Viability of standalone battery energy storage tariffs discovered in 2025

Download Full Report

View Press Release

Key Findings

India’s clean energy transition is increasingly becoming dependent on large-scale storage deployment, with procurement shifting toward standalone energy storage system (ESS) tenders that contract storage capacity without being tied to a specific renewable generation asset. These standalone tenders made up more than 71% of the total capacity tendered in India in 2025, with standalone battery energy storage system (BESS) projects accounting for 60% of this capacity.

A total of 10.4GW of standalone BESS capacity was allocated in 2025, with the 2-hour, 2-cycle configuration accounting for the bulk of this capacity.

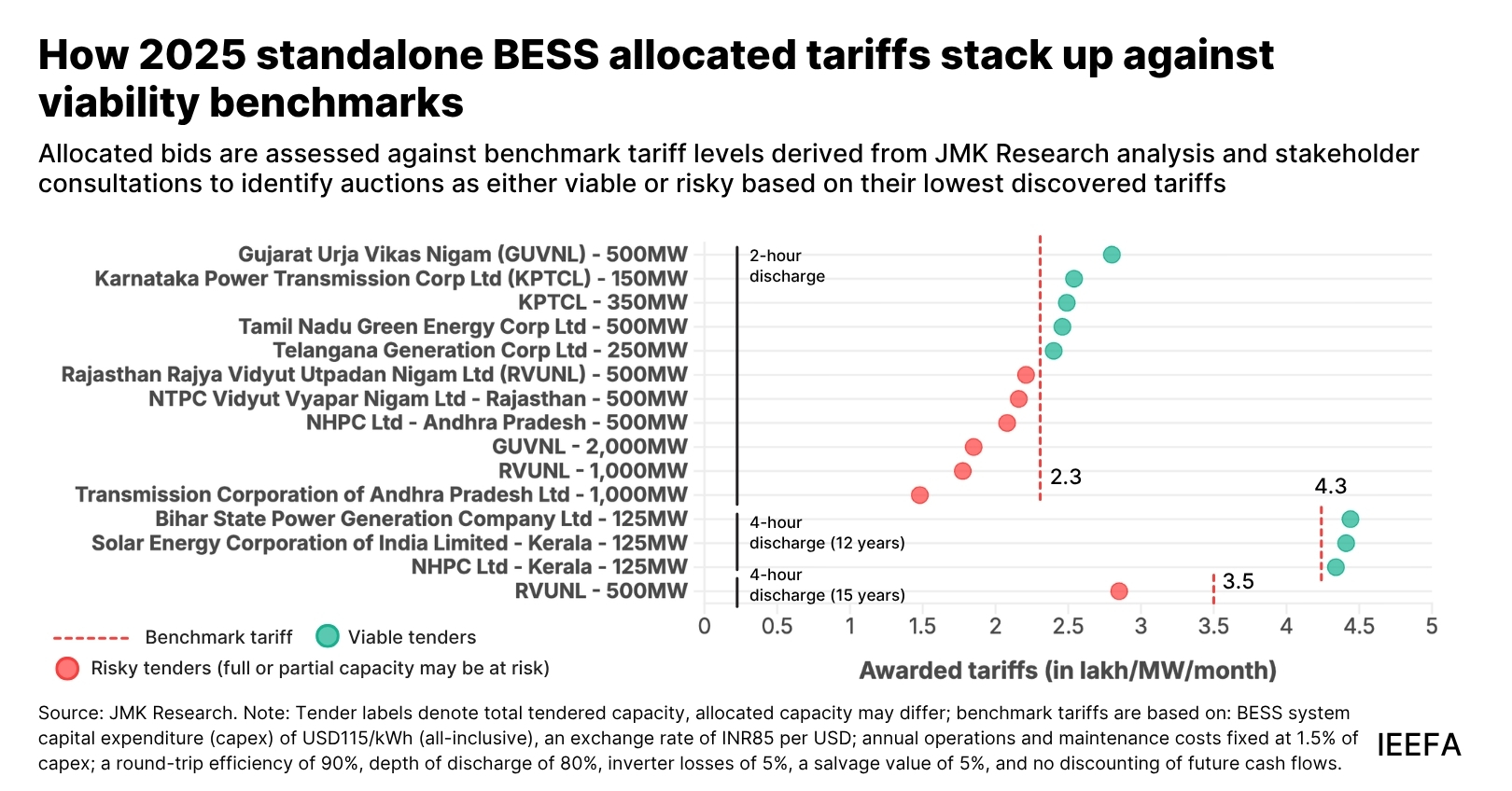

Tariff viability of the 2025 standalone BESS bids, however, remains a concern. Standalone BESS tariffs fell, with the lowest tariffs discovered reaching INR1.48 lakh/megawatt/month (USD1,576/MW/month) for the 2-hour system. Nearly 75% of allocated 2-hour BESS capacity falls into the at-risk viability category, indicating a major gap between discovered tariffs and actual project costs.

