ESG scrutiny reveals cracks in credit rating methods

Just as businesses and risk managers are expected to think beyond the short term, credit assessment practices must evolve to ensure that the rating system, too, promotes sustainability.

14 March (IEEFA Asia): The environmental, social and governance (ESG) conduct of a company has no direct bearing on its credit rating actions, which are focused on the short term, a research study of more than 700 corporates has shown.

The study outcome reveals how credit rating agencies are still evaluating companies the traditional way despite making an effort to produce detailed ESG scores and having come a long way in terms of their credit outlook on hydrocarbon related sectors, says Hazel Ilango, an Energy Finance Analyst at the Institute for Energy Economics and Financial Analysis (IEEFA).

The rating framework may have been ESG-enhanced, she says, but it remains a “repackaged concept” of long-established credit assessment principles.

“A company can have a weak ESG credit score, be carbon intensive or lack a clear carbon transition pathway, and yet be assigned a high investment-grade rating due to its high ability to repay its debt in the next three to five years,” Ilango writes in her new report. Such companies may not suit investors who take the long-term view on investment, so even those that do not focus on ESG matters can be exposed to abrupt rating downgrades stemming from climate change.

Credit rating agencies have the potential to play an important role in driving sustainable debt financing, particularly in view of the need to carry out 70% of clean energy investment over the next decade to achieve net-zero emissions by 2050, according to an International Energy Agency estimate.

As such, one critical step is to directly integrate ESG factors in their rating methodology, Ilango says.

She acknowledges that the three agencies examined in the report — S&P Global Ratings, Moody’s Investors and Fitch Ratings — are increasingly viewing risk through an ESG lens to assess an entity’s creditworthiness, as articulated in their development of ESG credit scores. However, that is not enough.

“Based on IEEFA’s analysis of 721 companies as of September 2022, we find that there is no direct relationship between their ESG credit scores and credit ratings,” Ilango says. “While the three agencies all provide detailed ESG credit scores to bond investors, it is difficult to establish a straightforward link between their ESG scores and credit ratings.

“Such scores merely represent a detailed and transparent ESG diagnosis on how these factors could impact the final credit outcome.”

She believes that if rating agencies had overhauled their conventional assessments by integrating ESG factors as a central component in addition to business, financial and supplementary risks, it would likely have prompted disruptive changes to companies’ ratings across sectors and regions.

As things stand, bond investors cannot adequately assess an issuer’s long-term credit risk based on the credit rating alone. They also have to refer to the ESG credit scores to somehow gauge its ESG exposure.

Case study: China Huaneng versus Denmark’s Orsted

Ilango illustrates her analysis outcome by comparing state-owned enterprise China Huaneng Group Co with offshore wind power company Orsted of Denmark.

Orsted has only a “BBB” credit rating from S&P and Fitch. Huaneng is reliant on fossil fuel and vulnerable to high stranded asset risks, but maintains a “A” credit rating range across all three agencies. This underscores the research finding that credit ratings do not change if a business model moves toward a low-carbon transition economy, until the company’s creditworthiness is affected.

“Consequently, bond investors will continue to fund carbon-intensive companies due to their high investment-grade ratings, and decarbonization challenges will persist,” says Ilango.

IEEFA considers that the current methodology does not encourage debt financing of sustainable initiatives, so bondholders may keep supporting businesses that have fundamentally poor green standards. If the credit framework remains “business as usual,” real-world problems such as climate change and social inequality will continue.

