IEEFA update: India’s coal-fired power plant stockpiles reach record levels even as electricity demand weakens

The 2019/20 financial year has been full of surprises.

Coal production in India is back on an upwards trajectory after a significant decline mid-year. Total coal stockpiles are close to record highs and those at power plants have reached a new peak, even as on-grid coal-fired power generation has declined by an unprecedented 2.5% year-on-year. And after a strong start, India’s overall electricity generation grew at just 0.8% year-on-year, a tiny fraction of the 6% annual growth seen this past decade. This is a clear reflection of the economic headwinds that have emerged and coal’s reduced competitiveness.

EVEN WITH THESE ANOMALIES THE ENERGY TRANSITION IS CONTINUING, and India is still making positive moves to embrace the strategic benefits it is bringing. Only this week India announced plans for 20 gigawatts (GW) of new solar tenders to be launched in the next 15 months to June 2021.

India’s power plants have a record average of 444 tonnes of coal per MW of utilised capacity on their hands.

Record high coal stockpiles

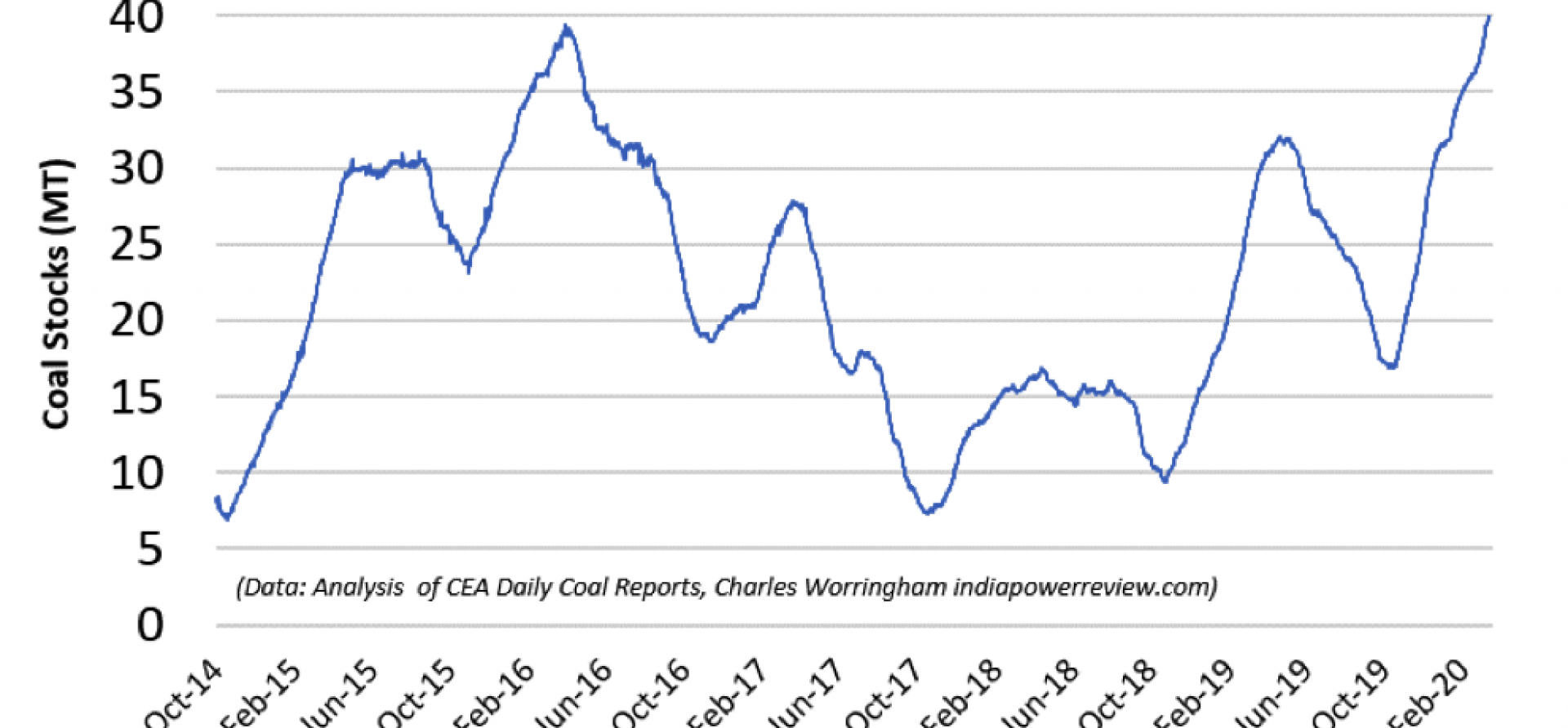

The quantity of coal stockpiled at India’s power plants surpassed 40 million tonnes (Mt) on 15 March 2020, having a few days earlier eclipsed its record high of 39.5Mt on 31 March 2016.

Even though India has made a net addition of 9% thermal capacity since March 2016, this was offset by a decline in average thermal capacity factor from 62.3% to 56% (as at the end of February).

As a consequence, India’s linkage-based thermal power plants now have an average of 444 tonnes of coal on their hands for each megawatt (MW) of utilised capacity, compared to 415 tonnes at the previous record high in 2016.

There have been some large oscillations in India’s coal stockpiles over the last five years. During the most recent trough in late 2017 and 2018, over thirty plants had less than seven days’ supply and headlines warning of critical shortages were commonplace, putting economic growth at real risk.

In contrast, during the previous highs in 2016 and early 2017, the abundance of coal made deterioration and spontaneous combustion of stockpiles the more pressing concerns. With the added problem of drought-induced shutdowns some plants, such as Raichur thermal power station, were literally running out of space to store coal at that time.

