IEEFA Update: How Will Westmoreland Coal’s Deepening Spiral End?

We’ve just published a research brief of interest to any person, community, business, or investor with ties to Westmoreland Coal Co.

The brief—“Westmoreland Coal Is in Trouble”—lays out how the company, which produces coal for electricity generation, is hobbled by debt, is losing customers, has suffered a catastrophic drop in stock price, and appears to be on the verge of bankruptcy.

The Colorado-based company’s holdings are far-flung, with major assets across a broad geographic area that includes Montana, New Mexico, Ohio, Wyoming, New Mexico, and Canada.

Our research brief notes that Westmoreland’s market capitalization has dwindled to about $10 million and that the company is buried in some $1.6 billion in debt.

Some additional takeaways, explained more fully in the brief:

- Risk is growing for investors who own a piece of the company, whose credit rating has tanked and whose debt is now considered junk.

- Electricity ratepayers and taxpayers in Montana and Wyoming are at potential financial risk because of their exposure to Westmoreland.

- An Ohio subsidiary of Westmoreland that is sinking under the weight of unmanageable debt is in negotiations that may result in lenders taking over assets.

- Westmoreland mines in New Mexico, North Dakota, and Texas have lost core customers.

- Four Westmoreland mines in Alberta and two in Saskatchewan at are risk of closure as a result of energy policy changes in Canada.

The company is in dire straits in no small part because of questionable decisions by management, but also because the U.S. coal industry is in broad decline and facing serious headwinds.

Utilities across the U.S. continue to retire coal-fired units at a rapid pace, cutting heavily into demand for coal. The advanced age of many plants, alongside relatively high maintenance and operating costs, are making them unviable in competitive electric markets, where cheap natural gas and the falling cost of wind and solar generation are relentlessly stealing market share.

The coal mining industry as a whole has not adjusted to this new reality, leading to an intensely competitive, oversupplied thermal coal market with low- or nonexistent profit margins for many producers.

Notably, companies that appear to be doing better than some include those that have recently gone through bankruptcy.

Our research brief summary:

Our research brief summary:

