South Australia is squandering a world-leading green iron and steel opportunity

Key Findings

By locking in the use of gas, South Australia risks squandering its opportunity to lead the global transition to green iron and steel.

The state government’s agreement with Santos to supply gas for the Whyalla steel plant suggests it has bought into gas industry claims that the only way to secure Australia’s steel sector is by replacing coal with gas.

The government’s recent shelving of green hydrogen projects reflects a misinterpretation of the current state of the transition to low-emissions iron and steel, with early use of green hydrogen becoming the global benchmark.

As green steel and green hydrogen projects gain momentum worldwide, South Australia’s continued commitment to gas may offer initial relief for Whyalla, but it won’t provide the long-term basis for a thriving domestic steel industry.

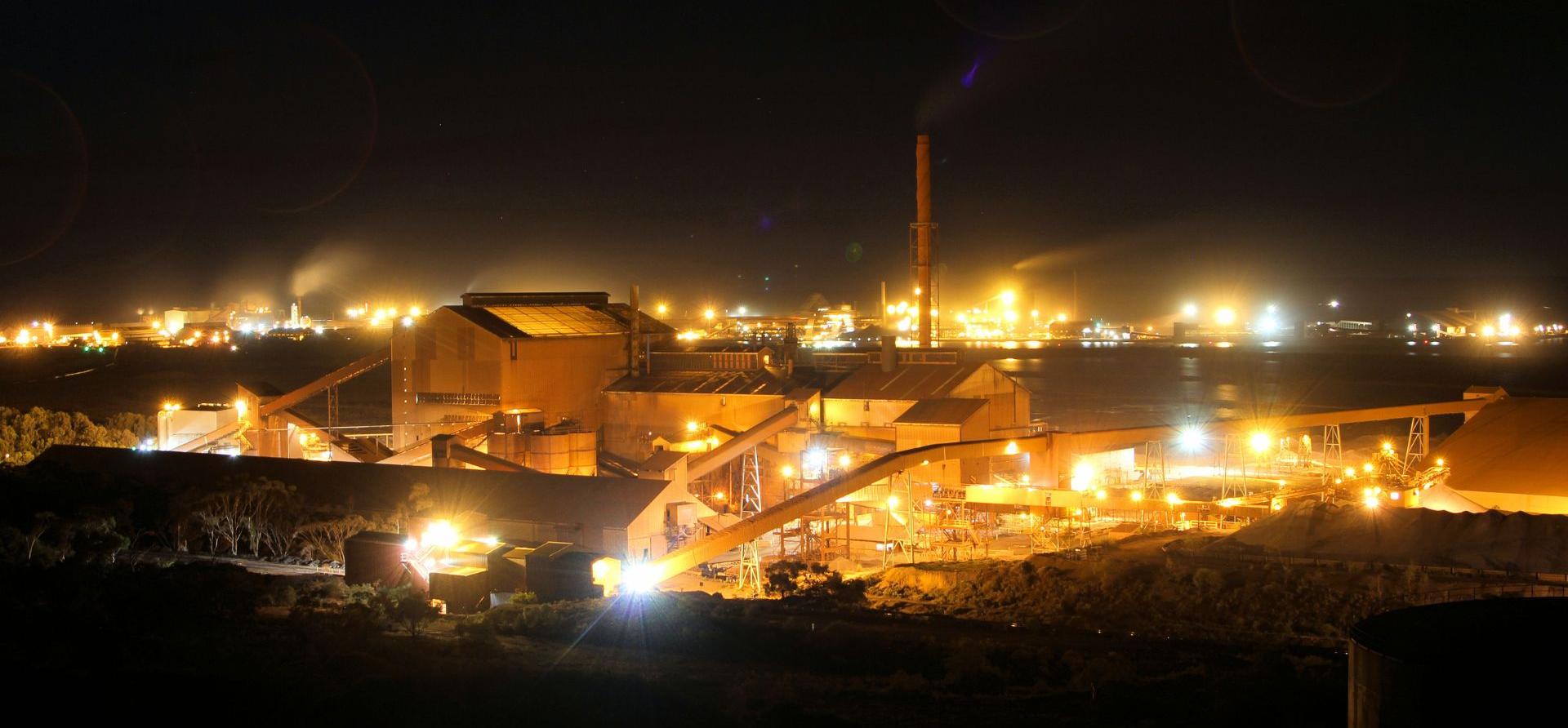

When the South Australian government published its Green Iron and Steel Strategy less than two years ago, the state was in a world-leading position to benefit from the steel technology transition away from fossil fuels.

