Key Findings

Volatile demand and supply, sharp swings in the prices of critical mineral inputs, long gestation periods, and high upfront capital requirements limit the flow of capital into the critical minerals sector.

While the National Critical Mineral Mission (NCMM) aims to create regulatory and institutional enablers to develop the critical minerals supply chain, focused capital expenditure is needed to accelerate large-scale mining, refining, and processing. The NCMM creates intent and incentives, but outcomes will depend on institutional execution.

For India to achieve its climate goals, the government must move beyond policy frameworks. It should focus on de-risking projects, ensuring that the critical minerals industry is commercially viable.

Context

The global energy transition, while encouraging, is moving at a much slower pace than needed. One of the major hurdles is the difficulty in securing critical minerals as their production, refining, and processing are concentrated in few countries, mainly China.

China dominates the critical minerals landscape; it accounts for ~51.7% of the world’s known rare earth reserves, followed by Brazil (~25.7%). For high-demand minerals such as lithium, nickel, and cobalt, China accounts for only 10–30% of global raw extraction, but dominates 60–70% of refining and processing capacity, and approximately 90% of rare earth refining. Between 2020 and 2024, most growth in the refined output of key energy minerals was driven by a few suppliers. For copper, lithium, nickel, cobalt, graphite, and rare earth elements, the combined market share of the top three producers (Indonesia, the Democratic Republic of the Congo and China) rose from about 82% in 2020 to 86% in 2024. In addition to the concentration of the critical minerals supply chain, resource nationalism is also shaping the sector’s dynamics. For instance, Indonesia has imposed export bans on raw nickel (2020) and bauxite (2023), while Zimbabwe has suspended exports of all raw materials and lithium concentrates. These export bans and tariffs give countries geopolitical leverage over market conditions and trade.

