Solar, battery storage to continue rapid growth as coal and gas share of power keeps shrinking

The blistering pace of the buildout of solar and battery storage appears set to continue for at least the next two years, allowing renewables to keep winning market share from coal and gas in U.S. power markets.

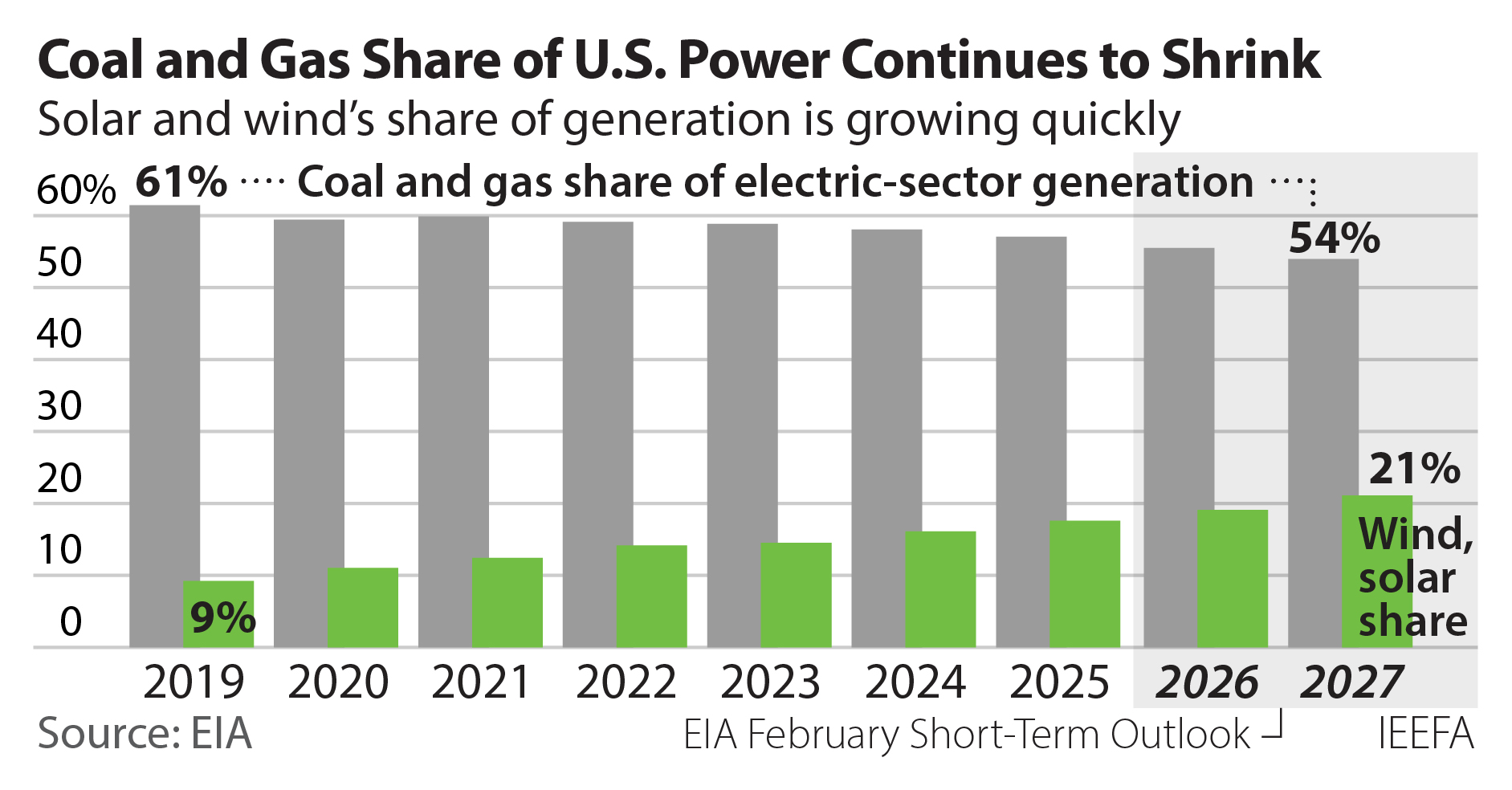

The Energy Information Administration’s (EIA) latest short-term outlook projects that U.S. electricity generation will increase by 170 million megawatt-hours (MWh) through the end of 2027, or 4%. Renewables, largely solar, are expected to account for all that increase and more. Overall, EIA expects generation from utility-scale wind, solar, and hydropower to rise by 201 million MWh through 2027, pushing their market share up to 27%.