Unfortunately, since then the state government has given up that position and is falling behind other global locations.

Now it has signed an agreement with Santos for the supply of 200 petajoules (PJ) of gas supply over 10 years. The deal is more evidence of the government buying into the gas industry’s questionable claim that switching from one fossil fuel to another is the only way to secure the Australian steel sector and capitalise on the opportunity to process the state’s high-grade iron ore for export.

Most of the 200PJ of gas is earmarked for the Whyalla steel plant’s transition from coal-based blast furnace to direct reduced iron (DRI) technology that can run on gas or green hydrogen (or both). The agreement is not much of a surprise – in February 2024 Santos signed a memorandum of understanding (MoU) with Whyalla’s previous owner GFG Alliance for gas supply.

This represents the Australian gas industry’s latest bid in its efforts to secure new demand from the iron and steel sector whilst attempting to convince us that a switch to gas will cut emissions. Any future demand for gas from new DRI plants will likely be used as an excuse to open up new gas reserves.

The supply agreement also may be partly an attempt by Santos to get ahead of federal government plans to impose more stringent reservation requirements for the east coast gas market.

Although steelmaking via gas-based DRI produces less carbon dioxide than coal-based blast furnaces, it is still very emissions-intensive, releasing 1.66 tonnes of greenhouse gases per tonne of crude steel produced according to the World Steel Association. You can’t make green iron and steel with gas.

The 2024 Santos/GFG MoU stated that the planned Whyalla DRI plant would “use a mix of natural gas and green hydrogen as the reducing agent, with the aim of fully transitioning to green hydrogen as it becomes available at scale”.

But since then, the South Australian government has lost interest in that transition. The state’s planned green hydrogen project – earmarked to supply Whyalla – has been shelved and its Office of Hydrogen Power has been disbanded. South Australian Treasurer Tom Koutsantonis has stated that the government will not be reviving its green hydrogen plans and that “gas is going to be king” for the Whyalla steelworks.

This policy shift reflects a misreading of the state of the steel technology transition globally. Although there has been a slowdown in green hydrogen developments around the world, its role in truly green iron and steel is firming up. Early green hydrogen use in DRI plants is now becoming the benchmark for low-emissions iron and steel.

Meranti Green Steel is set to make a final investment decision on a new DRI plant in Oman by the middle of 2026. From day one it will use a blend of 15% green hydrogen and 85% gas in its reduction mix, before gradually increasing the proportion of green hydrogen. This has not stopped Meranti securing 100% offtake coverage for its future iron production of 2.5 million tonnes per annum.

In addition to being a good place to produce green hydrogen, Oman has much cheaper gas than the Australian east coast gas market. Gas is not an area of comparative advantage for South Australia. Oman is one of several territories that have clearly overtaken South Australia in the last two years and are leaving it behind.

According to Hydrogen Insight, 59 new hydrogen projects began construction in 2025. Almost all of these are green hydrogen projects with nearly half of them in China. China Baowu – the world’s largest steelmaker – already has a commercial-scale DRI plant in operation. It is now developing a green hydrogen plant powered by offshore wind to supply it.

In Europe, the EU looks set to make green steel a key part of its efforts to support industry in a move that will support the use of green hydrogen in the steel sector. Measures will likely include the creation of new demand for green steel through public procurement and from the auto sector.

Stegra is pressing ahead with construction of its DRI plant in Sweden, which will run on 100% green hydrogen from the start. Stegra has been able to secure offtake of truly green steel at a 20%-30% premium from sectors including automakers. Such premiums would not be available to iron and steel produced using gas.

The German government has just increased its financial support for Saltzgitter’s new DRI plant to EUR1.3 billion (AUD2.2 billion). The steelmaker will run the plant on a mix of gas and green hydrogen that it will produce itself. And France’s GravitHy has also recently recommitted to green hydrogen for its own DRI plant, stating: “Our strategy is to start with hydrogen from day one.”

The South Australian government’s priority is clearly the future of domestic steelmaking at Whyalla and the jobs it supports. In common with other Australian governments, it is buying gas industry spin and has decided the uptake of green hydrogen in the iron and steel sector will be delayed.

But around the world there are examples that clearly challenge that narrative. From initially being one of the leaders, South Australia has fallen behind in the transition towards truly green iron and steel. Gas may support Whyalla in the short-to-medium term, but it won’t provide the long-term foundation for a thriving steel industry or for the processing of the state’s high-grade iron ore for export amid growing global competition.

Related Content