Minimal role for carbon capture, utilization, and storage (CCUS) in IEA's World Energy Outlook 2025

Key Findings

According to the International Energy Agency’s (IEA) World Energy Outlook (WEO) 2025, carbon capture, utilization, and storage (CCUS) is projected to contribute less than 5% to offsetting emissions by 2050.

The IEA’s minimal role for CCUS in the Net Zero Emissions (NZE) by 2050 Scenario reflects a multi-year downgrading of the technology, with renewables, electrification, fuel switching, and energy efficiency projected to contribute over 82% of the emissions reductions needed to achieve net zero.

CCUS faces high investment and operating costs, bespoke project designs, and inflation-sensitive components and materials, which make it economically uncompetitive compared to renewable energy and storage technologies.

CCUS projects have been delayed, canceled, or failed to materialize, often due to unfavorable economics, despite claims of the technology’s “vital” role in decarbonization. The IEA’s WEO 2025 data indicates that, even in the NZE Scenario, CCUS is not essential to achieving decarbonization.

On 12 November 2025, the International Energy Agency (IEA) released its annual World Energy Outlook (WEO). Among the three energy scenarios presented, the IEA’s Net Zero Emissions by 2050 Scenario (NZE Scenario) details the trajectory required to eliminate net carbon dioxide (CO2) emissions by 2050.

The IEA assesses the technologies, policies, and practices required to deliver the most significant and cost-effective reductions in CO2 emissions. The analysis examines factors such as technical efficacy, operational performance, deployment time, and economic development factors to determine the net-zero formula. The elements of the WEO’s NZE Scenario evolve each year based on the latest updated information on energy technology performance and cost trends.

Various renewable energy technologies, energy efficiency, and electrification lead the way in reducing significant carbon emissions from the global economy. In the 2050 NZE Scenario, solar and wind account for 73% of electricity generation, followed by hydroelectric and nuclear energy, each at around 9%. That accounts for 91% of electricity supplied by just those four sources.

Notably minimized in the report’s discussion of net zero is carbon capture, utilization, and storage (CCUS). At first glance, this downgrading may seem surprising. For years, media coverage, academic literature, and industry reporting on decarbonization have claimed that CCUS will play a critical role in achieving material carbon emissions reductions, particularly in hard-to-abate sectors. Even as recently as 2020, the IEA itself was touting CCUS as a key component of decarbonization.

