Debt facility raises concerns over thermal coal exposure, emissions costs

Key Takeaways:

Whitehaven’s market analysis presents an upside case for high-quality coal, but deeper analysis suggests a market facing declining demand and a growing threat from lower-quality substitutes.

The company’s reporting highlights a deteriorating financial position that reflects increased operating costs with growing exposure to emission costs. If not addressed, IEEFA believes annual emission costs could reach between $37.5 million and $60 million at its Narrabri mine alone by 2034.

The increased debt used to fund Whitehaven’s Queensland entry places further financial pressure on all assets. By being secured specifically against Queensland assets, it effectively increases equity exposure to NSW thermal coal assets.

A strategy to reduce the risks of current NSW assets rather than invest in growth would be consistent with Whitehaven’s stated capital management priorities, which stress shareholder returns above growth.

19 June 2026 (IEEFA Australia): Following the signing a new US$900 million loan facility in April, Whitehaven has projected a positive outlook for its thermal coal assets based on expectations of growing demand growth and sustained high prices.

However, new analysis by the Institute for Energy Economics and Financial Analysis (IEEFA) presents a markedly different picture. Published today, the briefing note The canary in the thermal coal mine highlights several key risks that, in IEEFA’s view, could be a concern for investors.

“Our analysis suggests Whitehaven faces an outlook of declining demand and falling prices for its product,” says the note’s author Jonathan Teubner, Lead Analyst – Australian Coal. “In addition, Whitehaven’s own reporting points to a deteriorating financial position, with increased operating costs, and growing exposure to emission costs. The debt burden places further financial pressure on all the company’s assets.”

