Japan’s diversified LNG procurement strategy cannot fully shield it from global price spikes

Download Briefing Note

Key Findings

Despite government claims that Japan is insulated from the direct impacts of the Strait of Hormuz closure, the country still faces several risks due to its exposure to global liquefied natural gas (LNG) prices.

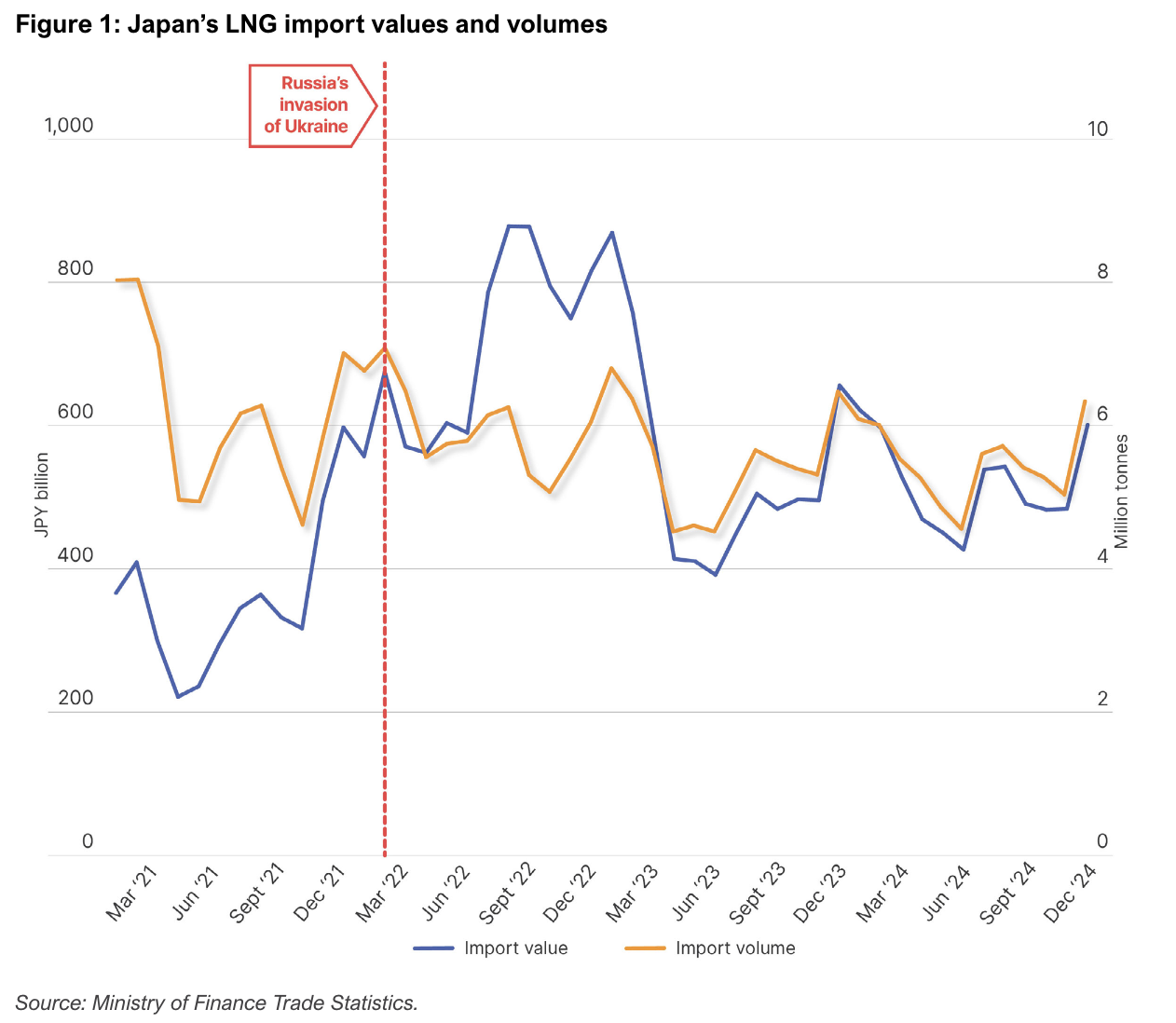

Japan’s total LNG import bill is likely to spike, similar to the increase seen after Russia invaded Ukraine. Between 2021 and 2022, the value of Japan’s LNG imports increased by 65% in United States (US) dollar terms and 98% in Japanese yen terms, even though import volumes declined by 3%.

