Shell’s 4Q25 results confirm chemicals division is structural drag

Key Findings

Shell’s chemicals division continues to be a drag on the company.

The company’s $14 billion Monaca facility accounts for many of the losses.

Disappointing revenues have been caused by an oversupplied market, not a soft macro environment.

Rather than “fix and reposition” the Monaca petrochemical facility, Shell should “rationalize and exit.”

Shell’s fourth-quarter earnings reinforce what we highlighted last year: The company’s chemicals division—and particularly the Monaca petrochemical complex—continues to destroy value.

The results confirm a trajectory we highlighted in our October 2025 report: The chemicals business has transitioned from a cyclical underperformer to a structural drag on the company’s valuation. While the upstream and integrated gas segments continue to benefit from high-return projects and strategic exits, the chemicals segment remains mired in losses.

The $14 billion Monaca facility in Pennsylvania—which cost double its original estimate—is the centerpiece of this failure. Shell must move beyond “fixing and repositioning” and pivot toward “rationalizing and exiting” this segment to protect shareholder returns.

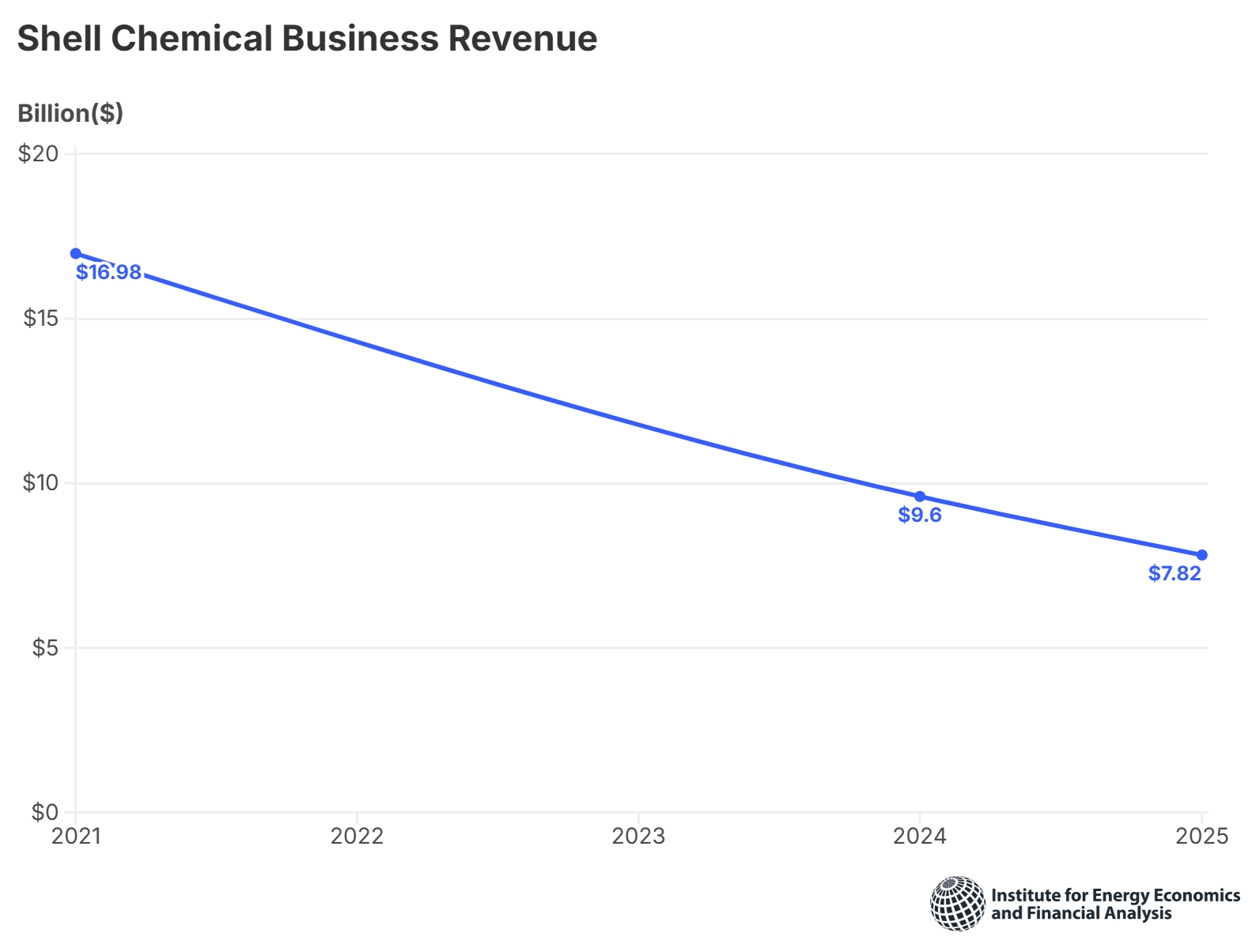

This is not a cyclical blip. It confirms a structural problem. The company’s chemical business revenue declined 43%, from $16.98 billion in 2021 to $9.60 billion in 2024. The deterioration has continued into 2025, with revenue falling to $7.82 billion—a cumulative decline of 54% from 2021 levels.

EBITDA in 2025 is now down 97% from its 2021 peak and negative free cash flow has been persistent. The 4Q25 earnings report validates our prior conclusion: Monaca and the broader chemicals division are misaligned with Shell’s capital allocation priorities and hurdle rates.

The strategic question is no longer whether chemicals will recover. It is whether Shell should continue owning them.

Time to shift from “fix and reposition” to “rationalize and exit”

Meanwhile, global petrochemical capacity continues to expand faster than demand growth, particularly in China and the Middle East. Shell’s U.S. ethane-based model no longer guarantees margin resilience in a market characterized by:

