rico

A deal has been reached to settle the more than $8 billion in legacy debt of the Puerto Rico Electric Power Authority (PREPA). Last Friday, the Financial Oversight and Management Board (FOMB) for Puerto Rico published an agreement between the government of Puerto Rico, the FOMB, a majority of PREPA bondholders, and Assured Guaranty, a major insurer of PREPA bonds.

A deal has been reached to settle the more than $8 billion in legacy debt of the Puerto Rico Electric Power Authority (PREPA). Last Friday, the Financial Oversight and Management Board (FOMB) for Puerto Rico published an agreement between the government of Puerto Rico, the FOMB, a majority of PREPA bondholders, and Assured Guaranty, a major insurer of PREPA bonds.

The deal calls for an annual per-kWh charge that customers of PREPA (or any successor company) will be obligated to pay through 2067. IEEFA estimates that over the next 48 years, Puerto Ricans will pay more than $23 billion, plus an initial $100-$200 million settlement charge to cover administrative expenses on the deal.

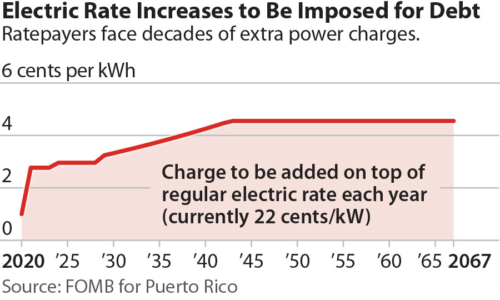

The first rate increase, which comes on top of the current 22 cents/kWh, will take effect this summer with a 1 cent/kWh increase to cover the settlement charge. Starting in July 2020, the debt charge will be 2.8 cents/kWh. In other words, between now and next summer, rates will go up by 13%. Over time, rates for the debt will rise to 4.55 cents/kWh in Fiscal Year 2043 and remain at that level through the lifetime of the debt payoff.

For the average residential household in Puerto Rico, which uses about 400 kWh/month, the deal will result in a charge of more than $130 per year in FY 2021, increasing to nearly $220 per household per year in FY 2043.

For the average residential household in Puerto Rico, which uses about 400 kWh/month, the deal will result in a charge of more than $130 per year in FY 2021, increasing to nearly $220 per household per year in FY 2043.

Under the terms of the deal, holders of PREPA’s legacy debt will exchange their outstanding bonds for new bonds that will be paid off over the coming decades. By granting these new bonds a superior lien position, the deal ensures that the first priority use of every rate dollar that comes into PREPA goes towards paying off the legacy debt.

Even customers who install their own power generation will be required to pay the debt charge

The deal also directly – and intentionally – goes against Puerto Rico’s new energy policy of moving towards a more distributed and decentralized electricity system. In order to ensure that residents and businesses that elect to generate their own electricity are not exempted from paying back the legacy debt, any customer who installs their own generation after September 30, 2020 will be required to pay the debt charge on all the electricity they purchase from the grid, as well as for the electricity produced by their own solar panels. Customers who install grid-connected systems before September 30, 2020 will be exempt from paying the debt charge on their self-generated electricity for twenty years, but after that time, they will be paying over 4 cents/kWh on the electricity generated by their own equipment.

The deal must be approved by the bankruptcy court and also requires approval by the Puerto Rican legislature.

IT IS IMPORTANT TO RECALL THAT WHEN PREPA WENT BANKRUPT, BEFORE THE HURRICANES, ITS PHYSICAL INFRASTRUCTURE WAS IN A STATE OF EXTREME DISREPAIR. In 2016, consultants to the Puerto Rico Energy Bureau noted that “many of PREPA’s existing units are in such a poor state of repair that PREPA must consider itself lucky if they remain operational for more than several months at a time,” and that “PREPA’s transmission and distribution systems are falling apart quite literally.”

In the decade that preceded this grim assessment, PREPA made many missteps: taking on debt to cover operating expenses, failing to diversify away from imported oil, and heavily subsidizing the electricity provided to municipalities and other entities, not to mention perpetuating a multi-billion-dollar oil fraud scheme. PREPA’s indebtedness almost doubled from 2005 to 2014, as the island’s declining economy was increasingly unable to support this mismanagement.

THROUGHOUT THIS PERIOD, AND IGNORING ALL WARNING SIGNS, PREPA’S CONSULTING ENGINEER (URS CORPORATION) CONTINUED TO CERTIFY THAT THE SYSTEM WAS “IN GOOD REPAIR AND SOUND OPERATING CONDITION,” rating agencies continued to give PREPA investment-grade credit ratings, and underwriters and legal advisors continued to collect fees on various loans and debt deals. Although the actions of some of these entities have been questioned by the Puerto Rico Commission for the Comprehensive Audit of the Public Credit and by the FOMB’s independent investigator Kobre & Kim, the new debt deal makes no effort to hold any of the responsible parties accountable. Indeed, some of those same parties will continue to benefit from fees linked with the new debt issuance.

PREPA’s nearly $9 billion in legacy debt produced very little in the way of long-term assets to benefit the people of Puerto Rico. Yet, Puerto Rican households are now being required to pay $130-$220/year to pay for a system that did not work.

Cathy Kunkel ([email protected]) is an IEEFA energy analyst.

Tom Sanzillo ([email protected]) is IEEFA’s director of finance.

Related Items

Related Content