Unlocking the clean energy potential of Australian business rooftops

Download Full Report

View Press Release

Key Findings

C&I solar and storage has significant untapped potential in Australia. Installed C&I solar capacity is 5.6GW, with 17-31GW forecast by 2050, and the technical rooftop potential could be even higher.

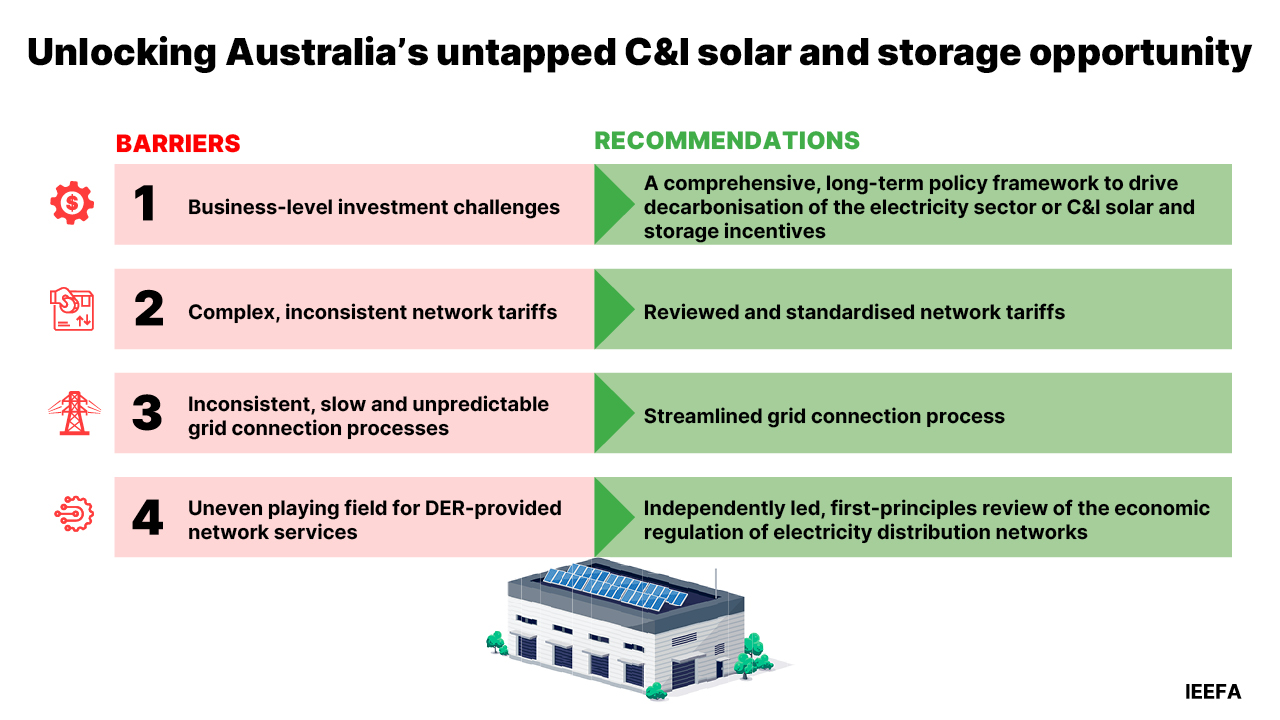

A range of barriers are constraining uptake, including business-level investment barriers, complex and inconsistent network tariffs and slow and unpredictable grid connection processes.

These barriers can be overcome through improved incentive schemes, reviewed and standardised network tariffs, a streamlined grid connection process, and a first-principles review of distribution network economic regulation.

Unlocking the C&I solar and storage sector could help accelerate renewable supply and storage additions, serve business energy demand, and reduce energy costs for businesses.

Executive summary

Australian households are playing a leading role in Australia’s transition to renewable energy, with the power-generating capacity installed on household roofs roughly equal to that of coal power stations. In addition, almost half a million small-scale batteries will have been installed in the first year of the federal government’s Cheaper Home Batteries Program. However, we have not seen the same scale of action in Australia's commercial and industrial (C&I) sector even though it consumes substantially more electricity than the household sector, and that usage is biased towards daytime solar hours. Just 5.6 gigawatts (GW) of solar is installed on C&I premises today against a forecast capacity of 17–31GW by 2050, and the technical rooftop potential could be even higher still. C&I storage deployment is well behind households, although demand is increasing quickly.

For the purposes of this report, the C&I sector encompasses any non-residential, non-utility energy user, from manufacturers and retailers to farms, hospitals, and schools. This sector could play a far larger role in accelerating Australia’s energy transition; in fact, it must play a larger role if the country is to meet its renewable energy targets. The National Energy Market (NEM) and Western Australia’s South West Interconnected System (SWIS) grids are tracking below the pace of renewable supply additions needed to meet the 82% renewables target, and C&I solar can help fill that gap. It can be deployed faster than utility-scale alternatives, because it generally doesn’t require extensive planning and environmental approval processes, nor new transmission build that can add several years to the roll-out of utility-scale power projects. It is also well suited to serving typical business demand profiles, supports energy cost reductions and competitiveness for businesses, and contributes to emissions-reduction goals.

Despite the significant market potential and benefits, C&I solar and storage continues to have low annual installation levels, as it is constrained by four key barriers. These key barriers were identified by IEEFA through interviews with stakeholders and our own analysis.

Business-level investment barriers

There are a number of business-level investment barriers constraining C&I solar and storage uptake.

- As has been well documented in historical research into investment in energy efficiency, because C&I solar and storage investments are usually deemed non-core business expenditure, managers tend to apply high return thresholds for these investments above the actual cost of capital.