Higher LNG costs in Japan are expected to pass through to wholesale power markets and retail tariffs. Several utilities plan to raise tariffs, with household electricity bills projected to increase by JPY15,000 (USD95) from April 2026. A prolonged closure of the Strait of Hormuz could further exacerbate inflation and reduce Gross Domestic Product (GDP) by up to 3% in 2026.

Energy security remains a key concern for Japan's policymakers. To better safeguard against energy shocks, Japan should prioritize renewable energy deployment, provide clear policy signals for utilities to make ambitious domestic renewable energy commitments, and introduce incentives to support such investments.

Read the Japanese translation: 日本の多様なLNG調達戦略は、世界的な価格高騰から完全に身を守ることはできない

Following the Middle East conflict and closure of the Strait of Hormuz, the Takaichi government has stated that Japan is insulated from direct impacts because only 6% of Japan’s total liquefied natural gas (LNG) imports pass through the Strait and that it holds three weeks of domestic LNG inventory.

However, this view overlooks several indirect risks if the Strait of Hormuz closure continues. First, Japan would be exposed to greater volatility in LNG spot prices, raising overall import costs. Second, higher fuels costs would translate into electricity price hikes at a time when Japanese households and businesses are already struggling with inflation. Third, government efforts to curtail these price increases would exacerbate Japan’s macroeconomic and fiscal pressures. The risks of fuel price volatility to domestic electricity prices and macroeconomic and fiscal stability were strikingly clear during the global energy crisis triggered by Russia’s invasion of Ukraine. Similar dynamics are beginning to play out as a result of the Iran conflict.

The severity of these risks depends on the duration of the Strait of Hormuz closure. In the medium to long term, Japan should prioritize deployment of domestic energy sources — particularly renewable energy — to hedge against volatile energy markets amid geopolitical uncertainty.

LNG price exposure cannot be mitigated through diversification

LNG accounts for over 30% of Japan’s power generation. A central pillar of the country’s LNG procurement strategy is portfolio diversification. Japanese utilities and trading houses source LNG from geographically diverse suppliers to reduce concentration risk and hedge against disruptions in any single production region. However, diversification does not shield Japan from price volatility resulting from severe global supply shocks.

This vulnerability became evident during the Russia-Ukraine war when Japan’s LNG import costs surged. In April 2021, LNG imports amounted to JPY221.3 billion. As Russia began to limit its pipeline gas exports to Europe, forcing European buyers to import more LNG and driving up global LNG prices, Japan’s monthly LNG import bill rose to nearly JPY600 billion. By August 2022, six months after the invasion, Japan paid over JPY878 billion for LNG imports in a single month — nearly a fourfold increase compared to April 2021 — despite Russian LNG accounting for only 8.7% of Japan’s total imports in 2021. Notably, Japan has not significantly reduced imports of Russian LNG since.

On an annual basis, and in United States (US) dollar terms, the total value of Japan’s LNG imports increased by 65% between 2021 and 2022, even as import volumes declined by 3%. In local currency terms, Japan’s LNG import bill increased by 98% over the same period due to the weakening yen. The country’s annual LNG spending remains above 2021 levels even though imports were 8.8 million tonnes lower in 2025 than four years prior, according to Kpler data. This underscores that diversification of supply sources does little to protect Japan from global LNG price hikes.

LNG spot prices for Japan followed a similar trend. From a low of USD5 per million British thermal units (MMBtu) in February 2021, rising European gas prices pushed Japan’s spot prices up to USD56/MMBtu in October 2021. Following the outbreak of the Russia-Ukraine war, spot prices spiked above USD70/MMBtu in 2022. Although Japan procures almost all of its LNG through long-term contracts, volatility in spot prices means Japanese buyers must bear the cost when they are forced to turn to the spot market.

