Restructuring PLN's transmission business could lower financing costs and align grid investment with Indonesia's energy transition needs

May 12, 2026 (IEEFA Asia): A new report by the Institute for Energy Economics and Financial Analysis (IEEFA) finds that Indonesia's grid expansion is being constrained not by a lack of policy ambition but by how transmission is financed — resulting in slower build-out, higher financing costs, and a structural mismatch with the country's energy transition goals.

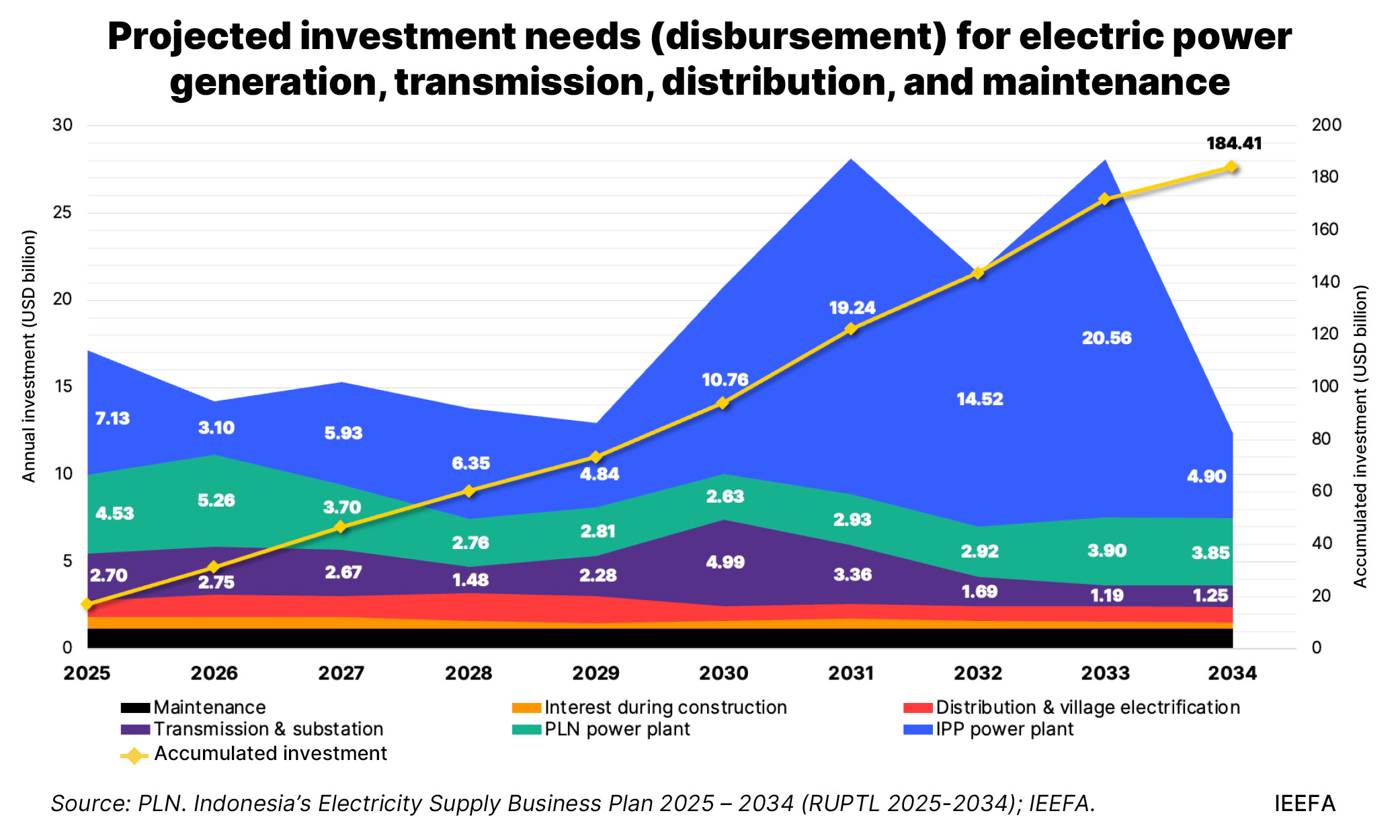

Indonesia's Electricity Supply Business Plan (RUPTL) 2025–2034 requires an average of USD2.4 billion in annual transmission investment, compared with a realized average of just USD1.4 billion annually since 2019. The report finds that closing this gap requires structural reform in transmission financing, not just larger budget allocations.

A low-risk asset, financed as high-risk

Under the vertically integrated structure of Indonesia's national electricity utility, PT Perusahaan Listrik Negara (PLN), transmission investment competes internally with generation development, fuel procurement, distribution expansion, and a range of policy-driven obligations.