Execution risks can constrain BESS project realisation. Financing conditions remain stringent, while declining tariffs, rising battery input costs, and heavy reliance on China across key segments of battery supply chain are expected to create execution challenges.

Executive summary

India’s battery energy storage system (BESS) segment is entering a critical phase as the country’s clean energy transition becomes increasingly dependent on large-scale storage deployment. India’s cumulative tendered energy storage capacity has grown from 6.8 gigawatts (GW) in 2018 to 90.7GW by 2025. Standalone energy storage system (ESS) tenders, that contract storage capacity without being tied to a specific renewable generation asset, represented more than 71% of the total capacity tendered in 2025, with standalone BESS projects accounting for 60% of this.

Of the 10.4GW of standalone BESS actually allocated, the 2-hour, 2-cycle configuration with a 12-year contract tenor was the most prevalent, representing 57% of the total allocated capacity. The cost of storage, or tariffs, paid by procurers (distribution companies, power generation companies or central agencies like the Solar Energy Corporation of India Ltd [SECI]) to BESS developers declined sharply with the lowest discovered tariffs reaching INR1.48 lakh/megawatt/month (USD1,576/MW/month) for 2-hour systems, and INR2.85 lakh/MW/month (USD3,035/MW/month) for 4-hour systems.

Despite strong procurement momentum, the economic viability of the 2025 standalone BESS bids remains a key concern. Against a benchmark tariff of INR2.3 lakh/MW/month (USD2,449/MW/month) for the 2-hour, 2-cycle configuration, nearly 75% of allocated capacity in this segment falls within the risky category. In contrast, the 4-hour segment appears relatively more viable, with more than two-third of the allocated capacity aligned with the benchmark tariff. In the second half of 2025, tariff reduction accelerated with several large-scale tenders awarded at very low prices, suggesting speculative bidding behaviour.

Execution risks further constrain project realisation. Between 2022 and 2025, tariffs declined by over 71%, far exceeding the 36% reduction in battery pack prices over the same period, indicating a growing divergence between tariffs and the underlying cost structures. During 2025, prices for lithium carbonate, a key input in lithium iron phosphate (LFP) cell manufacturing, in China increased sharply; and now the phased removal of export rebates from April 2026 is expected to further increase landed battery costs in India. Developer capability remains uneven, with only 46.3% of allocated capacity awarded to players with standalone BESS execution capabilities. The financing conditions also remain conservative as lenders typically expect internal rates of return (IRR) in the range of 15–20%.

Execution risks in standalone BESS are expected to have broader implications for the sector. Implementation delays in the range of nine to 18 months may persist due to challenges related to financial closure, procurement and commissioning. Cost pressures at lower tariffs could also lead to compromised asset quality, system reliability and safety. These challenges may ultimately constrain effective renewable energy integration in India’s energy mix.

Revisiting procurement frameworks will be critical to address emerging risks in the standalone BESS segment. This would include introducing cost-reflective tariff floors, tightening eligibility criteria, and revisiting the auction framework to ensure tariffs remain aligned with execution realities. Alongside this, a standardised payment security mechanism will be necessary to improve project bankability. In parallel, domestic manufacturing ecosystem and local supply chains will develop gradually. Introduction of the Approved List of Battery Manufacturers (ALBM), acceleration of cell manufacturing under the Production Linked Incentive (PLI) scheme, and the National Critical Mineral Mission (NCMM), will be essential to support this transition and reduce import dependence over time.

India’s BESS sector is transitioning from the tendering and pipeline stage to execution and on-ground project deployment. Near-term execution challenges could result in delays or cancellations for a portion of the allocated capacity. In the near term, supply chains will remain dependent on lithium carbonate imports from China, with a gradual diversification of sourcing and a shift towards a more diverse technology mix taking place. Ultimately, the pace and scale of energy storage deployment will determine India’s trajectory to achieve its 500GW renewable energy target by 2030.

Related Content