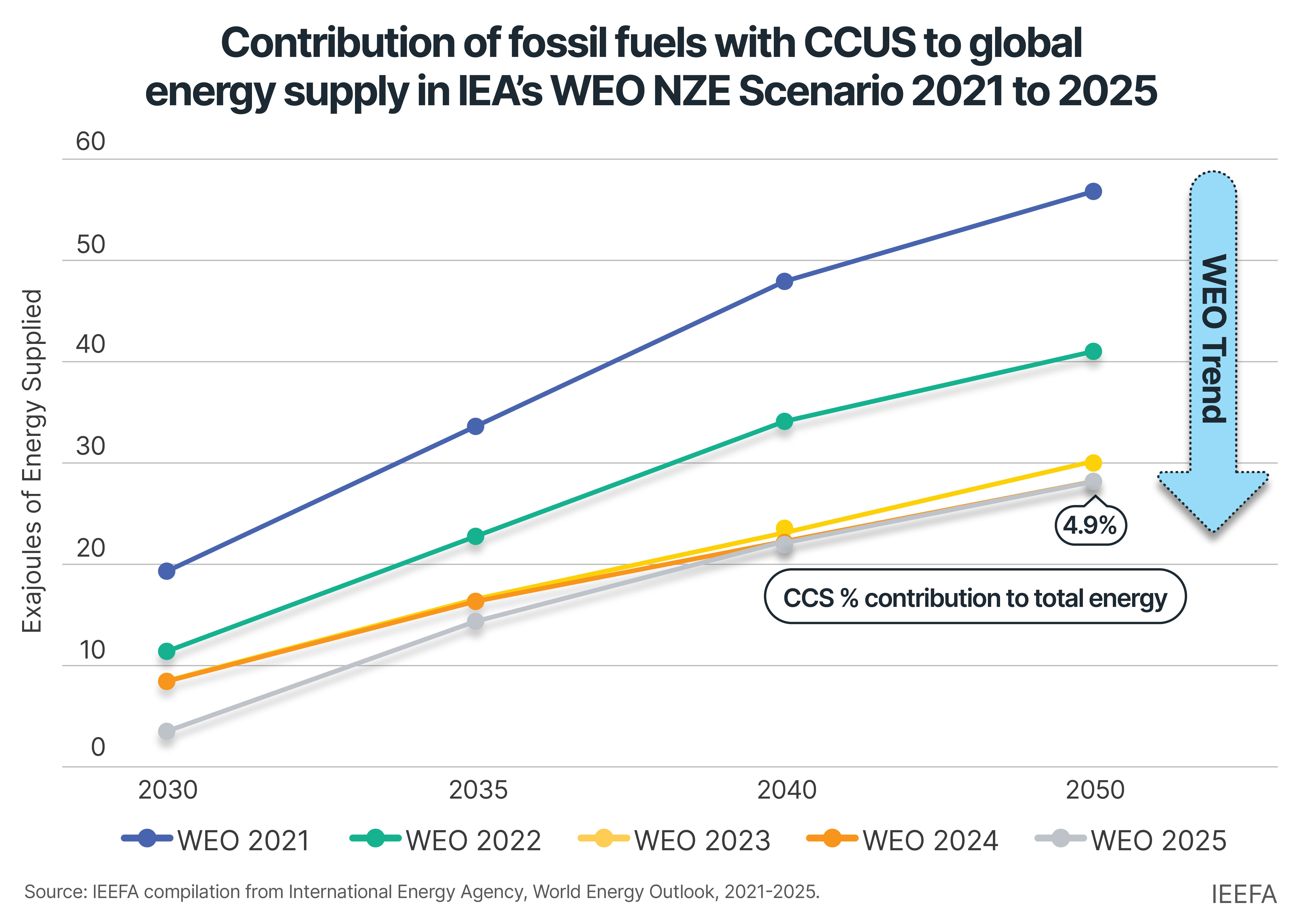

However, based on the WEO 2025, there is no clear conclusion that CCUS is essential to decarbonization. While CCUS is referenced in the text assessing future energy mixes, it is barely visible in the most important metric — the percentage contribution to reduced CO2 emissions. Across all applications, IEA’s figures in the WEO 2025 NZE Scenario show CCUS accounting for a maximum of 4.9% of total emissions reduction, with 1.2% from power generation and 3.7% from industry.

Unfavorable economics for CCUS and falling costs of renewables

The IEA’s implication that CCUS will be of minimal importance reflects the rapid expansion of renewables markets. Globally, total installed renewable energy capacity increased by a record estimated 793 gigawatts (GW) in 2025, led by China. China has demonstrated that renewable energy can be added at scale, at a low cost, and with exceptional speed. According to a China State Council press release from December 2025, Chinese entities installed around 342GW of solar capacity in 2025 alone, an extraordinary rate of 950 megawatts (MW) per day.

While China’s scale may be exceptional, Pakistan has shown that decentralized efforts to install solar panels can significantly increase capacity in a short time. Renewables First found that Pakistan imported a staggering 39GW of solar panels between July 2021 and September 2025, of which only 6.1GW is grid-connected. This indicates that many solar users are either not connecting to or leaving utility service. As a result, in past two fiscal years, grid-based power demand has dropped nearly 12%. This example suggests that the energy transition can advance rapidly, regardless of economic income level. These transformative trajectories, supported by decreasing renewable technology costs, underpin the IEA’s NZE Scenario calculations.

