Key Findings

Bangladesh’s new rooftop solar programme sends a strong signal on the country’s commitment to shore up renewable energy capacity amid its limited success thus far.

Achieving new rooftop solar capacity of 3,000 megawatts (MW) in less than six months would require scaling up installations to more than 12 times the capacity of 245MW recorded in June 2025.

With the combined power demand in government offices, hospitals, educational and religious institutions being less than 1,500MW, their sanctioned load is much less than 3,000MW. This limits the possibility of achieving rooftop solar capacity of 3,000MW in these facilities under net metering guidelines.

Rooftop solar is a low-hanging fruit, which can help the country attain its new renewable energy target of 30% by 2040. However, with many unknown factors like actual rooftop solar potential and maintenance issues in the CAPEX model still unresolved, the government must design measures for readiness to dispel stakeholder concerns.

Bangladesh is struggling to boost its renewable energy capacity amid the energy crisis and spiralling power tariffs. Against this backdrop, the government’s announcement of a new programme to install rooftop solar capacity of 3,000 megawatts (MW) by December 2025 comes as a boost to the sector.

But the question remains whether the target is overly ambitious, given that Bangladesh installed rooftop solar capacity of only 245MW between June 2008 and June 2025. This requires the country to ramp up efforts by more than 12x to achieve 3,000MW by December 2025.

As government offices, hospitals, educational and religious institutions are unlikely to offer adequate sanctioned load to install 3,000MW rooftop solar, the Sustainable and Renewable Energy Development Authority needs to assess and document rooftop solar potential in these buildings. Furthermore, fund allocation for various projects, tendering, evaluation of bidding documents, issuing work orders and project implementation will likely require an extension of the December 2025 deadline. Only 15-20 high-quality Engineering, Procurement and Construction companies operate in the country, and they may not have enough capacity to install 3,000MW in less than six months.

Under Bangladesh’s new rooftop solar programme, government offices will roll out installations via the CAPEX model supported by public funds, while hospitals and educational institutions will operate under the OPEX model with no upfront cost.

There are pros and cons to both models. While the CAPEX model allows for faster rollout and higher savings, there could be risks stemming from poor coordination, lack of maintenance, and rushed developer selection. On the other hand, the OPEX model ensures quality, but offers lower savings, and could face financing hurdles and risks from load-shedding in rural areas. If projects are small and scattered in rural areas, they may fail to attract companies to invest in the OPEX model.

The risk of soiling could significantly reduce solar energy yield per annum, hence the government must instruct public offices to create a fund from the monthly savings in projects under the CAPEX model and enter long-term maintenance contracts with service providers. Utilities should also find a way to address load-shedding in rural areas, as the resulting solar generation loss could pose risks under the OPEX model.

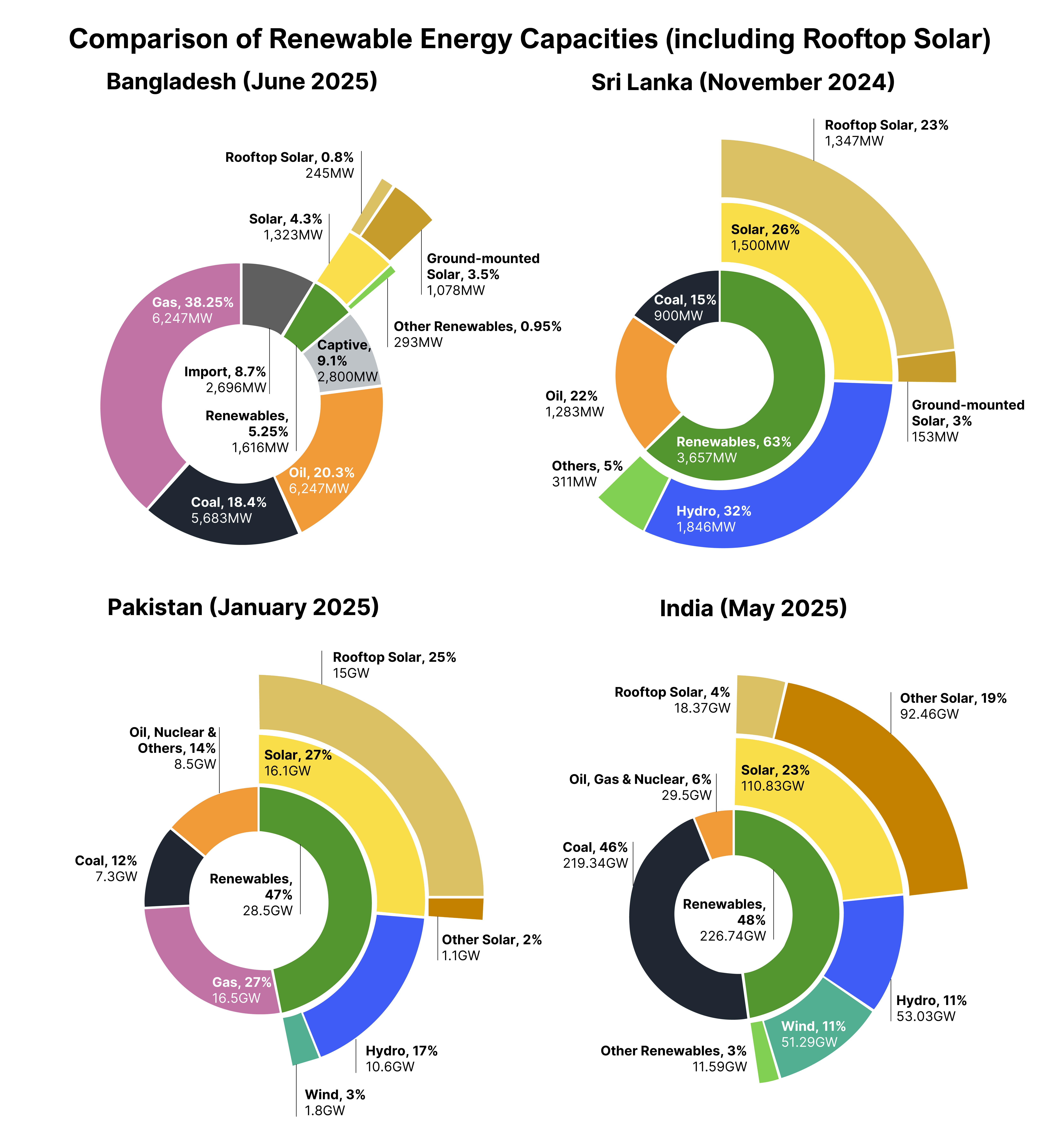

Bangladesh can draw on the experience of its neighbours, like India, Pakistan and Sri Lanka, which boast a greater share of renewable energy in the power mix, ranging from 47% to 63%.

For instance, Pakistan’s rooftop solar sector success is an example that push factors, such as energy supply crunch and unaffordable power tariffs, can spearhead change.

In Sri Lanka, the government addressed financing barriers to expand rooftop solar, supported by a multilateral agency. Later, the government provided funds for rooftop solar on public buildings. Similarly, India’s rooftop solar capacity of more than 18 gigawatts in May 2025 can be attributed to the consistent policy and regulatory support extended by the government.

As Bangladesh’s rooftop solar sector is still at a nascent stage, capacity development of key stakeholders and government agencies will be important for the programme’s success. Besides, the government needs an independent monitoring mechanism to ensure that projects operate smoothly.

Related Content