Four hidden stories in the New Fortress Energy bankruptcy

Key Findings

A March 17 debt restructuring plan announced by New Fortress Energy revealed systemic mismanagement and operational failures.

The plan for New Fortress, which had lost almost $1.3 billion over the previous 12 months, would slash its debt from $5.7 billion to $527 million.

Financial filings show New Fortress made pervasive financial misstatements and steered more than $1 billion in dividends to shareholders and company insiders.

New Fortress also suffered poor operational performance at Mexico’s only liquefied natural gas plant and likely will abandon a second Mexican LNG plant.

A debt restructuring plan announced last week by New Fortress Energy (NFE), the U.S.-based company that owns and operates Mexico’s only operating liquefied natural gas (LNG) plant, sent the company’s stock to all-time lows as markets absorbed a series of devastating revelations about the company’s financial and operational disarray.

An IEEFA review of SEC filings and other public announcements reveals that NFE made pervasive financial misstatements; suffered terrible operational performance at Mexico’s only LNG plant; appears poised to abandon a second, partially-completed Mexican LNG plant; and is unable to repay more than $5 billion owed to its creditors, despite steering more than $1 billion in cash to shareholders and company insiders since 2020.

The debt restructuring was far from unexpected. NFE lost $1.3 billion over the last four quarterly reporting periods and had never in its history generated a single cent of free cash flow. The restructuring plan, which requires approval from a U.S. bankruptcy court and the High Court of Justice in the United Kingdom, would slash NFE’s overall debt burden from $5.7 billion to $527 million, in return for handing over majority ownership in the company to its former creditors.

Although the restructuring avoids a total wipeout for the company’s existing stockholders, investors were dismayed by the torrent of bad news in a series of U.S. Securities and Exchange Commission (SEC) filings and data releases. By Thursday, only two days after the announcement, the company’s stock had fallen to 89 cents per share—down from the highs of more than $60 per share reached in 2022. Today, less than a week later, the company's stock has fallen still further, to 69 cents per share.

Investors had many reasons to punish NFE’s stock. IEEFA has already reported that filing in U.S. bankruptcy court could invalidate a key contract with the government of Puerto Rico. But four additional stories buried in NFE’s financial filings have caught our eye:

Pervasive financial misstatements. An SEC filing released the same day as the restructuring plan admitted that the company had misstated its finances since 2023 and had identified multiple “material weaknesses” in its internal financial controls. Wes Edens, the billionaire CEO of NFE (and co-owner of the Milwaukee Bucks basketball team), has a reputation as a financial wizard. Clearly, however, he ran a slipshod operation at NFE.

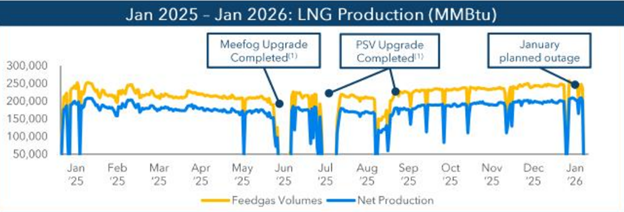

Terrible operational performance of Mexico’s only LNG plant. The same filing describing NFE’s failures in financial reporting also revealed severe engineering and operational challenges at NFE’s largest capital investment, the so-called “Fast LNG” plant off the coast of Mexico near the town of Altamira. Almost 20 percent of the project’s feedgas is consumed by liquefaction and process losses—far higher than typical —and this has required expensive engineering fixes that had failed to improve the project’s performance by January 2026. Even excluding feedgas costs, the project appeared to have the highest operating costs of any LNG plant in the Gulf of Mexico.

Figure 1: Despite repeated upgrades, NFE has consumed almost one-fifth of its feedgas for liquefaction and unspecified “process losses.”

Source: New Fortress Energy

Abandonment of NFE’s second liquefaction plant. NFE has already begun construction of a second LNG plant that it hoped to deploy onshore at Altamira. But as Bloomberg reported in December 2025, the company’s cash challenges had forced it to put construction on hold. What’s more, Mexico’s National Energy Commission had denied NFE’s pipeline permit for the plant, citing technical inconsistencies in the company’s application. (Slipshod permit applications and regulatory setbacks have been a persistent problem for the company.)

NFE’s most recent disclosures go further: In discussing the company’s future, NFE makes no mention of the second Altamira LNG plant. The company no longer lists the partially completed plant among its portfolio of assets. The new plant is also not featured in the company’s gas portfolio or future earnings plans. NFE only mentions the uncompleted project as collateral for $400 million in non-recourse loans due in three years. (Non-recourse loans are backed by a pledge of collateral: If the borrower defaults, the creditor can seize the collateral but can’t go after other corporate assets.)

Reading the tea leaves, NFE has effectively acknowledged that it no longer has the cash to build its second LNG plant. It might not want to finish the plant even if it could, given the dismal performance of its first plant. Moving forward, if NFE is unable to repay its non-recourse loans when they come due, the company will simply hand over the unfinished LNG project to creditors. This may not mean that the second Altamira LNG plant is dead. But it’s very difficult to see how it will move forward over the next several years.

Insiders have already gotten most of their money out of NFE. This last story is the key to understanding NFE’s slipshod approach to both financial reporting and LNG engineering. By the end of last September—and after almost a decade in business—NFE had racked up $8.9 billion in debt without generating a single cent of free cash flow. Yet despite this lousy performance, the company had paid its shareholders, including company executives and their family members, more than $1 billion in dividends between 2020 and 2025.

The biggest dividend came in January 2023, when the company rewarded its shareholders with a $3 per share dividend, totaling a one-time payout of $623.3 million. The company’s annual proxy statement, published shortly afterwards, revealed that CEO Edens owned 23.2 percent of the company’s stock. His family investment company, Edens Family Holdings LLC, owned another 12.3 percent. The investment firm that Edens co-founded, Fortress Investment Group, owned an additional 5.3 percent. Randal Nardone, who co-founded both Fortress Investment Group and New Fortress Energy with Edens, owned 12.8 percent. All told, Edens, Nardone, and their affiliates controlled 53.6 percent of the company’s shares—meaning that they likely took in $334 million from this special dividend alone. These insiders received significant additional dividends each year from 2020 through 2025, even as the firm sank deeper into a sea of red ink.

The source of this cash for these dividends wasn’t NFE’s business; it couldn’t have been, since the business didn’t generate any free cash flow whatsoever. Instead, the source of cash for these dividends was new investors, including both shareholders and lenders. NFE raised $275 million from its 2019 IPO. The company sold $292 million in additional stock in 2020. In 2023, the year of the special dividend, the company borrowed more than $2 billion. Company executives effectively took some of that money and handed it out as dividends. In effect, they borrowed from Peter to pay … themselves.

The lenders are now bearing the brunt of these financial shenanigans. Edens, Nardone, and their affiliates have no obligation to return the dividends and likely will escape unscathed. But lenders and shareholders who entrusted their money to NFE will walk away with pennies on the dollar.

Related Research