South Korea's coal phaseout should not balloon LNG use and erode energy security

Key Findings

South Korea’s pledge to phase out 40 of 61 coal-fired power plants (CFPPs) by 2040 raises concerns that retired coal capacity may be replaced with liquefied natural gas (LNG) rather than renewables, undermining expected reductions in greenhouse gas (GHG) emissions.

South Korea has committed to purchasing approximately USD100 billion worth of energy from the United States (US), including LNG. As of February 2026, uncertainty persists over whether the agreement will proceed, given indications that the US could increase reciprocal tariffs from 15% to 25%.

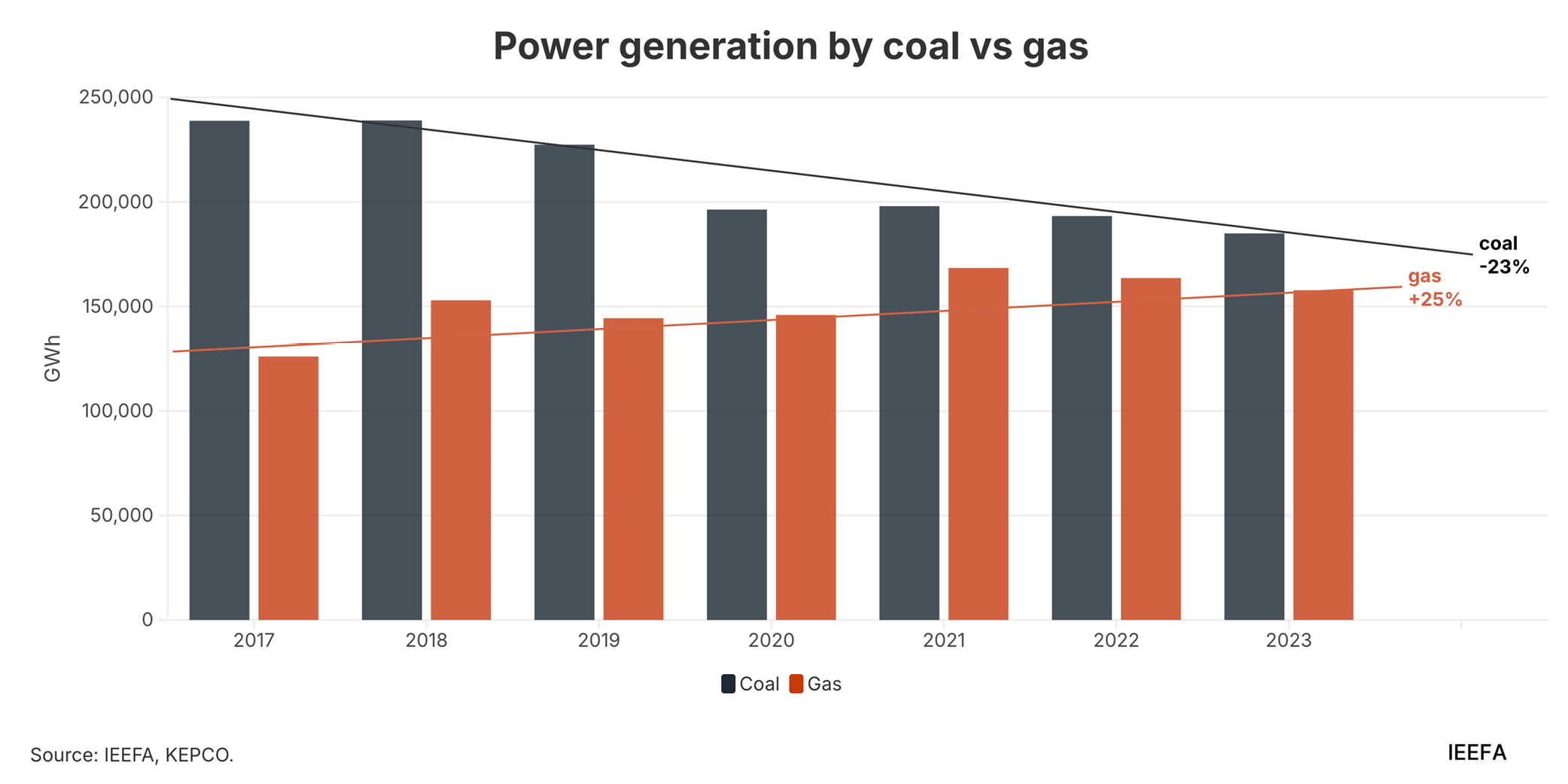

From 2017 to 2023, coal-fired power generation decreased by 23% while gas-fired generation increased by 25%. Over the same period, carbon dioxide (CO2) emissions from coal power decreased to 185 million tonnes, while gas power emissions increased to 77 million tonnes. This suggests that a coal phaseout, replaced by LNG, may not achieve meaningful GHG reductions.

South Korea’s 11th Basic Plan for Long-Term Electricity Supply and Demand (BPLE) outlined ammonia and hydrogen co-firing targets of up to 2.41% in its power mix by 2030. However, policy signals indicate that these plans may be abandoned or significantly reduced.

During the 30th Conference of the Parties (COP30), South Korea joined the Powering Past Coal Alliance (PPCA) and pledged to phase out coal-fired power plants (CFPPs) by 2040. This goal raises concerns about a potential ‘balloon effect’, where reductions in coal use may lead to an increase in liquefied natural gas (LNG)-fired power.

Coal phaseout and an increase in US LNG imports planned in parallel

In the past, similar coal phaseout strategies for decarbonization resulted in higher LNG generation as a trade-off. There were two main drivers behind the shift from coal to gas: the misleading narrative that gas is “green,” and the concurrent geopolitical push to increase LNG imports from the United States (US).

South Korea’s coal phaseout ambition dates back to 2017, when the Coal and Nuclear-free Economy policy was announced at the Group of 20 (G20) Summit. This supported the narrative that LNG is a ‘green energy’ in the energy transition pathway, and the targeted share of LNG in the national power mix was increased from 16.9% in 2017 to 18.8% in 2031 in the 8th Basic Plan for Long-Term Electricity Supply and Demand (BPLE).