- Overcapacity

- Slower GDP-linked plastics demand

- Increasing policy pressure on single-use plastics

- ESG capital reallocation away from fossil-intensive assets

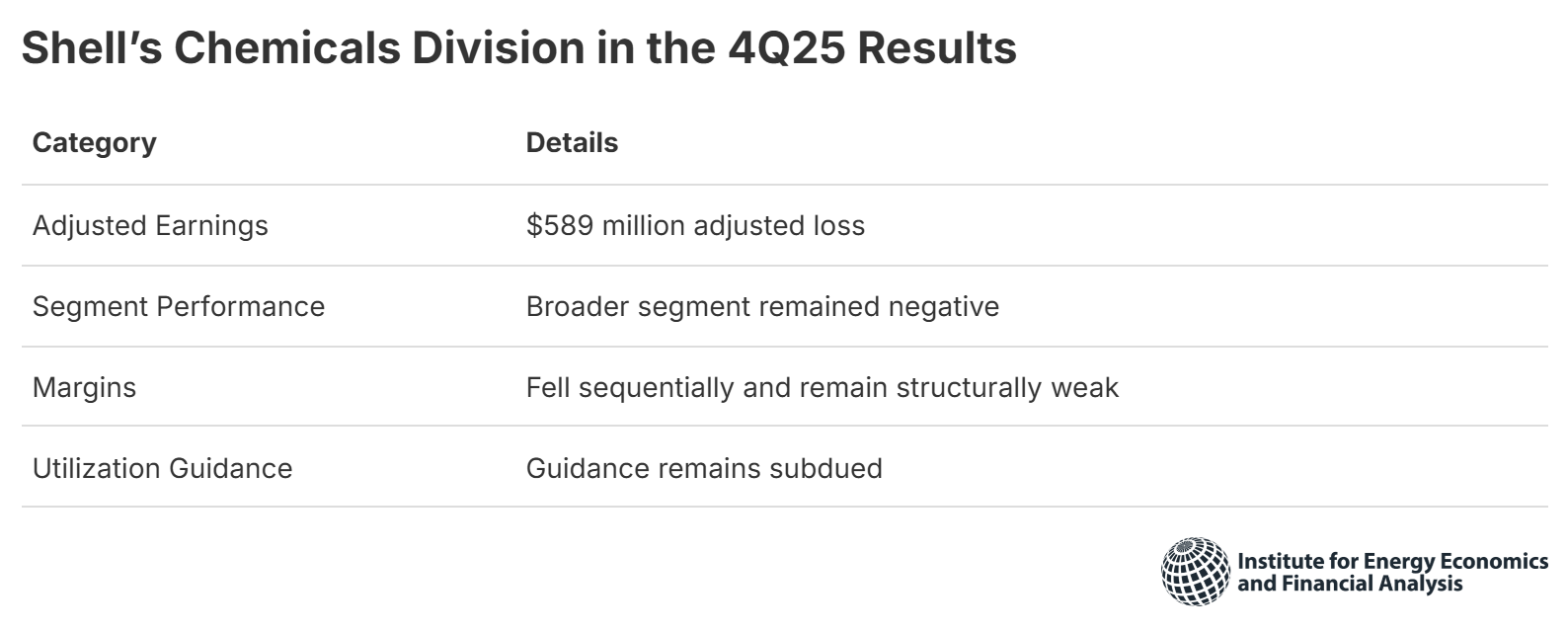

The 4Q25 loss is not merely a reflection of a soft macro environment but a symptom of costly assets entering a structurally oversupplied market. Management explicitly cited a planned downturn and continued operational headwinds at the Monaca facility as a weight on performance. The $14 billion capital investment—double its original estimate—is now actively eroding group-level returns.

Even so, Shell management’s current narrative focuses on "fixing and repositioning" the chemicals business to achieve an annual growth and normalized free cash flow per share of over 10% through 2030. By “fixing and repositioning,” management is referring to restructuring underperforming assets, reducing costs and optimizing capacity utilization of those assets. But the overcapacity (driven by China) and compressed margins for polyethylene/ethylene are not temporary. They are structural.

Meanwhile, capital remains trapped in the low-margin Pennsylvania petrochemical hub. Every dollar deployed into a negative return petrochemical asset is a dollar not deployed into lower-carbon transition investments, debt reduction, or shareholder return enhancement.

Our October 2024 briefing note warned the $575 million annual EBITDA target for Monaca was highly unlikely to be met. The 4Q25 results reinforce that the plant is currently a net consumer of cash rather than a generator. Despite internal efforts to "fix and reposition" the business, significant work would still be required to move the chemicals business to a positive free cash flow story.

Currently, the segment remains a laggard, trapped in a cycle of high-maintenance capex and negligible (or negative) margins.

Moving beyond the downcycle