The growth in renewables is not just a two-year blip. Combining annual totals from 2022-25 with the projections through 2027 tells the same story. EIA’s data shows that over the five-year period, the increase in generation from these three renewable resources will total 367 million MWh, also covering all the expected increase in total demand. The result will be a continuation of the trend highlighted in the following graphic: Fossil fuels’ share of U.S. generation is declining steadily even as the demand for power increases.

Solar is by far the fastest growing renewable resource, with total output from utility-scale facilities projected to top 418 million MWh by the end of 2027, up 275 million MWh in just five years and pushing its market share to just under 10%. Of particular interest is that solar’s growth, long focused in Texas and California, is growing rapidly across the country.

Nowhere is this more evident than in the Midcontinent Independent System Operator (MISO) system that stretches from Louisiana in the south to Minnesota and Michigan in the north (see territory map below). Solar has been a relative afterthought across the system, until recently.

Solar generation barely provided 1% of total MISO demand in 2023 and only topped 2% of the system’s daily demand six times that year. Fast forward to 2025 and solar’s share of total MISO generation has jumped, averaging 4.5%. And according to year-end MISO statistics, solar generated 6% or more of the system’s demand during five months of the year—a sharp increase from its 2023 output.

Solar’s growing market share is particularly noteworthy given that overall demand in MISO has climbed significantly in the past two years, rising by almost 7%. In other words, solar is outgrowing a growing market. In fact, solar accounted for 55% of the total increase in MISO demand from 2023-25, with wind providing another 17%. This rapid renewable growth pushed the share of MISO’s coal- and gas-fired generation down 3% in just two years.

The growth in MISO solar generation resembles the early development in the Electric Reliability Council of Texas (ERCOT), now the largest solar market in the U.S. ERCOT did not begin reporting solar data until 2016, when it supplied 0.2% of the system’s electric needs. Solar generation grew from there, topping 1% of demand in 2019, rising to more than 5% in 2022, and jumping to just under 14% in 2025, the third-largest power resource after gas and wind.

MISO may not duplicate ERCOT’s subsequent growth, but EIA data shows that more solar is coming. Overall, companies are planning to add 15,470 megawatts (MW) of solar in MISO through 2028, with half of that already under construction.

Solar is also growing outside the nation’s organized markets.

In Florida, for example, NextEra Energy subsidiary Florida Power and Light has installed thousands of megawatts of solar capacity in the past several years, with plans for much more through the early 2030s. In 2025, solar met 11% of FPL’s demand, more than double its 2021 share of 4.4%. In its latest long-term resource plan, FPL says its installed solar capacity will increase threefold by 2034, to 24,471MW from 7,932MW in 2025, tripling its share of the utility’s annual demand to almost 35%.

Nevada is another solar success story. It currently generates 34.4% of its electricity from the fuel-free resource—29.5% from utility-scale projects (the highest rate in the U.S. in 2025) and another 4.9% from rooftop or other small-scale installations. That number should continue to rise, with EIA data showing that an additional 2,893MW of utility-scale solar are currently under development and scheduled to come online by the end of 2029.

Nevada also points to two other national trends that will continue to push the transition away from fossil fuel resources in the electric power sector: the ongoing growth of small-scale solar and the rapid, transformative adoption of dispatchable battery storage.