In reality, the share of LNG in the power mix increased far more sharply, growing from 23% in 2017 to 26% in 2020. In 2017, the US share of South Korea’s LNG imports more than doubled year-on-year, coinciding with the start of the Korea-US Free Trade Agreement (FTA) renegotiation, followed by US LNG imports hitting a historic high in 2021.

Based on previous experience, there are growing concerns about increased LNG use from 2026 onward. Following tariff negotiations in mid-2025, South Korea has committed to purchasing around USD 100 billion worth of energy from the US, including LNG. As of February 2026, it is unclear whether this agreement will proceed, as the US has indicated that it could increase its “reciprocal tariff” from 15% to 25%. The volume and duration of imports are also uncertain, though South Korea may import 9 to 10 million tonnes of US LNG annually, according to estimates.

For context, in 2024, South Korea imported around 5.6 million tonnes of LNG from the US, representing 12% of its total annual LNG imports of 46.33 million tonnes.

At COP30, South Korea pledged to retire 40 of 61 CFPPs by 2040 and to build no new coal plants without greenhouse gas (GHG) abatement. However, if the coal phaseout is achieved by increasing LNG-fired power rather than renewable energy, as seen earlier, the expected GHG reductions may be undermined.

Revitalizing LNG jeopardizes net-zero, raises supply chain carbon risks

Since 2017, CFPP phaseout plans have mainly been implemented through coal-to-gas conversion. The 11th BPLE outlined that 40 coal-fired power plants would be replaced by LNG and “zero-carbon” generation, potentially including unproven technologies such as hydrogen co-firing and carbon capture and storage (CCS). The remaining 21 coal plants currently lack a clear transition plan, but are expected to be replaced by renewables and zero-carbon energy sources. However, if South Korea’s coal phaseout pledges are implemented in parallel with increased LNG use, achieving its net-zero target and mitigating supply chain carbon risks could become increasingly challenging.

