Policy blind spots slow mining decarbonisation

Key Findings

Less than a third of Australian mining’s 50–70MTPA of Scope 1 emissions are covered by any policy mechanism, with open-cut mine diesel emissions in a regulatory void.

The NSW EPA’s latest Greenhouse Gas Mitigation Guide for Coal Mines has no abatement requirements for diesel emissions, and its only requirements, for underground mines, are likely to be ineffective.

Safeguard Mechanism compliance costs for open-cut mines are insignificant compared with the Diesel Fuel Tax Credit, giving miners a negative policy signal to decarbonise.

Committed federal and state grant funding for diesel decarbonisation sits idle, and government electrification pathways ignore coalmine electrification demand.

Note: This analysis is for information and educational purposes only, and is not intended to be read as investment advice. Please click here to read our full disclaimer.

A recent investigative series attributed BHP’s lack of progress on diesel decarbonisation to revised ambitions by the mining giant, but governments share some responsibility. Policy settings not only carry negligible consequences for inaction on diesel emissions, but miners are effectively rewarded for taking no action.

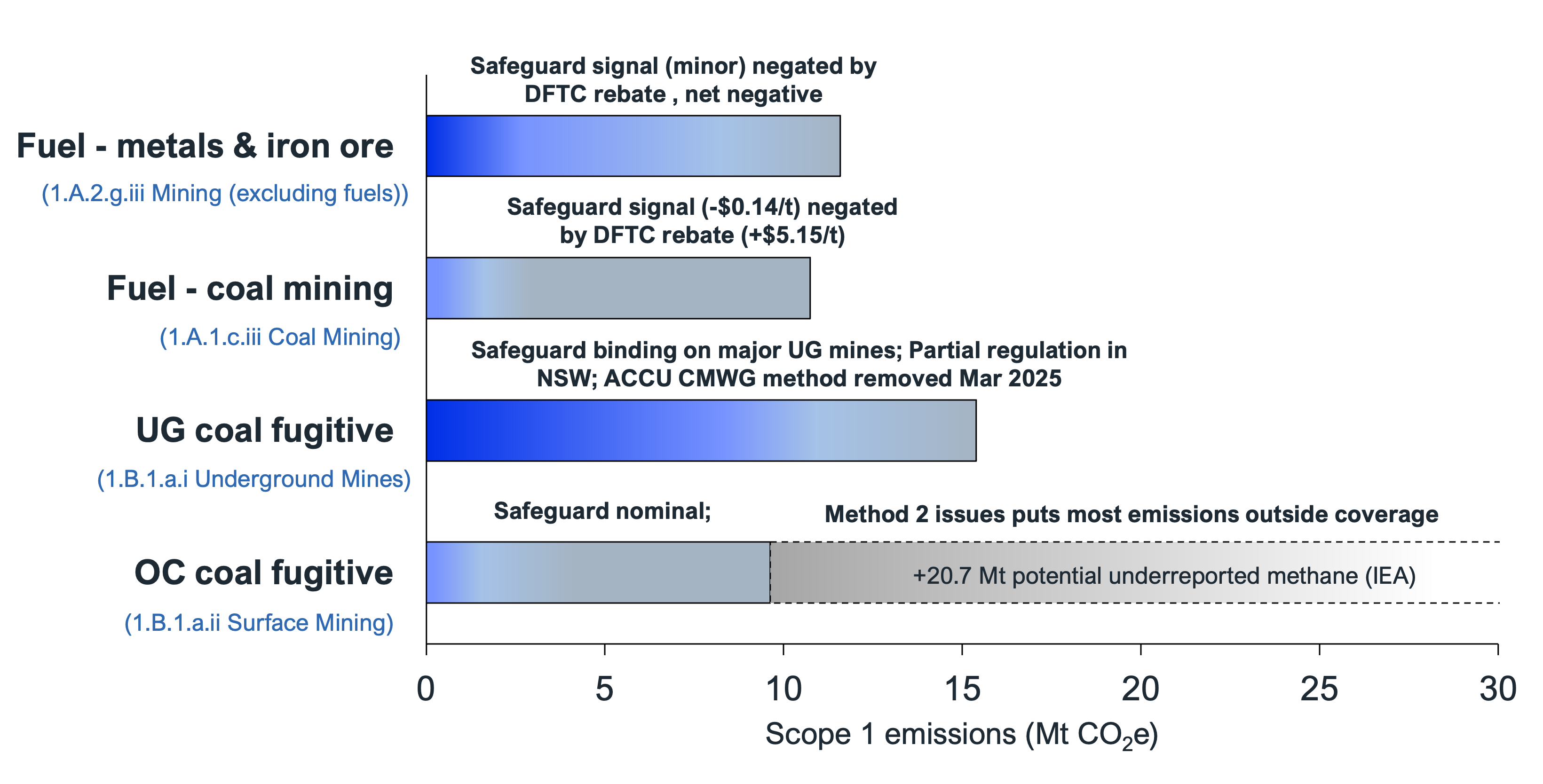

IEEFA’s January review found a disconnect between federal emissions projections and reality. Figure 1 shows 47.3 million tonnes of carbon dioxide (MtCO2e) of reported mining Scope 1 (direct) emissions in FY2023–24 — up to 68Mt allowing for potential underreporting, including 20.7MtCO2e based on International Energy Agency/Ember methane gap data. Policy mechanisms are strongest for underground coalmining, and partial for metals and iron ore diesel decarbonisation; about 20Mt of emissions is covered, and that coverage is uneven. Most open-cut mine diesel emissions abatement is compromised by counterproductive policy incentives.

Figure 1: Policy coverage for mining emissions (Scope 1, MTPA)