Rating challenges and trends

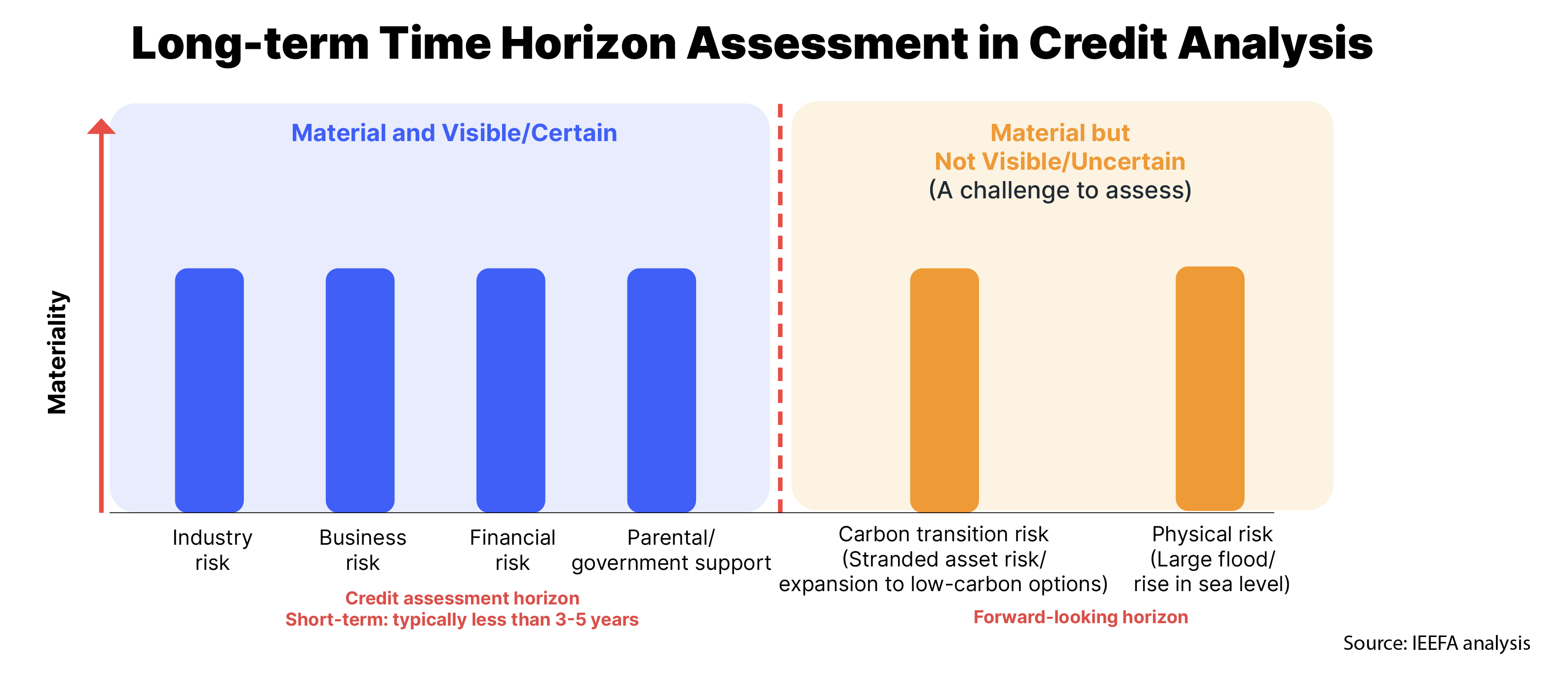

One of the challenges is a mismatch between ESG factors and the credit ratings time horizon. When evaluating ESG risks as part of a credit assessment, credit rating agencies consider four key factors: visibility, probability, severity and timing.

If ESG risks or factors are sufficiently certain, quantifiable and severe enough to affect creditworthiness, they are factored into rating considerations.

A carbon emissions tax, for example, would be a climate transition risk to include in financial forecasts, but the potential future cost of an extreme weather event would be excluded due to the uncertainty of its timing and impact.

“It could be too late to consider these risks, particularly climate change-related threats, only when they become visible and certain — while we sit and wait on a snowballing crisis,” says Ilango.

“Climate change risks expose bond investors not only to the physical climate, but also to transition risk with the shift toward a low-carbon economy. Therefore, corporates that are susceptible to such risks may have a higher potential for default.”

Ilango cites the case of California’s Pacific Gas and Electric Company (PG&E), which faced billions of U.S. dollars in liabilities related to wildfires, a physical risk, between 2015 and 2018. Subsequently, S&P and Moody’s downgraded PG&E’s rating due to its challenging environment, and the company finally filed for bankruptcy on 29 January 2019.

“This highlights that what is deemed uncertain risk today could result in a multi-notch downgrade and, eventually, bankruptcy, which can severely impact bondholders,” says Ilango. “It also exemplifies how the current credit rating model is short-sighted and not intuitive enough to provide an early warning signal.”

An issuer which faces heightened ESG risks in the long term, particularly climate-related risk, may experience an abrupt rating downgrade sooner than expected, raising the possibility of significant bond sell-offs.

Proposed Models for Integrating ESG Factors in Ratings

These challenges do not have a quick fix, given the complexity around credit evaluation. However, environmental and social issues are gaining traction and deserve more attention. Ilango believes that the conventional rating methodology requires an overhaul to include long-term risk and produce a tangible outcome on credit ratings that account for ESG factors.

“Just as businesses and risk managers are expected to think beyond the short term, so should credit rating agencies. However, this challenges the conventional perception of a credit assessment,” she says.

Ilango suggests carrying out standalone ESG risk assessment through qualitative scoring of environmental and social impacts on long-term creditworthiness, just as agencies are already doing in examining governance.

Rating agencies can also introduce double rating measures. For example, they can give a company a “BBB” rating based on the conventional credit assessment, then issue an upgrade or an ESG-adjusted rating to an “A” to recognize its substantial decarbonization strategy and robust social and governance attributes.

In addition, rating agencies could take a more granular approach to ESG considerations by including and publishing scenario analysis to quantify long-term trends and risk trajectories.

“In our report, we’ve explored possible models for how to better integrate ESG in credit rating assessments,” Ilango says. “The aim is to study the possibility of creditworthiness and sustainability coexisting in a credit rating assessment.”

Read the report Can credit rating assessments and sustainability coexist? and the factsheet

Report contact:

Hazel Ilango ([email protected])

Media contact:

Alex Yu ([email protected]) Ph: +852 9614 1051

About the author:

Hazel Ilango is an energy finance analyst at IEEFA covering debt markets. Her past work has actively focused on data analytics and credit analysis while developing credit-related models for fixed-income instruments. She holds a BSc Mathematics degree from the University of Wisconsin–Eau Claire.

About IEEFA:

The Institute for Energy Economics and Financial Analysis (IEEFA) examines issues related to energy markets, trends and policies. The Institute’s mission is to accelerate the transition to a diverse, sustainable and profitable energy economy. (www.ieefa.org)