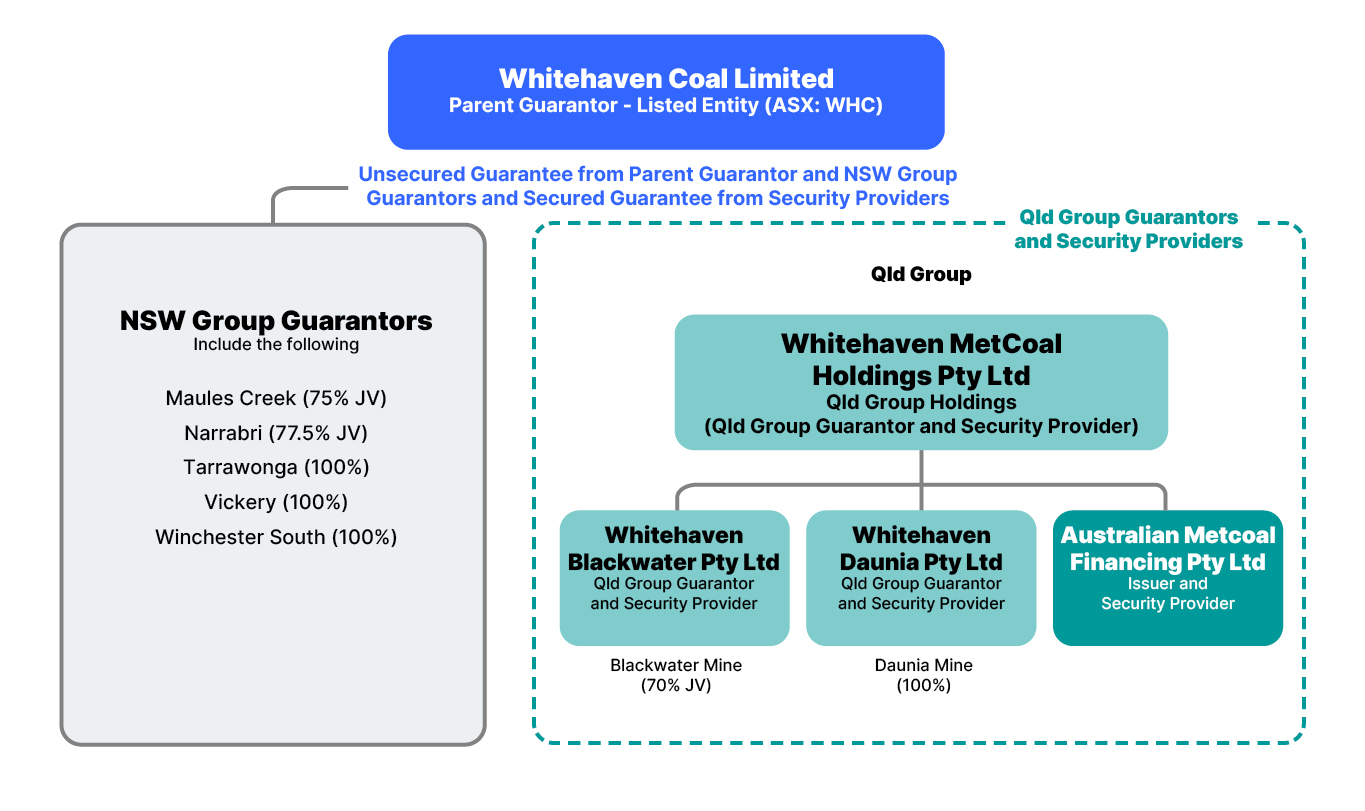

Acquired through Whitehaven’s subsidiary Australian MetCoal Financing (AMCF), the loan facility will be used to pay down debts from the acquisition of the Blackwater and Daunia metallurgical coal mines in Queensland in 2024. In a prospectus released to accompany the loan, the company presented an optimistic forecast for its New South Wales (NSW) thermal coal assets. This was based on projections of growing demand, mainly in Asia, for the high-quality coal produced by its NSW mines, with prices anticipated to rise for the coming decade.

IEEFA examined the analysis underpinning Whitehaven’s forecasts, which drew heavily on modelling by consultants Commodity Insights and Wood Mackenzie. Comparison of this with another assessment by Wood Mackenzie for another coal producer raised questions about various assumptions contained in Whitehaven’s prospectus, concerning future pricing trajectories and the long-term demand for higher-grade coal.

“Most notably, prices are only projected to rise in a scenario where the global energy transition to net zero is delayed,” says Teubner. “In other scenarios where transition occurs sooner, the price trends are downward. In other words, the price growth Whitehaven forecasts is based on a scenario where global temperatures rise 3.1 degrees by 2100.”

IEEFA’s analysis also highlighted significant financial challenges for Whitehaven. Its NSW thermal coal mines are facing increasing costs while the outlook for prices is likely trending downwards. This suggests a future of increasing pressure on margins, placing significant pressure on the NSW assets’ future economic viability. For the Queensland mines, the cost of financing their acquisition has combined with decreased revenue to deliver an underlying loss.

Whitehaven’s corporate structure also raises concerns over shareholders’ risk exposure. In the prospectus, the Queensland mines Blackwater and Daunia are placed alongside AMCF, with their assets used to secure the financing of the new loan facility. This means investors in Whitehaven Coal Limited, the parent guarantor, have less security from the performance of the Queensland assets, leaving their risk positions heavily weighted to NSW thermal coal assets.

Teubner explains: “The AMCF transaction dilutes the equity exposure to the performance of met coal assets – and more broadly to the metallurgical coal market and its differing risk profile to the market for thermal coal. Shareholders who based their increased investments on Whitehaven’s acquisition of the Queensland assets may want to consider the impact of this dilution and their consequently enhanced proportional risk exposure to NSW thermal coal assets.”

Moreover, Whitehaven’s prospectus offers limited detail on potential emissions exposures under the Safeguard Mechanism, though this appears to be a further cost category under pressure. The most emissions-intensive of Whitehaven’s mines, Narrabri produced 511,474 tonnes of Scope 1 emissions in FY2025. Assuming production rates remain unchanged, IEEFA’s analysis suggests the potential Safeguard liabilities for Narrabri could rise to between AU$37.5 million and AU60 million in 2034.

“The combination of cost increases and exposure to softening market prices, along with future Safeguard liabilities, points to significant risks to the future profitability of thermal coal operations in NSW,” says Teubner.

In IEEFA’s view, equity investors are facing increased exposure to a growing array of risks associated with Whitehaven’s NSW thermal coal assets. This has been compounded by the debt financing structure established to enable the purchase of the Queensland met coal assets.

In its prospectus, Whitehaven describes a capital allocation framework in which surplus capital is only used to pursue growth projects once operations are optimised, the balance sheet is strong and it is delivering returns to shareholders. In other words, the company prioritises capital returns to shareholders over growth investments.

“We believe it would not be unreasonable for shareholders to hold Whitehaven to its stated capital management priorities,” says Teubner. “A strategy to reduce the risks of the current NSW assets – rather than investing in growth – would be consistent with this commitment.”

This analysis is for information and educational purposes only and is not intended to be read as investment advice. It is subject to our disclaimer. Please click here to read our disclaimer.

Read the report: The canary in the thermal coal mine – Whitehaven’s debt prospectus highlights increasing risks for equity investors

Media contact: Amy Leiper, ph +61 414 643 446, [email protected]

Author contacts: Jonathan Teubner, [email protected]

About IEEFA: The Institute for Energy Economics and Financial Analysis (IEEFA) examines issues related to energy markets, trends, and policies. The Institute's mission is to accelerate the transition to a diverse, sustainable and profitable energy economy. (ieefa.org)