South Korea’s power-sector carbon intensity (CI) was around 436 grams of carbon dioxide emitted per kilowatt-hour (gCO2/kWh) in 2022, which includes coal (approximately 1000 gCO2/kWh) and LNG-based generation (about 490 gCO2/kWh). From 2017 to 2023, coal-fired power generation in South Korea decreased by 23% to 184,927 gigawatt-hours (GWh), while gas-fired generation increased by 25% to 157,729GWh. Over the same period, carbon dioxide (CO2) emissions from coal power decreased to 185 million tonnes, while gas power emissions increased to 77 million tonnes.

This suggests that replacing coal with LNG-fired power generation may not deliver substantial GHG reductions, given the ambitious Nationally Determined Contribution (NDC) targets.

South Korea’s latest Nationally Determined Contribution (NDC) target outlines a reduction of between 53% and 61% in GHG emissions from the 2018 level by 2035 — significantly more ambitious than the previous 40% emissions reduction target for 2030. Achieving this new target will require a faster and more comprehensive phaseout of fossil fuels.

However, phasing out coal by increasing LNG imports, along with expanded US LNG purchase commitments, could lock South Korea into long-term fossil fuel dependence, undermining its plan to reduce LNG’s share of the power mix to 10.6% by 2038. Additional LNG imports also present risks amid an impending global supply glut and anticipated declines in demand and prices. Overreliance on LNG could exacerbate stranded asset risks, including the overbuild of LNG receiving terminals, as demand falls and pressure for the energy transition accelerates.