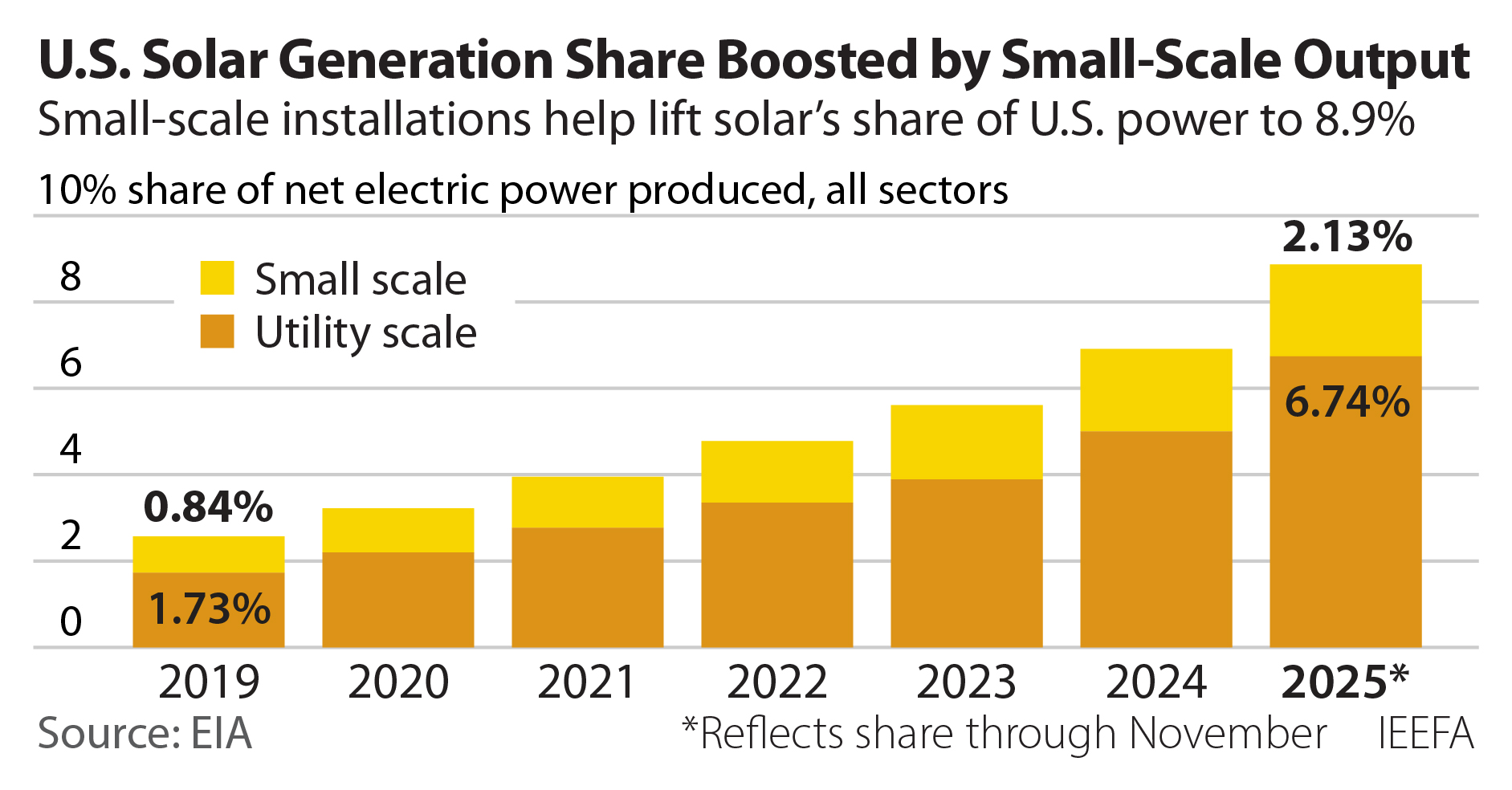

Small-scale solar has grown significantly in the past decade. Output from these distributed resources has doubled since 2020, and now accounts for more than 2% of total U.S. generation. But in many states, the growth has been even faster. In Nevada, for example, rooftop solar accounted for less than 2% of statewide generation in 2020. Through November, four states produced more than 10% of their power from small-scale solar, with Massachusetts topping the list at 16.0%, followed by Hawaii (15.1%), California (14.5%), and Vermont (10.3%).

The beauty of small-scale solar is that it works everywhere, particularly in areas where larger utility-scale facilities are harder to site. In the New England market run by ISO-NE, rooftop solar frequently provides more than 20% of total demand; when the region set its most recent record, these distributed facilities accounted for 46% of demand.