Source: United Nations Paris Agreement inventory for 2024. Note: Blue scale represents strength of policy initiatives. OC coal grey shaded area represents uncertainty based on the IEA’s estimated emissions reporting (1.657Mt methane or 46.4MtCO2e, to the UNFCCC reported 0.918Mt methane or 25.7MtCO2e – a gap of 0.74Mt methane for Australian coalmining (0.74Mt CH4 x 28GWP* = 20.7MTCO2e). *Global warming potential.

There is no national or resources sector target for diesel decarbonisation. Existing policies, such as the Safeguard Mechanism, bundle methane and diesel together, and drive change on neither. The NSW Net Zero Commission (NZC)’s Spotlight report found the Safeguard Mechanism, “does not provide sufficient incentive to ensure the on-site abatement that is required”. To offset their emissions, miners can earn and sell Australian Carbon Credit Units (ACCUs). However, a combination of low ACCU prices and unbounded use of offsets, limits its effectiveness.

At last month’s NSW Joint Standing Committee on Net Zero Future hearing, the NSW NZC confirmed that the resources sector was one of only two NSW sectors whose emissions were projected to increase — adding to the already significant 2030 target gap. Net Zero commissioner Katerina Kimmorley told the hearing that, “coal sector emissions in 2030 need to be lower than recently reported, not higher, and that’s not what we see in the projections”. She added, “coalmine extensions and expansions will increase the industry’s overall emissions, adding to the projected gap”.

The commissioner noted the Environment Protection Authority (EPA)’s Greenhouse Gas Mitigation Guide for Coal Mines (2026), “does not include any abatement requirements for open-cut coal mines or diesel emissions”.

Seven policy gaps failing the decarbonisation task

1. Sector emissions projections are unreliable

Official data shows mining sector emissions declining slightly or broadly flat. Significant reductions in fugitive emissions are being driven by the temporary closure of gassy mines. Meanwhile, diesel emissions in operating mines continue to rise with increasing diesel intensity in coalmining and stalled mitigation of fugitive emissions in active mines (Figure 2).

Figure 2: Mining emissions trend (Scope 1)

Source: United Nations Paris Agreement inventory for 2024.