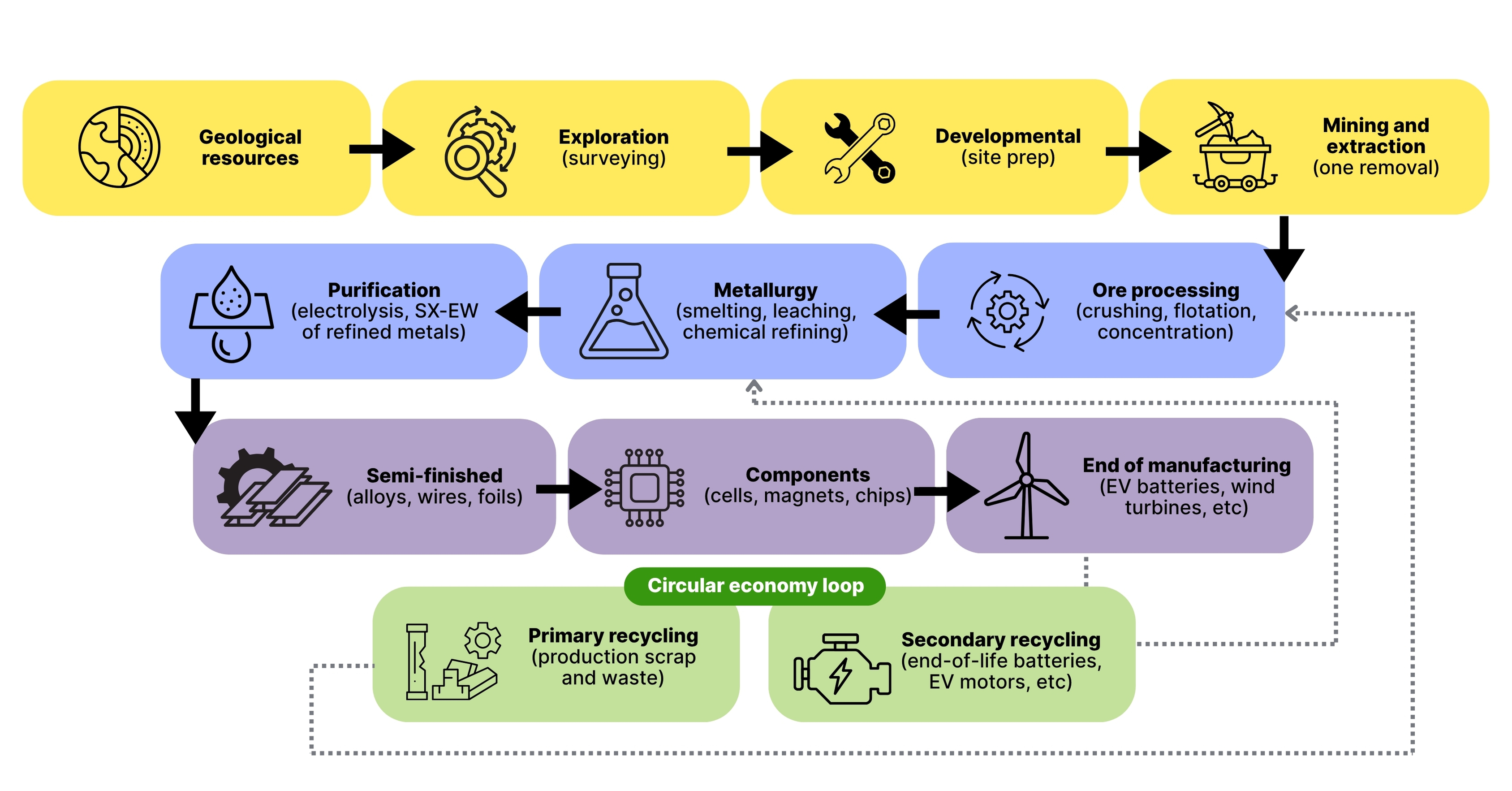

Figure 1: Critical minerals supply chain

In the midst of these developments, countries have been striving to accelerate the energy transition but are also rethinking their plans, in some cases pausing renewable energy capacity additions, particularly as access to critical minerals across the value chain is being used as political leverage. Energy security has been one of the key drivers of the transition but relying on a few countries for critical minerals could temporarily halt progress or even reverse it. In this scenario, some countries like the US, India, and the EU are making an attempt to diversify their supply chains and ramp up domestic manufacturing capabilities.

Like most other countries looking to advance the energy transition, India needs a massive volume of critical minerals to augment its domestic clean technology manufacturing. India imports 100% of lithium, cobalt, and nickel for manufacturing and intermediate green products. India has adopted a two-pronged approach to boost its energy transition by 2030 and beyond: strengthening domestic capacity and securing access to global critical mineral supply chains.

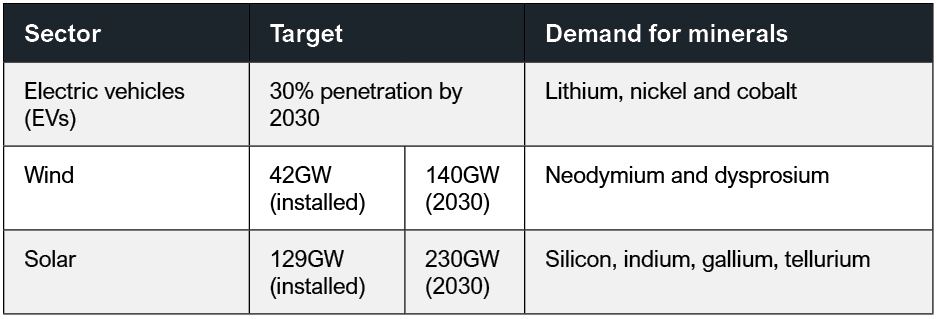

Table 1: India’s critical minerals: Key sectors and minerals required

Source: Press Information Bureau (PIB)

Meeting the rising demand will require significant investment across the critical minerals supply chain over the next two decades. Much of this investment is front-loaded and involves risks that may not naturally attract private investors. The key question is whether private capital is being deployed adequately in this sector, which is crucial to India’s green energy ambitions and energy security.

This briefing note highlights financing challenges across the supply chain, i.e. from upstream exploration to capital-intensive midstream processing. Furthermore, it evaluates the current institutional and policy enablers, identifying areas where current schemes fall short in financing projects.

Related Content