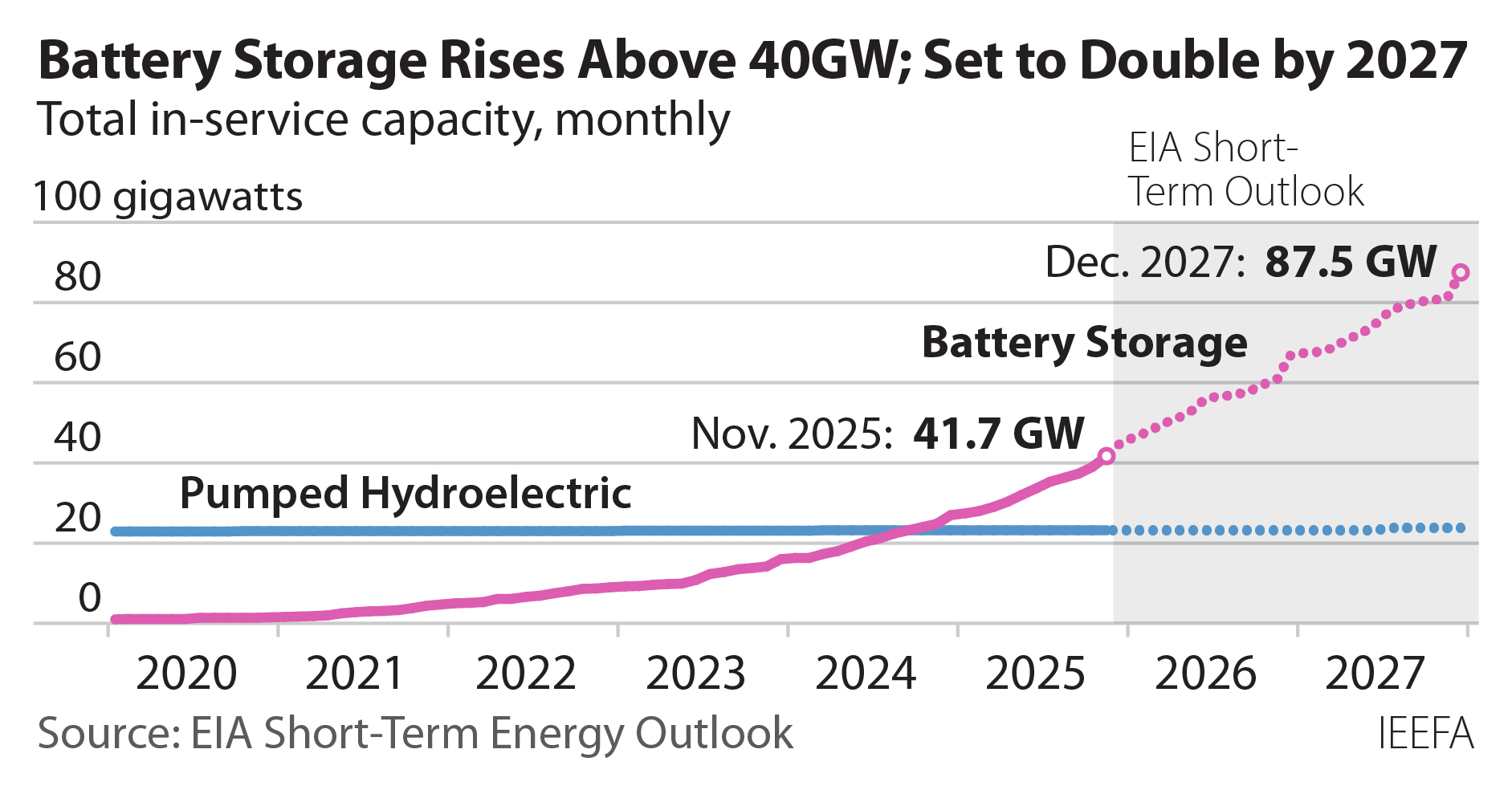

The most transformational technology in the power markets right now is dispatchable battery storage. Its rapid growth and reliable performance has turned solar from a reliable daytime energy producer to a truly dispatchable resource, a transition that is already evident in Texas and California. Batteries can be charged from any resource, but in practice they are generally charged during the day when solar generation peaks and wholesale power prices are low. Then, batteries are discharged into the grid during two periods of higher demand and prices: early evening around sunset and in the morning just before sunrise. In this fashion, solar is being time-shifted and reliably dispatched when needed, reducing the need for fossil fuel generation and helping to keep prices down.

Installed battery storage capacity in California and Texas accounts for more than two-thirds of the current operating total nationally, but this is projected to fall steadily as more batteries are installed across the country. EIA data through 2025 shows that there are only five states with more than 1,000MW of installed battery storage capacity, with Arizona, Nevada, and New Mexico joining California and Texas. But by 2030, EIA data shows that 12 states will have more than 1,000MW of installed battery storage capacity, and four others will top 500MW.

This forecast also likely understates the amount of battery storage capacity that will be installed by then. The technology is relatively easy to site since it can often be co-located at existing generation sites or substations. The components also are readily available and stable or declining in cost, unlike hard-to-purchase and increasingly expensive gas turbines.

The current political headwinds facing the energy transition are real. But the market clearly recognizes the economic competitiveness, reliability, and speed to market of renewables and dispatchable battery storage. That’s why the energy transition is continuing; the only question is how fast it occurs.

Related Content