There is also significant suspected underreporting of fugitive methane emissions from coal mining. In NSW, the Method 2 sampling review for open-cut coal methane estimation — recommended as a “matter of urgency” by the Climate Change Authority in 2023 — remains a work in progress some 30 months later.

The NSW Net Zero Commissioner noted, “fugitive methane emissions from coalmining, particularly open-cut coalmining, may be significantly under-reported and that the new government position fails to recognise this issue beyond committing generally to continuous improvement of emissions reporting”.

On a positive note, a pilot study on atmospheric greenhouse gas (GHG) measurement — including from mines — has been launched in the NSW Hunter region.

2. The Safeguard Mechanism is not working for coalmine diesel use

The Safeguard is meant to set declining baseline emissions intensities. For open-cut coal mines, IEEFA has reported it is not working as designed with major open-cut coalminers. They face an increased baseline emissions intensity of 1.3%, on average, in FY2024–25, despite the mechanism nominally requiring 4.9% in annual reductions.

Across the major listed open-cut coalminers, aggregate compliance cost was approximately AU$24 million — or AU14¢/t of coal produced. For reference, the coal price sits at US$249/t for coking coal and US$149/t for thermal coal. The diesel consumed by heavy vehicles in open-cut mines effectively faces no marginal abatement signal. Facilities covered by the Safeguard have become heavily reliant on offsets to meet emissions reduction obligations — a use beyond the original, market-based design.

3. Fuel tax credits actively discourage diesel decarbonisation

For an off-road mining ultra-class haul truck, the Diesel Fuel Tax Credit (DFTC) is large enough to flip the decarbonisation business case. At 2025 levels around AU$1.70 per litre, the rebate offset roughly 30% of fuel input costs, equivalent to diesel’s contribution to the truck’s total cost of ownership (TCO). At AU$2.70/L, the rebate share falls but diesel rises to as much as 45% of the TCO.

In coal production terms, the rebate was worth AU$5.15/t at AU$1.70/L, and each additional dollar per litre of diesel price adds about AU$10 per tonne to production costs for open-cut coalmines. In comparison, the Safeguard compliance cost is just AU14¢.

The DFTC subsidises the deferral of a technology BHP's own strategy assumes will arrive.

4. The ACCU scheme has lost its coalmine crediting tools

The ACCU scheme produces verifiable carbon credits which Safeguard facilities can buy to offset their emissions. The marginal income from ACCUs can be the difference between a viable abatement project — in miners’ capital investment priorities — and a shelved one.

The ACCU Coal Mine Waste Gas (CMWG) method credited the use of vented gas for onsite electricity generation until it expired in March 2025. The federal government announced in April the CMWG method would not return, citing “declining marginal value”.

The data does not support that reasoning: 11 new projects were registered in FY2024–25 — the highest uptake in the method’s history, more than double the next highest year. The federal Emissions Reduction Assurance Committee (ERAC)’s review confirmed the integrity of the CMWG method. It was originally restricted to underground mines, on the erroneous basis that open-cut abatement would cause more emissions than it saved. It should be remade and broadened to include open-cut mines. Considering the potential for methane underreporting, this policy gap is potentially the largest.

5. State mine regulation absent on diesel and partial on emissions

Coalmine approvals pass through state-based and sometimes federal Environment Protection and Biodiversity Conservation (EPBC) processes. GHG controls are considered only at state level. In March, the NSW EPA introduced the Greenhouse Gas Mitigation Guide for NSW Coal Mines for licensing conditions. The guide phases in from next year (waste-gas flaring) to 2032 and 2034 for ventilation air methane (VAM) implementation, subject to certain criteria.

It is highly likely the guide will be ineffective in driving any new emissions reductions at the underground mines it is designed to cover. Many mines have closed before implementation. Operating mines and those approved for extension are illustrated in Figure 3.

Figure 3: NSW EPA policy guidelines exclude most mines

Source: 2024-25 Safeguard data, Coal mines in NSW Key Statistics, IEEFA. Note: Excludes undeveloped Wallarah 2 Coal Project and the Maxwell underground mine, assumes 75% methane content in annual Scope 1 emissions estimate of 0.37MtCO2e, per the project GHG assessment.

