Lack of ring-fencing provision means Guyana won't realize oil gains before 2030s, if at all

Download Full Report

Key Findings

The lack of a "ring-fencing" provision acts as a subsidy and allows the contractor to charge Guyana for the cost of new wells before they start producing oil.

The contract is front-loaded, which means the contractors receive more than Guyana in the early years of the contract.

Postponed payments may never be recovered. Guyana’s longterm scenario to secure robust profits is risky, and the risk is intensified by this contract provision.

Executive Summary

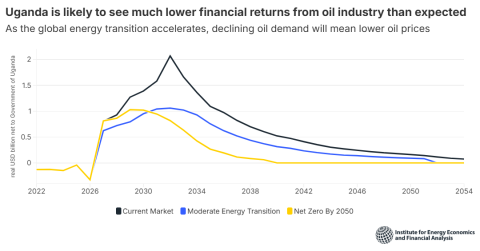

Over the next five years, revenues from Guyana’s newly discovered oil reserves being developed by an ExxonMobil-led development team will not be enough to cover Guyana’s budget deficit, support new spending and build its wealth. Over the longer term, a declining oil and gas sector is highly unlikely to provide Guyana with the robust revenues promised.

This paper focuses on one provision of the contract that allows the contractor to apply any exploration costs it incurs anywhere on the area under contract and to charge 100% of the costs immediately against the active wells. Right now, this means that the contractor can explore for oil at the Tanager and Redtail sites,1,2 for example, and charge its expenses against Guyana’s oil profits from the Liza 1 site. Guyana’s profit drawn from the Liza 1 site is reduced as a result of this loophole. Put another way, Guyana’s profit during the 2021 fiscal year will be reduced to pay for oil and gas that may not be extracted until 2030 or later.

This paper is the first in a series of reports to explore in detail the many ways that the oil share agreement limits the revenue coming to Guyana. Taken alone, the absence of a ring fence front loads the contract with expenses that must be paid before Guyana enjoys an abundant revenue flow. When combined with the other issues, IEEFA will show that the contract is harmful to Guyana’s interests. The contract is front-loaded in favor of ExxonMobil, Hess and CNOOC. Declining oil and gas markets significantly increase the risk that in the long run Guyana’s oil fields will not produce the revenues promised.

Related Content