Rising LNG costs have also prompted questions about whether Japan should deepen LNG procurement from the US to further diversify its supply. In 2025, Japanese companies signed 7.5 million tonnes per annum (MTPA) worth of new LNG contracts with US companies. These contracts are indexed to Henry Hub prices, which are expected to average USD5/MMBtu over the next five years, up from USD2.19/MMBtu in 2024. The US Energy Information Administration also forecasts an increase in average annual Henry Hub prices from USD3.53/MMBtu in 2025 to nearly USD4.40/MMBtu in 2027.

A similar dynamic is already emerging following the conflict in Iran that began in late February 2026. Since the closure of the Strait of Hormuz, the Japan-Korea Marker (JKM) — Asia’s benchmark LNG spot price — has doubled, reflecting tighter supply and intensifying competition between Asia and Europe for available cargoes.

Although Japan’s LNG supply portfolio remains highly diversified and most long-term contracts are indexed to crude oil benchmarks, Japanese buyers remain materially exposed to supply disruptions in the Middle East.

Higher fuel costs lead to higher electricity prices

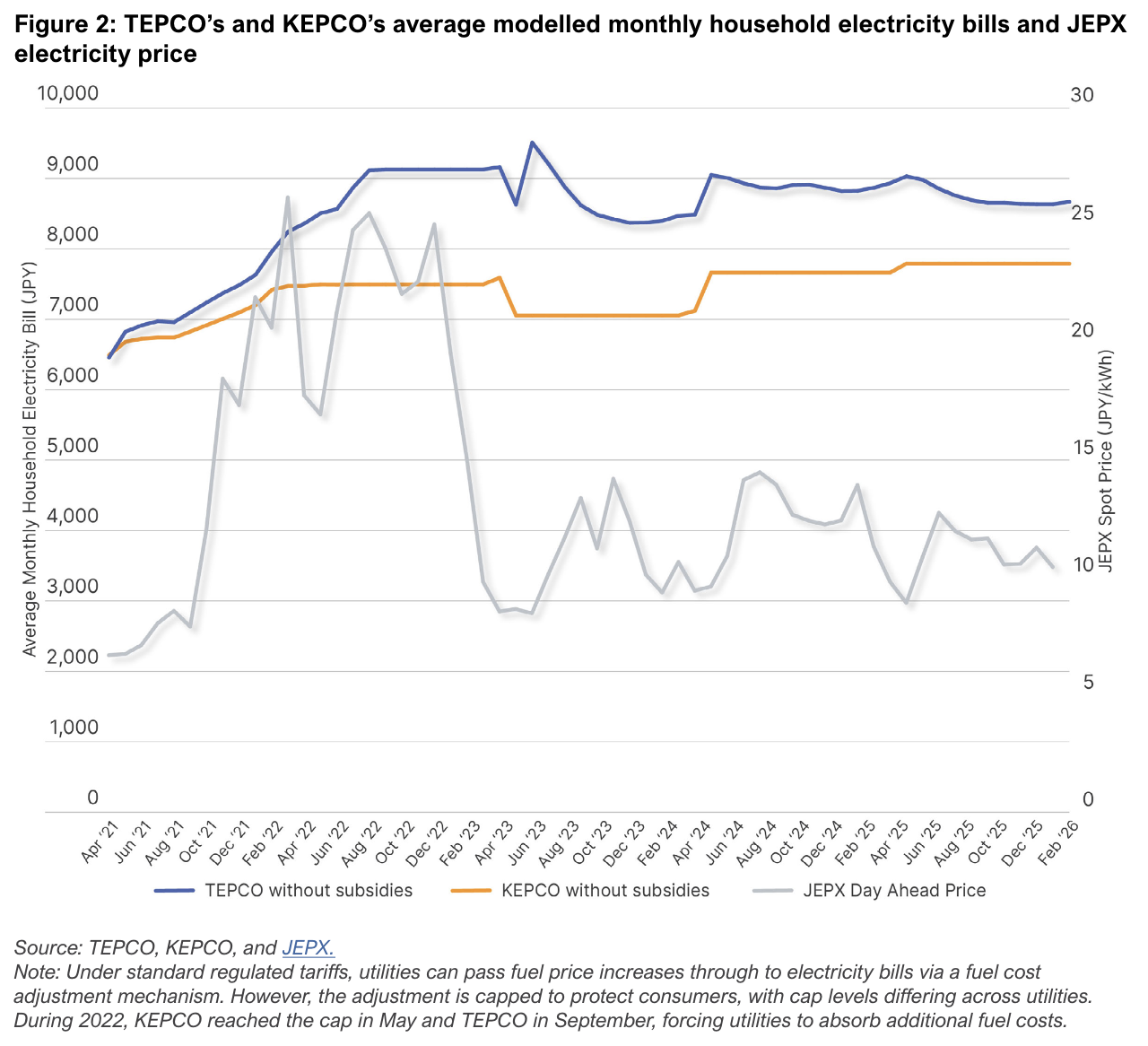

The rise in LNG prices and import costs directly translates to higher domestic electricity prices. Increased LNG costs in 2022 quickly passed through to Japan’s wholesale power markets and retail tariffs. On the Japan Electric Power Exchange (JEPX) wholesale market, the annual average system price rose from JPY13.43 per kilowatt-hour (kWh) in fiscal year (FY) 2021 to JPY20.41/kWh in FY2022, with temporary spikes exceeding JPY65/kWh during periods of extreme fuel price volatility. Retailers reliant on short-term procurement from the wholesale market faced sharp cost increases. By March 2023, 195 electricity retailers — about 27.6% of those registered by April 2021 — had suspended contracts, withdrawn, or exited the market, up from 31 a year earlier, a 6.3-fold increase.

Fuel price shocks also strained incumbent utilities. Nine of Japan’s ten major utilities reported net losses for the April–December 2022 period amid surging LNG procurement costs. Although electricity tariffs include a fuel cost adjustment mechanism, caps under regulated tariffs limited utilities’ ability to fully recover these costs during the price spike.

