Key Findings

India’s electric vehicle (EV) sector attracted ~INR2.23 lakh crore (USD25.6 billion) in investment from 2020 to 2025, or 18% of the estimated total investment needed by 2030.

In 2024 and 2025, EV investment announcements shifted decisively from three-wheelers to four-wheelers, driven by surging demand for premium electric cars.

Public charging infrastructure investment from 2020 to 2025 amounts to ~9.6% of the INR20,600 crore (USD2.36 billion) estimated to be required by 2030.

Commercial EV borrowers face interest rates of 15–33%, which offset the total cost of ownership advantages of EVs. An integrated financing platform—combining credit guarantees, residual value protection, battery-as-a-service, and co-lending—could bring rates closer to 8–12%.

Executive summary

India has a vision to increase the share of EV sales to 30% in private cars, 70% in commercial vehicles, 40% in buses, and 80% in two- and three-wheelers by 2030. Achieving these goals requires substantial investment in electric vehicle (EV) manufacturing, charging infrastructure, and supportive ecosystems. This report provides a consolidated view of realised investments between 2020–2025, identifies the investment gap, and outlines pathways to mobilise capital for the next phase of India’s electric transport transition.

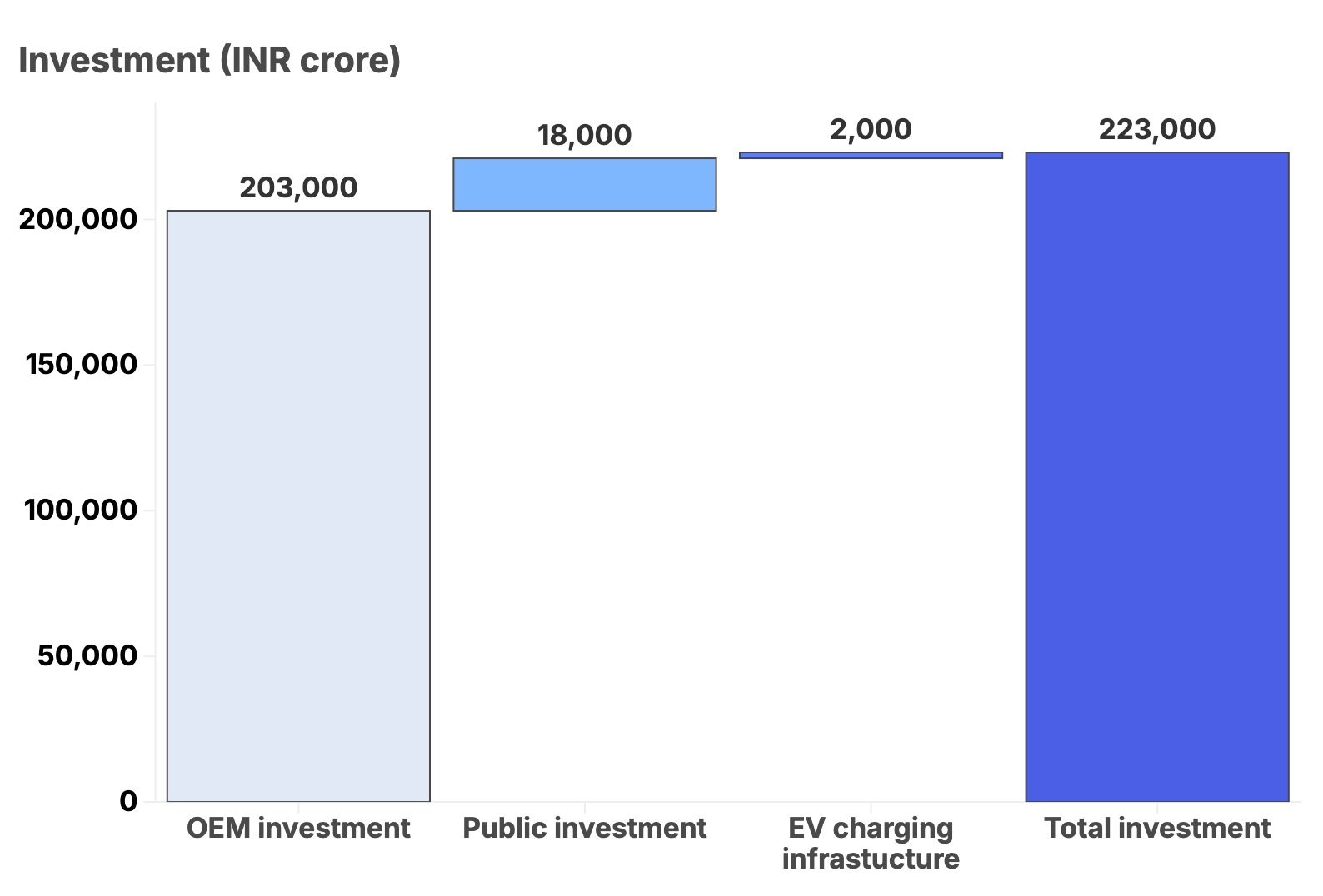

IEEFA estimates a capital deployment of ~INR2,23,119 crore (USD25.6 billion) across three measurable nodes of India's electric transport ecosystem from 2020 to 2025. These include investments by vehicle manufacturers (original equipment manufacturers – OEMs), public subsidies and incentives and investments in public charging infrastructure. Investments in OEM manufacturing capacity accounted for the bulk of the investments during this period (Figure 1).

Figure 1: India’s electric transport investments, 2020–2025 (INR crore)*

Sources: IEEFA estimates, company financials, and budget documents.

*Notes: Figures have been rounded off. Public investments include only direct fiscal support extended through government schemes. Our estimates also exclude investments made by component manufacturers, non-fiscal incentives and capex subsidies given by states for EV manufacturing.

However, this figure represents only about 18% of the roughly INR12,50,000 crore (USD143.41 billion) required to meet India’s transport electrification targets by 2030, based on publicly available projections. Mobilising the remaining INR10,26,881 crore (USD117.82 billion) by 2030 presents a significant challenge.

From 2020–2025, electric three-wheelers (E3Ws) had the largest share (~78%) of investments among vehicle segments, due to the segment’s maturity and the achievement of commercial-scale operations. Electric two-wheelers (E2Ws, mostly scooters), electric four-wheelers (E4Ws, mostly cars) and electric buses (e-buses) accounted for the remainder. However, investment announcements in 2024 and 2025 revealed a marked shift in potential investments towards E4Ws, driven by rising demand for premium electric cars.