NOW IN 2020, POWER PLANTS HAVE AGAIN REACHED RECORD HIGH STOCKPILES. Coal India has systematically drawn down its pithead stocks by upping the ratio of dispatch to production. Their pithead stocks now stand at slightly over 40Mt, about half of their peak in March 2017. This means the total amount of stockpiled coal in India was about 82Mt at the end of February when the government-owned coal mining company SCCL’s pithead numbers are included, rising to a new reported high of 88Mt on 12 March.

Indian Power Plant Daily Coal Stocks 1 October 2014 – 15 March 2020

All up, this is still less than the 105Mt that India reached during its previous high in March 2017. However, the additions to stockpiles at power plants have exceeded reductions in those at the mines. And with economic growth and hence electricity demand flat-lining, the annual peak has been edging back up and may again push through the record peak this year. This will be assisted by the month of March normally marking both a period of generally favourable weather and the end of the Indian financial year, which typically sees big spikes in coal production and dispatch.

The increasing stockpile is an outcome of both the downturn in coal consumption for power generation in the second half of this financial year (2019/20), and the product of a stalling Indian economy, strong hydro generation and the resolution of temporary supply problems, such as from the inundation of Coal India’s Dipka mine in October 2019.

India’s electricity production is flatlining overall

Having staged a recovery in late January and February relative to 2019, electricity demand has slackened again in March 2020, and coal-fired power has continued to bear the brunt of this dip. Thermal power, being the highest marginal cost of production, bears the heaviest burden of any demand weakness.

Cumulative Generation – Difference Between FY2019-20 and FY 2018-19

The financial year (FY) 2019/20 looks set to end with India having generated about 10-12 terawatt hours (TWh) more electricity than the previous year (+0.8% year-on-year vs 1,379TWh in 2018/19). This is on the back of increased hydro (+22TWh), solar (+10TWh) and (to a lesser degree) nuclear generation (+5TWh). A poor wind season and a lack of new capacity development means wind generation is in line with 2018/19 levels, and gas is down marginally.

These increases have combined to more than offset coal’s 25TWh decline in 2019/20, the largest decline in a decade. The next financial year will start with record amounts of coal stockpiled at India’s power plants and considerable uncertainty as to how much is really needed in light of weak coal power generation.