Household bills also increased sharply during this period. The Consumer Price Index (CPI) shows that household electricity charges rose 20% in 2022, reflecting the pass-through of higher fuel costs in Japan’s fuel-dependent power system. Tokyo Electric Power Company’s (TEPCO) average modelled monthly bill increased from JPY6,546 (USD36) in April 2021 to JPY9,126 (USD50) in late 2022, while Kansai Electric Power Company’s (KEPCO) rose from JPY6,499 (USD36.6) to JPY7,497 (USD41). As fuel costs climbed, seven utilities applied to revise regulated retail tariffs between late 2022 and early 2023, prompting regulators to reassess tariff assumptions based on updated fuel and wholesale market prices.

With fuel costs rising again amid the Iran conflict, TEPCO and Chubu Electric plan to accelerate the pass-through of higher procurement costs to retail tariffs from April 2026. Assuming crude oil prices of USD97 per barrel, annual household electricity costs are projected to increase by JPY15,000 (USD 95).

Price shocks will lead to further inflation and fiscal burden

Rising electricity and fuel costs weigh on consumption and economic growth, amplified by the depreciation of the yen — from JPY109.78/USD in 2021 to JPY131.37 in 2022, JPY140.5 in 2023, and exceeding JPY150 since 2024 — which directly increases the cost of imported energy.

Currency depreciation and rising fuel prices caused Japan’s total fossil fuel import bill to nearly double, from JPY17 trillion in 2021 to JPY33.7 trillion in 2022. This increase pushed the trade deficit to a record level of over JPY20 trillion (USD155 billion). Although prices have since moderated and LNG import volumes have declined, fossil fuel imports remained around JPY22 trillion in 2025, well above pre-2022 levels.

Japan’s CPI, which was negative in 2020 and 2021, rose to 2.5% in 2022 — exceeding the Bank of Japan’s (BOJ) 2% target for the first time in many years. It remained elevated at 3.2% in 2023 and 2025 as higher energy and import costs fed through to consumer prices.