Among financing sources, internal accruals accounted for the largest share of realised EV manufacturing investment (INR1,59,701 crore/USD18.32 billion), followed by debt (INR36,738 crore/USD4.22 billion) and equity (INR6,455 crore/USD740 million). This aggregate pattern masks segment-level differences. Internal accruals dominate fragmented and incumbent-led segments, while debt and equity play a larger role in segments with greater scale, demand visibility, and firm maturity.

Government subsidies under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme and other Union- and state-level policies catalysed adoption by disbursing INR18,251 crore (USD2.09 billion) from FY2020–24. While public investments grew during the period, disbursements are below budgeted outlays due to several implementation bottlenecks.

Public EV charging grew rapidly (from 5,151 chargers in 2020 to 39,485 in 2025), but remains far below global benchmarks. India’s charger-to-EV ratio significantly lags China, the EU, and the US. Investment in charging infrastructure from 2020–2025 accounted for only 9.6% of the INR20,600 crore (USD2.36 billion) required by 2030. Investment in EV charging faces challenges due to limited investor interest, as public EV charging remains an unproven business model, with many charging stations reporting low usage and high initial costs.

With an estimated 82% of required investments pending, India must attract diverse financing sources to mobilise capital at scale to meet the 2030 electric transport goals. Bridging the INR10,26,881 crore (USD117.82 billion) EV manufacturing and charging infrastructure investment gap in five years requires moving beyond traditional subsidy-led approaches to systemic derisking mechanisms that unlock private capital at scale.

IEEFA proposes an integrated EV financing platform bundling partial credit guarantees, residual value protection, battery-as-a-service models, and co-lending structures. Development finance institutions with existing guarantee infrastructure and bank relationships would anchor such a platform—Small Industries Development Bank of India (SIDBI) is well-positioned for the micro, small, and medium enterprises (MSME) segment (commercial two- and three-wheelers, small fleet operators), while India Infrastructure Finance Company Limited (IIFCL) could serve larger commercial and institutional buyers. Partnering with OEMs, banks, and non-banking financing companies (NBFCs), and drawing on carbon revenue streams, such a platform could unlock low-cost bank financing through comprehensive risk coverage.

Related Content