Few mines remain in the policy window:

- Airly mine is scheduled to close in 2038. With less than 100kt of annual emissions, it falls below VAM abatement threshold.

- Appin, which is already capturing methane and undertaking a VAM pilot project.

- Ashton, scheduled to close shortly after the VAM implementation is due in 2034.

- Mandalong produces domestic coal. While not specifically excluded, an exemption could be granted because any cost increases will be reflected in NSW electricity bills.

- Maxwell mine recently commenced, and could be captured by the policy, noting the project gas model indicates “low inherent methane levels in the ventilation air, and assumes that no abatement occurs due to practical constraints”.

The remainder are exempt. The regulations also exempt open-cut mines and diesel emissions.

Rather than be drawn on relative readiness of each mine to decarbonise, the NZC recommends an “outcomes-based approach” to the EPA guidelines that specifies the amount of onsite abatement required by a set time, to minimise the need for exemptions.

Queensland has no equivalent regulatory instrument, and its resources sector emissions reduction plan has been postponed from 2025 until up to 2030.

The NSW government’s Coal Industry 2026–50 statement, released in March, indicated a preference for approving extensions of open-cut mine lives. NSW Resources told the NZC hearing that, “Extensions of existing mines will continue to be considered, subject to rigorous controls to reduce emissions”. On the current settings, it is difficult to see what those controls are. It is also not sufficient to accept emissions reduction will be achieved from the closure of coalmines alone, even thermal coalmines. As the NZC was told, “[export] coal from New South Wales will be required well into the 2040s”.

6. Idle decarbonisation funding not directed to diesel

The first five gaps describe policy shortcomings. This gap highlights the disparity between funded decarbonisation initiatives and actual funds allocated. More than AU$1 billion in government funding for coalmine diesel decarbonisation remains largely unspent or has been directed to fugitive methane abatement.

Sources: LEIP, STS, HEI, ARENA and IEEFA.

All funding directed to coalmining went to fugitive methane abatement projects. Apart from AU$9M in Australian Renewable Energy Agency (ARENA) funding for diesel decarbonisation, the remaining funds were not directed to this end, despite being eligible. Targeted use of these idle funds might consider the diesel electrification needs of the multiple open-cut coal mines that operate hundreds of large mobile mining equipment and lie along distinct mining corridors.

7. Planning and approvals blind spots

Government planning does not prioritise coalmine diesel decarbonisation in electricity roadmaps. Grid expansion under way across NSW and Queensland focuses on two demand categories: decarbonisation of existing industrial processing — such as Tomago aluminium in the Hunter, and Gladstone alumina, ammonia and refining in Central Queensland. The Australian Energy Market Operator’s 2025 decadal electricity grid demand forecast made no mention of coalmining. Its 2026 draft Integrated System Plan explicitly reclassified the Central Queensland to Southern Queensland Expansion project from “actionable” to “future”, pushing any grid capacity build into the 2030s. Coalmining haul-fleet electrification appears in none of the demand cases.

NSW Resources confirmed at the NZC hearing that when assessing coalmine extensions, emissions were not considered because, “we don’t have a remit that covers emissions”. The NSW Coal Industry 2026–50 Statement projects coal demand running well into the 2040s, and signals approval preference for open-cut mine extensions on that basis. There is no decarbonisation pathway for the operating fleet those extensions will require. States’ tendency to approve coalmine extensions on a rolling basis means they cannot rely on mine closures as a decarbonisation tool.

Policy gaps have made it difficult for decision makers to accurately estimate whether real emissions reductions are being achieved. The lack of a sector decarbonisation targets compounds the problem. Meanwhile, international pressure is rising. The United Nations supports the International Court of Justice’s Advisory Opinion, that the failure of a State to “protect the climate system from GHG emissions — including through fossil fuel production, […] or the provision of fossil fuel subsidies — may constitute an internationally wrongful act”.

Related Content