Sustained Middle East tensions and a continued closure of the Strait of Hormuz would likely place additional upward pressure on prices. A USD10 increase in crude oil prices, for example, is estimated to raise inflation by 0.3–0.4 percentage points, underscoring Japan’s continued exposure to energy price shocks. Brent crude oil prices have already risen from USD72 per barrel on 27 February to USD103 on 17 March. Iran has warned that oil prices could reach as high as USD200 per barrel.

Unlike the US and the European Union (EU), which aggressively tightened monetary policy, the BOJ maintained negative rates and yield curve control through the 2022 energy crisis. Though policy normalization has begun — rates reached 0.75% in early 2026 — the BOJ remains cautious amid geopolitical uncertainty, leaving fiscal measures as the primary shock absorber.

Gross Domestic Product (GDP) growth has remained fragile, slowing to 0.9% in 2022 and just 0.1% in 2024. A 10% increase in oil prices could trim GDP by 0.1–0.3 percentage points in the near term. A prolonged shock in which fuel prices double could lead to a 3% GDP contraction in 2026, reversing the modest recovery underway.

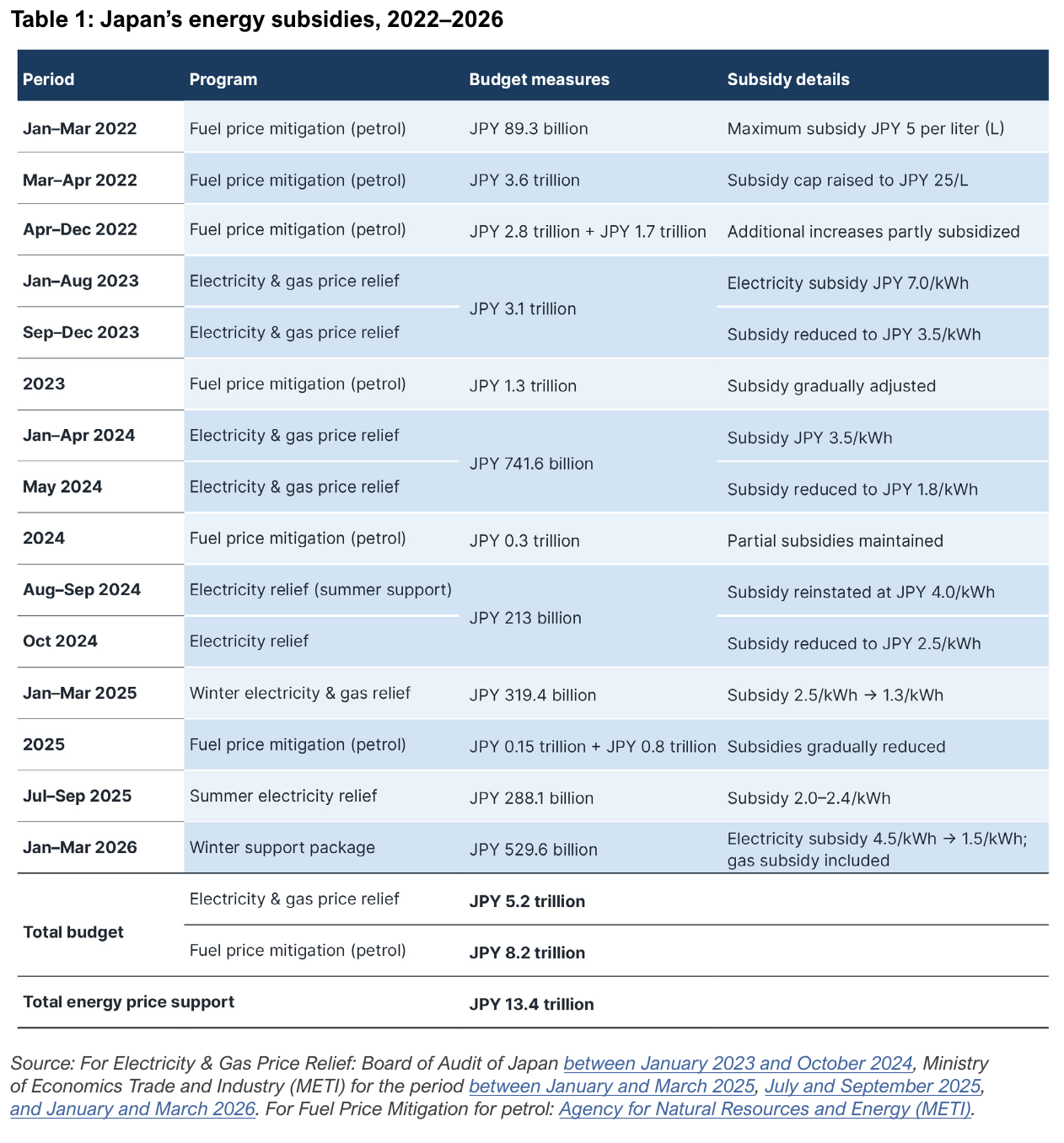

These pressures constrain fiscal policy. Japan’s government debt is projected at 235% of GDP in 2025 — the highest among advanced economies — yet total energy subsidies amounted to JPY13.4 trillion between 2022 and 2025. A further JPY5 trillion (USD32 billion) support package approved immediately before the Iran conflict in February 2026 allocated JPY2.2 trillion to petrol price stabilization. In March 2026, as domestic gasoline prices rose to record levels, the Prime Minister announced subsidies to cap them at JPY170 per liter. While such measures may soften the impact of spiking crude oil prices, they also raise concerns about Japan’s long-term fiscal sustainability.

Domestic renewable energy is key to Japan’s energy security

Japanese policymakers have insisted that Japan is insulated from the most severe impacts from a closure of the Strait of Hormuz, citing the country’s limited physical exposure to LNG imports from the Middle East and the availability of domestic LNG inventories. Such claims may help reassure markets, but they may also understate the extent of the risks Japan faces.