- As most businesses rent their premises, landlords will usually be the final decision-makers on solar and battery investments. Yet because the landlord doesn’t pay the energy bill, they see little to no financial benefit from these systems, so have limited incentive to help drive the project forward. Tenants are also often on leases shorter than the life of a solar and storage asset, meaning they often cannot capture the full return on an investment they fund themselves.

- In many cases, government incentive schemes intended to correct for the negative externality of carbon pollution exclude the C&I sector or are being phased out. C&I is effectively the “missing middle” because systems are typically too large for residential incentives, such as the Cheaper Home Batteries Program, but too small for the utility-scale Capacity Investment Scheme. The value provided by certificates under the federal government’s Renewable Energy Target – via Large-scale Generation Certificates (LGCs) and Small-scale Technology Certificates (STCs) – is declining rapidly. This means C&I solar systems receive significantly less support than previously, and the support they do receive is generally well below the value of carbon abatement estimated by the Australian Energy Regulator (AER).

To help counter the sub-optimal level of investment in C&I solar and storage arising from these issues, governments need to develop a comprehensive, long-term framework to drive decarbonisation of the electricity sector. It should support all forms of zero emissions energy, irrespective of scale, and the value of that support should align with the AER’s guidance on the value of emissions reductions. At the very least, policy support should align with the value paid for abatement under the federal government’s Safeguard Mechanism. In the absence of a comprehensive decarbonisation framework, or as an interim step, governments should seek to address some of the holes in the existing, patchwork approach by introducing incentives to help the “missing middle” of C&I solar and storage overcome business-level investment barriers.

Complex and inconsistent network tariffs

Australia has 16 different distribution network service providers (DNSPs), each of which has been free to develop its own distinct network tariff structures. The result a fragmented and inconsistent network tariff landscape for C&I distributed energy resource (DER) project proponents operating across DNSP boundaries. Tariff structures vary significantly across DNSPs, making it difficult for businesses to model investment returns, develop software and control systems to manage batteries, and develop nationally scalable business models. In this report, we examine demand charges, which can be up to 40% of business’s electricity bills. We find they are inconsistently applied across DNSPs, differing based on the lasting cost of a single spike, when peak demand is measured, how charges differ across seasons, and the complexity of the demand charge structure. This creates significant complexity and cost for C&I solar and storage providers (and electricity retailers). Further, the window in which demand charges are applied can often be so wide that it does not appear to adequately enable businesses to shift loads away from network peak periods. This could be reducing the ability of network tariffs to incentivise long-term network cost reductions.

Given this, network tariff structures should be reviewed by the AER to reduce the number of tariff structures, standardise them at a national level (or at least NEM-wide level) and ensure they send a clear incentive to consumers to manage their demand (or export power to the grid) where this could reduce the need for costly network upgrades. In addition, to prevent the complexity problem re-emerging, responsibility for tariff design should be given to the AER rather than individual DNSPs.

Inconsistent, slow and unpredictable grid connection processes

An inconsistent, slow and unpredictable grid connection process imposes material costs and delays on C&I projects. There is a lack of consistency in the grid connection processes and technical requirements for connection across DNSPs even though the technology involved is the same. In IEEFA’s interviews, we heard reports of grid connection timelines ranging from a few months to a year or more for more complex projects or those with a number of iterations in the connection application process. We also heard reports of certain Australian DNSPs regularly taking longer than others to process applications. DNSPs retain discretion over specific technical requirements, meaning proponents can face different technical requirements for systems in different areas. Additional technical requirements can also emerge during the process rather than being stated upfront, creating iterative revision loops that compound delays and cost. There is also a lack of consistent and easily accessible information on the degree to which different parts of the network could host solar capacity, making it harder for consumers and the solar industry to make well informed decisions about where they should be pursuing solar projects. The grid connection process should be streamlined, through a range of measures outlined below:

- A fast-track connection pathway should be developed (similar to residential systems) for C&I projects that adhere to a standard technical architecture that mitigates power quality and safety risks. This should be developed by the Clean Energy Regulator’s National Technical Regulator for Consumer Energy Resources with input from DNSPs and the C&I sector.

- Technical requirements should be harmonised across Australia (or at least NEM-wide) with the Clean Energy Regulator’s National Technical Regulator for Consumer Energy Resources playing a key role.

- DNSPs should be required to publish granular data on DER hosting capacity by location via a national, publicly accessible online portal.

- DNSPs should be required to publish data on C&I grid connection application processing timeframes, which should be collated and compared as part of broader network reporting processes.

- DNSPs should be incentivised to process grid connection applications quickly.

Uneven playing field for DER-provided network services

Distributed solar and storage can deliver value to the network through services such as voltage support, congestion management and reduced or deferred network augmentation. The Regulatory Investment Test for Distribution (RIT-D) includes an options screening process in which DNSPs judge whether technological competitors (such as C&I solar and storage) might do a better job of serving an identified network need than upgrading their own network assets (over which they have exclusive licence). However, how this process is run is largely not conducive to effective competition from non-network alternatives in the form of C&I solar and storage. Other elements of the economic regulation regime also appear to constrain the consideration of non-network alternatives such as DER. Australia is not alone in grappling with these issues - momentum is growing internationally towards reform of the economic regulation of electricity networks. An independently led, first-principles review of the economic regulation of distribution networks should be undertaken. This should examine the potential for non-network solutions such as DER to compete with traditional poles and wires investment.

Together, these structural barriers to C&I solar and storage investment are preventing the sector from reaching its full potential at speed. The recommendations in this report offer a set of solutions to address the barriers and enable the C&I sector to be scaled up at pace, helping serve demand as coal exits, and supporting Australia in attaining its emissions reduction goals while reducing energy costs for businesses.

Related Content