It is time for Shell to acknowledge the Monaca investment was a strategic error based on outdated market assumptions. IEEFA warned as early as 2020 that the project could come online into a challenging market environment. Shell’s current strategy of "leaving no stone unturned" to reach cash neutrality is insufficient for an asset of Monaca's scale. The "fixing" narrative implies the issues are purely operational, but our 2025 report, Shell’s petrochemical problem in Pennsylvania, has proved the issues are structural and economic.

Shell’s management must shift from a "fix and reposition" mindset to a "rationalize and exit" strategy. By “rationalize,” we mean undertaking a serious portfolio review that prioritizes capital discipline—recognizing impairments where necessary, shutting down structurally uncompetitive capacity, redeploying capital to higher-return opportunities, and eliminating assets that consistently fail to earn their cost of capital. In an operational environment where Shell is being punished by investors for its reserve life (short oil and gas life) and capital discipline, clinging to a value-destructive petrochemical asset is no longer defensible. The most economical path forward is to stop throwing good money after bad and consider a total exit from the Monaca site.

The successful Nigeria (SPDC) and Canadian Oil Sands exits present a potential blueprint for the corporation to extricate itself from its unsuccessful Monaca venture. The current situation for the chemicals division makes it likely that Shell management will accelerate rationalization efforts, and the company may find it necessary to consider impairment and shutdown options to halt ongoing operating losses.

Shell’s 4Q25 results reinforce that the financial status of the company’s chemicals division is a structural capital misallocation that calls for correction. Patience is a virtue only when returns justify it.

Related Research