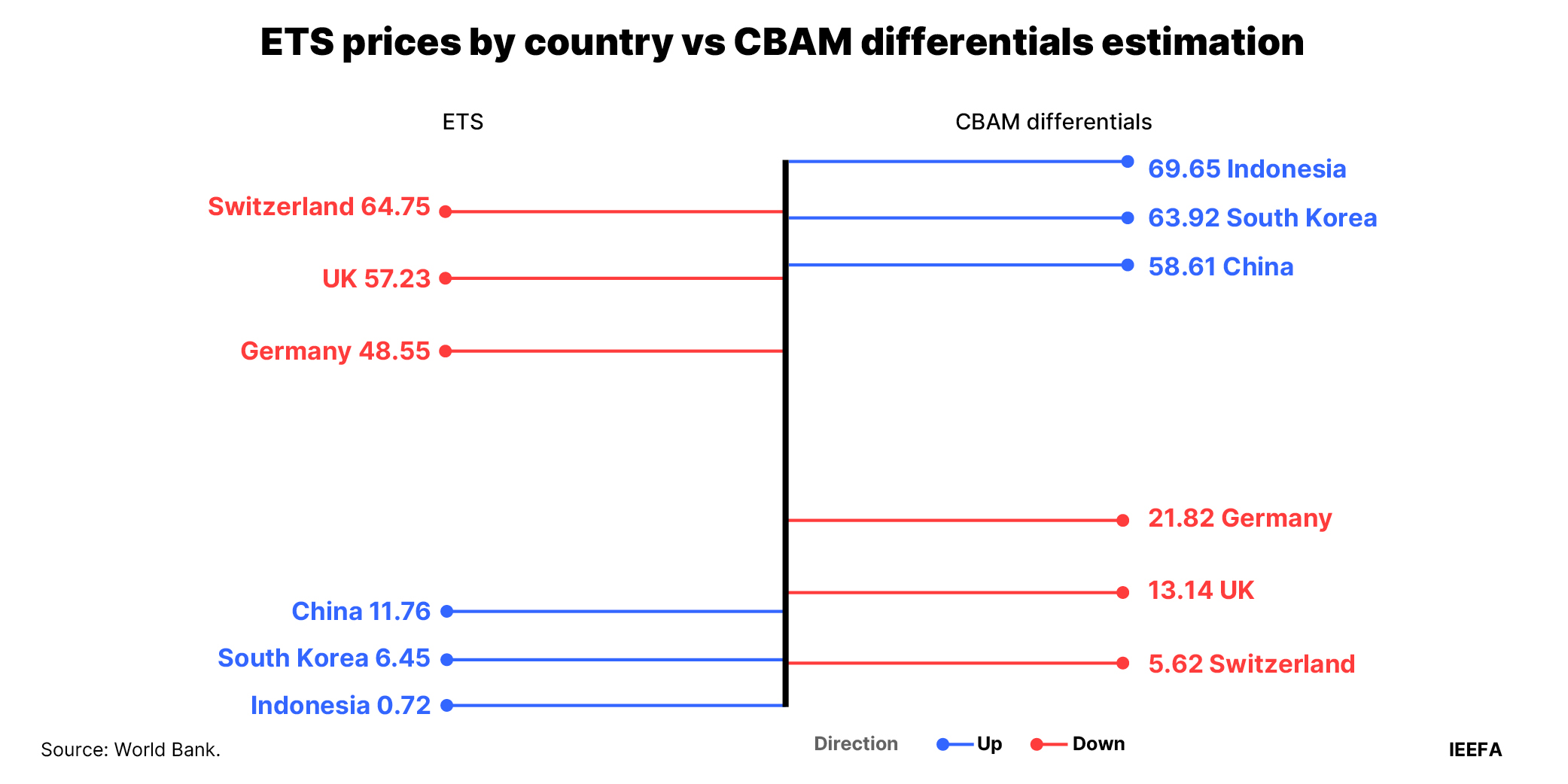

With the recent full implementation of the European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM, rising supply chain carbon risks in LNG-powered semiconductor clusters and Artificial Intelligence (AI) data centers could increase counterparty risks and production expenses. South Korea's limited renewable energy supply further constrains data center investment and heightens carbon cost exposure due to significant differences between the EU Emissions Trading System (ETS) and South Korea’s ETS (K-ETS) prices.

Continued reliance on fossil fuels, particularly LNG, exposes energy security to escalating geopolitical tensions, such as the Russia-Ukraine war and the recent US-Israel war with Iran. LNG prices reached record highs in early 2022 following Russia’s invasion of Ukraine, triggering sharp increases in wholesale electricity prices in South Korea, which relies heavily on a fossil fuel-intensive power mix (58.5% in 2023).

Ammonia-coal co-firing is likely to decline

The latest coal phaseout pledge signals that ammonia co-firing in CFPPs will likely be abandoned or significantly reduced from what was planned for in the 10th and 11th BPLE.

South Korea’s 11th BPLE, released in February 2025, highlighted hydrogen and ammonia co-firing in gas and coal-fired power generation, targeting a 2.41% share of the power mix by 2030 and 6.23% by 2038. These targets were slightly higher than the 10th BPLE, which planned for 2.1% hydrogen/ammonia co-firing by 2030.

There is increasing policy uncertainty regarding both ammonia-coal and hydrogen-LNG co-firing plans, as outlined in the two previous BPLEs. In October 2025, the South Korean Ministry of Climate, Energy and Environment cancelled the Clean Hydrogen Power Generation Bidding (CHPS), which was intended to subsidize hydrogen and ammonia co-firing projects. Globally, apart from a few small prototype units, no commercial-scale power plant using hydrogen or ammonia has become operational, and there is no evidence that co-firing in gas turbines will be economically viable for at least the next decade.

There is growing speculation that only clean hydrogen co-firing with LNG plants would be eligible for government subsidies. However, currently there is no clear policy for managing ammonia-coal co-firing. The preliminary 12th BPLE, which is expected to include detailed energy transition plans and guidance on managing technologies, such as hydrogen and ammonia co-firing, will likely be released in the first half of 2026.

IEEFA recommends that the upcoming 12th BPLE outline a pathway to achieve a phase out of coal without increasing LNG dependence, while accelerating renewable energy deployment to help mitigate supply chain carbon risks for South Korean industries.

Related Content