CCUS proponents claim that the technology requires a consistent and robust policy environment, supported by subsidies or tax credits, to offset the high investment and operating costs. These expenses must cover the capture equipment, CO2 transportation, and its final, permanent subsurface storage, and vary widely depending on the source of emissions, distance to disposal, geological complexity, as well as country-specific material, labor, and operating costs. When aggregated across the CO2 disposal chain, these costs are substantial. A 2025 presentation to the European Parliament by Agora Industry and the Öko-Institut estimated that in the European Union (EU), the end-to-end expenses range between EUR105 (USD122) to EUR280 (USD326) per tonne of CO2 (tCO2) disposed.

Without direct subsidies, carbon prices on the EU Emissions Trading System (ETS) need to be maintained within or above the full disposal cost range for industries to feasibly undertake CCUS investments. However, the lower-end EUR105/tCO2 disposal cost is equal to the EU ETS’s all-time peak price, achieved just once in February 2023. In 2025, ETS prices averaged EUR75/tCO2 or USD87. By minimizing the contribution from CCUS in the NZE Scenario, the IEA recognizes that end-to-end CO2 disposal costs are untenable without sustained carbon market pricing or carbon taxes at similar levels.

Declining role of CCUS in decarbonization scenarios

The IEA’s effective omission of CCUS from the WEO 2025 NZE Scenario reflects a recurring, multi-year downgrading of the technology. As shown in the figure below, the contribution of CCUS has steadily declined from WEO 2021 to 2025. In 2021, CCUS accounted for 13% of total carbon removal; by 2025, its share had decreased to below 5%.

Clearly, alternative options for achieving large-scale decarbonization are far cheaper, increasingly cost-competitive, proven to succeed, and rapidly scalable. The IEA notes that the combination of renewables, electrification, fuel switching, and energy efficiency will contribute over 82% of the emissions reductions needed to achieve net zero. By contrast, it states that CCUS-equipped energy production accounted for a mere 0.003% of the global energy supply in 2024. Even under the NZE Scenario, CCUS is projected to contribute no more than 4.9% of the energy decarbonization solution by 2050. These numbers fall far short of what is touted as a “vital” technology.

Bespoke CCUS systems will keep costs high

The costs of CCUS contrast sharply with those of renewable energy and storage technologies. Proponents have been discussing the potential for significant CCUS deployments for decades, arguing that future additions will increase scale and, eventually, reduce costs. However, projects have been delayed, canceled, or failed to materialize, often due to unfavorable economics. CCUS faces two major challenges that keep costs high: the bespoke nature of project design and the high exposure to inflation in equipment and material inputs.

CO2 separation systems are tailored to the specific characteristics of the effluent streams being handled. For example, an ethanol plant’s removal system configuration will be different from that of a coal-fired power plant. Variations in the chemical composition, CO2 concentration, and characteristics of effluents impact the operation and design of CCUS systems.

Additionally, the components that make up a CCUS system are comprised of steel fabrications outfitted with widely available equipment, including pumps, valves, and compressors. However, given the harsh chemical effects specific to CO2 processing, expensive special steel alloys have to be used. Market prices, labor costs, and inflation highly impact these components, materials, and fabrications. CCUS does not benefit from the same level of technological innovation and learning curve savings that have characterized the sharp decline in prices for solar photovoltaic (PV) and battery storage systems.

Conclusion: Marginal role for CCUS now, and in the future

In the WEO 2025, the IEA assigns almost no role for CCUS in electric power generation in its NZE Scenario. CCUS in the 2050 setting accounts for just 1.2% of global energy generation, with about two-thirds attached to coal-fired plants and one-third to natural gas combustion turbine plants. Including hard-to-abate industry effluents, CCUS is expected to contribute less than 5% of offset emissions by 2050. These projections underscore that CCUS is clearly a marginal technology and far from being on equal footing with renewable energy technologies.

Related Content