A halt in Qatari LNG cargoes spells a 20% reduction in global LNG supply, reviving competition between Europe and Asia and putting upward pressure on prices. Japan's total LNG import costs are likely to spike as they did in the wake of Russia's invasion of Ukraine in 2022, even as its LNG import volumes declined. Higher LNG import costs are further compounded by the weakening of the Japanese yen. If the Strait of Hormuz remains closed, escalating LNG prices could continue to raise domestic electricity rates for households and businesses well into 2026 and 2027. The government may attempt to ease the burden of high electricity prices through subsidies, but doing so would place additional strain on the country’s already fragile macroeconomic and fiscal position.

These risks underscore the limits of Japan’s LNG diversification strategy, which has not insulated the country from the global price shocks triggered by geopolitical disruptions.

In the medium term, the Japanese government may attempt to strengthen energy security by accelerating nuclear reactor restarts. A recent Bloomberg New Energy Finance analysis suggests that restarting Japan’s largest nuclear reactor, Kashiwazaki-Kariwa Unit 6, could replace 10% of the LNG that was imported from the Persian Gulf in 2025. The restart was expected in January 2025 but has been delayed due to technical malfunctions. These delays illustrate the complex and protracted process of bringing the country’s nuclear fleet back online.

Japan's energy security will be best served by scaling up domestic renewable energy generation. However, several factors currently constrain the rapid deployment of large-scale renewables. One challenge is that Japan's largest utilities, including Tokyo Gas and JERA, have scaled back on their renewable energy commitments. Between 2021 and 2023, major utilities have added less than 2 gigawatts (GW) of renewable capacity, compared with more than 10GW of solar capacity installed during the period when generous feed-in tariffs were in place.

Another, more fundamental, barrier for renewables is the persistent policy ambiguity that shapes these utilities' investment strategies. Notably, Japan's Green Transformation (GX) strategy places LNG, hydrogen, and ammonia co-firing on equal footing with renewables, limiting the incentives for renewable deployment. The 7th Strategic Energy Plan further reinforces this ambiguity by including a scenario in which renewables stagnate — implying greater reliance on LNG imports to close the supply gap.

Energy security is of paramount concern for Japanese policymakers. They can safeguard the country against global energy shocks by prioritizing renewables, providing clearer policy signals for utilities to make ambitious domestic renewable energy commitments, and introducing stronger incentives to support these investments.

Related Content