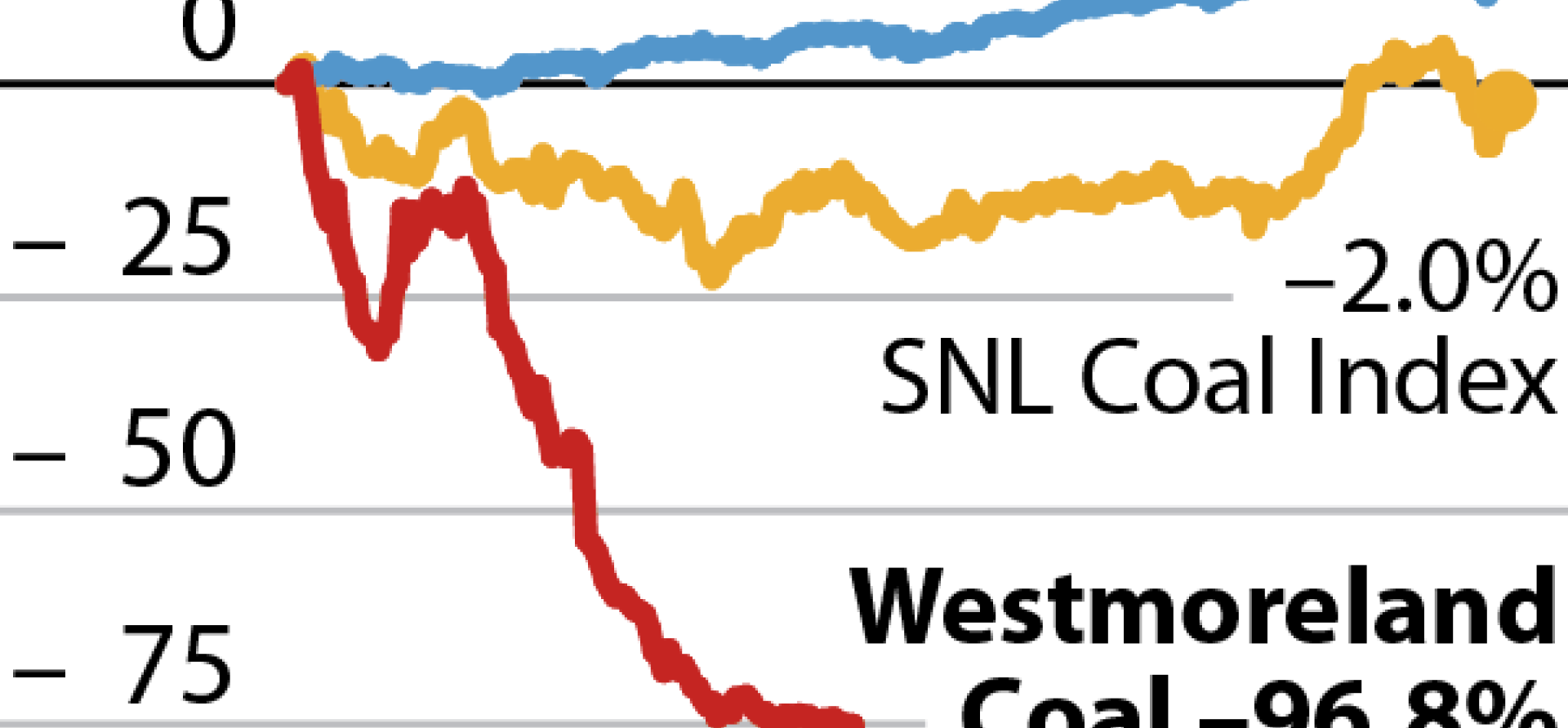

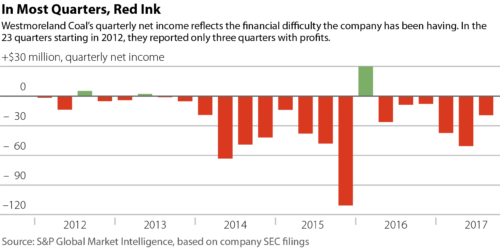

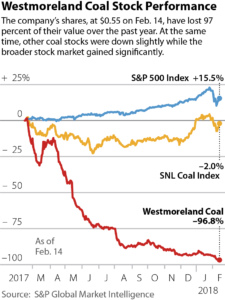

“The company’s current stock price is currently trading around 50 cents a share, reflecting an almost total loss in value over the past year. Westmoreland is well over a billion dollars in debt and faces debt-service costs that will only increase as interest rates rise. Its debt is in junk-bond territory and deteriorating. It continues to report losses, quarter after quarter. Its negotiations with lenders has led it to try to give away assets to avoid default. Intense competition, low prices, and overall falling demand for coal are also buffeting the company.”

“All of these suggest that Westmoreland is in a precarious financial position that stands to adversely affect its business and potentially expose investors, lenders—and, in some instances, ratepayers and taxpayers—to fallout should the company go bankrupt.”

We note also that while Westmoreland has a few customers in Asia, it depends almost entirely on thermal-coal sales in the U.S. and Canada, where an electricity-generation shift toward other sources—natural gas, wind, and solar—is gaining momentum.

Westmoreland Coal is not well-positioned for survival in in its current incarnation as this market shift continues.

Full research brief: “Westmoreland Coal Is in Trouble”

Seth Feaster is an IEEFA energy data analyst.

RELATED ITEMS:

IEEFA New Mexico: Ratepayer Risk Seen in Utility’s Entanglements With Westmoreland Coal

IEEFA Update: A Case That Suggests Regulators Are Tiring of Campaigns to Bail Out Failing Power Plants

IEEFA Report: U.S. Coal Market Erosion Continues

Related Content