“Despite being one of the lowest-risk and most economically productive segments of the power system, transmission is financed through the same corporate balance sheet that absorbs fuel price volatility, foreign exchange exposure, subsidy timing risk, and long-term power purchase commitments,” says report co-author Randi Bachtiar, IEEFA's Energy Finance Specialist, Indonesia.

"By embedding transmission within PLN’s consolidated balance sheet, Indonesia is effectively paying a high-risk cost of capital to finance a low-risk asset," explains co-author Grant Hauber, IEEFA's Strategic Energy Finance Advisor, Asia.

Transmission networks are natural monopolies with stable, predictable, regulated cash flows. Internationally, when financed through ring-fenced regulated entities, they raise long-tenor debt at interest rates only modestly above sovereign borrowing. In Indonesia, however, transmission is invisible to external financiers as a stand-alone asset. PLN's return on equity sits at around 2%, against a cost of funds of roughly 8.5%.

The creation of a PLN transmission subholding through corporate separation, along with a more structured financing model, could improve creditworthiness without changing public ownership. Clearer transmission planning and financing would support Indonesia’s ambitious solar and broader renewable energy targets.

The establishment of Danantara, Indonesia's sovereign investment holding company, which now oversees PLN, further highlights this structural misalignment and the need for reform.

"A ring-fenced transmission company would create the institutional form necessary for Danantara, alongside other domestic and international institutional financiers, to invest in grid expansion on terms that reflect transmission's stand-alone risk profile," says Bachtiar.

The report emphasizes that the most complex aspect of transmission separation — system operations — has already been achieved. PLN already operates its grid through dedicated regional transmission units with system-wide reliability standards and clear operational accountability.

Following PLN's 2022 holding restructuring, the utility now operates through four subholdings with their own balance sheets, boards, and audited financial statements: PLN Indonesia Power and PLN Nusantara Power for generation, PLN Energi Primer Indonesia for fuel and primary energy, and PLN Icon Plus for adjacent services.

A transmission subholding would extend this established model into financial ring-fencing, with regulated tariffs, stand-alone credit standing, and the ability to raise long-tenor infrastructure capital in its own name.

"Indonesia does not need to break up PLN to reform transmission financing," says Hauber. "It needs to complete a process that has already begun — moving from functional to financial separation so that the grid can be financed, expanded, and managed in line with its true economic role."

Domestic and international precedents

The report examines financial ring-fencing experiences among state-owned enterprises in India and Vietnam, as well as within Indonesia through Perusahaan Gas Negara (PGN).

India’s Power Grid Corporation of India Limited (PGCIL) demonstrates how a stand-alone, regulated transmission utility can self-finance capital expansion at a pace consistent with national grid plans. It has raised approximately USD800 million per year, with a weighted average maturity of 10.7 years.

"Over the past decade, the regulated return on equity allowed for transmission investment has been around 15%, leaving PGCIL ample earnings to pay dividends to shareholders and invest self-generated equity into new infrastructure," says Hauber.

In Vietnam, the structural separation of the transmission entity, National Power Transmission Corporation (EVNNPT), from the parent state utility, Electricity of Vietnam (EVN), enabled grid investment to continue through a financial crisis in 2022–2023. EVNNPT sustained record capital investment of approximately USD660 million in 2023, even as EVN recorded consecutive billion-dollar losses.

Reform without privatization

According to the report, a ring-fenced transmission subholding within PLN would also create the legal and commercial basis for revenue streams that the current integrated structure cannot support. These include shared transmission network use for renewable energy developers and corporate buyers, and cross-border interconnection projects. One such project is the proposed Indonesia to Singapore renewable electricity export, in which Danantara has confirmed interest at an investment scale of approximately USD30 billion.

Transparent transmission tariffs enable refinancing, bond issuance, and portfolio-based financing structures that could reduce or even eliminate reliance on state budgets. Enabling electricity exports through infrastructure-based financing models could also reduce cross-subsidies and improve overall project bankability.

The report emphasizes that transmission separation would not imply privatization, market liberalization, or constitutional unbundling. Transmission would remain a regulated monopoly under state ownership, consistent with Indonesia's Electricity Law and recent Constitutional Court rulings.

The report also recommends that the transmission entity be listed on the Indonesia Stock Exchange over time to strengthen governance transparency, attract domestic capital, and support the development of domestic capital markets.

Read the report: Unlocking Indonesia's transmission grid investment

Read this press release in Bahasa

Author contacts:

Randi Bachtiar ([email protected])

Grant Hauber ([email protected])

Media contact: Josielyn Manuel ([email protected])