This burgeoning stockpile also gives a clear perspective on Coal Minister Pralhad Joshi’s sensible call on 16 March 2020 to cut back on thermal coal imports at a time of rising domestic production and weak demand.

Weaning India off thermal coal imports could save the country upwards of US$2bn annually.

PRIME MINISTER NARENDRA MODI’S RENEWED FOCUS ON LOCAL JOBS AND INVESTMENT, reflecting the “Make in India” strategy, combines with clear energy security needs: India must sustainably reduce its excessive reliance on fossil fuel imports in favour of increasing its reliance on domestic coal, hydro, wind and solar resources.

Weaning India off thermal coal imports could save the country upwards of US$2bn annually – a taste of the opportunities the technology-led energy transition is bringing the country. Further, a progressive increase in the electrification of transportation could save India ten to fifty times this amount every year by next decade if it is done comprehensively.

Coal-fired power as a balance to variable renewable energy

As India accelerates deployment of low cost but variable renewable energy generation, grid balancing and stability will come to the fore as key constraining factors, particularly into evening peaks as daily solar generation tails off just as the workforce returns home.

IT IS IMPORTANT FOR INDIA TO INVEST ‘AHEAD OF THE NEED’ in flexible, on-demand power generation, with the answer likely to rest in a combination of greater national grid connectivity; hydro, including pumped hydro storage; batteries; peaking gas; and demand response management, where consumers are offered an incentive to cut use during extreme circumstances.

India needs to make its coal power fleet more flexible to help balance the rising share of intermittent renewable energy.

Given India’s significant historic investment in now 205 GW of coal-fired power capacity, the much lower than planned utilisation rate (averaging just 56%) of these plants creates both a financial problem, but also an opportunity for the country. India needs to make its coal power fleet more flexible to help balance the rising share of intermittent renewable energy.

Gujarat recently completed a trial whereby the state operated its coal-fired power plants at average capacity utilisation rates of 40% so as to provide peaking power to balance ever higher variable renewable energy. There are however economic implications of adopting such a model nationally – using coal plants running at half the design rate – as it makes energy materially more expensive per unit of electricity produced.

Likewise, SECI this month launched a 5GW tender for a hybrid wind-solar-hydro-thermal generation package supported by a 25-year power purchase agreement. Renewables must constitute at least 51% of total generation (ensuring low cost and low emissions), but the delivery must be firm for 80% of the time each year, meaning this tender provides a financial incentive for much needed balancing capacity.

When combined with higher ramp rates than currently declared by power stations, investigated in CEA and POSOCO reports in 2019, the ability of some plants to operate at lower capacities emphasises the potential for coal generation to make a larger contribution to peaking power, and the importance of developing a pricing structure to incentivise the delivery of more valuable peaking power.

Conclusion

TECHNOLOGY IS DISRUPTING GLOBAL ENERGY MARKETS. For many countries this is problematic.

For India, this brings a suite of opportunities including reduced water scarcity pressures; reduced reliance on inflationary fossil fuel imports; improved energy security; reduced air pollution; and a lower cost total energy system. Decarbonisation is an added bonus to showcase India as a global leader, doing its unfair share of the Paris Agreement workload.

2019/20 has delivered a landmark 25TWh reduction in coal-fired power generation in India, highlighting the speed of the energy transition. The slowdown in electricity generation growth to just 10-12TWh, up 0.8% year-on-year in 2019/20 has highlighted the risks, and the opportunities.

India’s increasing domestic coal production likewise provides the opportunity for India to permanently reduce reliance on expensive coal imports. And the coal industry can potentially also play a key positive balancing role in facilitating India’s increased peaking power needs whilst reducing the overall cost.

Charles Worringham is an IEEFA Guest Contributor and Tim Buckley, Director Energy Finance Studies, IEEFA Asia Pacific.

Related links:

Policy certainty and stability sought to increase renewable energy development and investment

India urged to boost competition, modernise and upgrade the grid

Reducing pressure on banking and thermal coal sectors

India’s stranded asset risk in thermal power sector underestimated

Global coal power set for record fall in 2019

India’s electricity sector transformation has made progress in 2019/20

Related Content