Gas reservation policy design critical as conflict hits global supplies

Key Findings

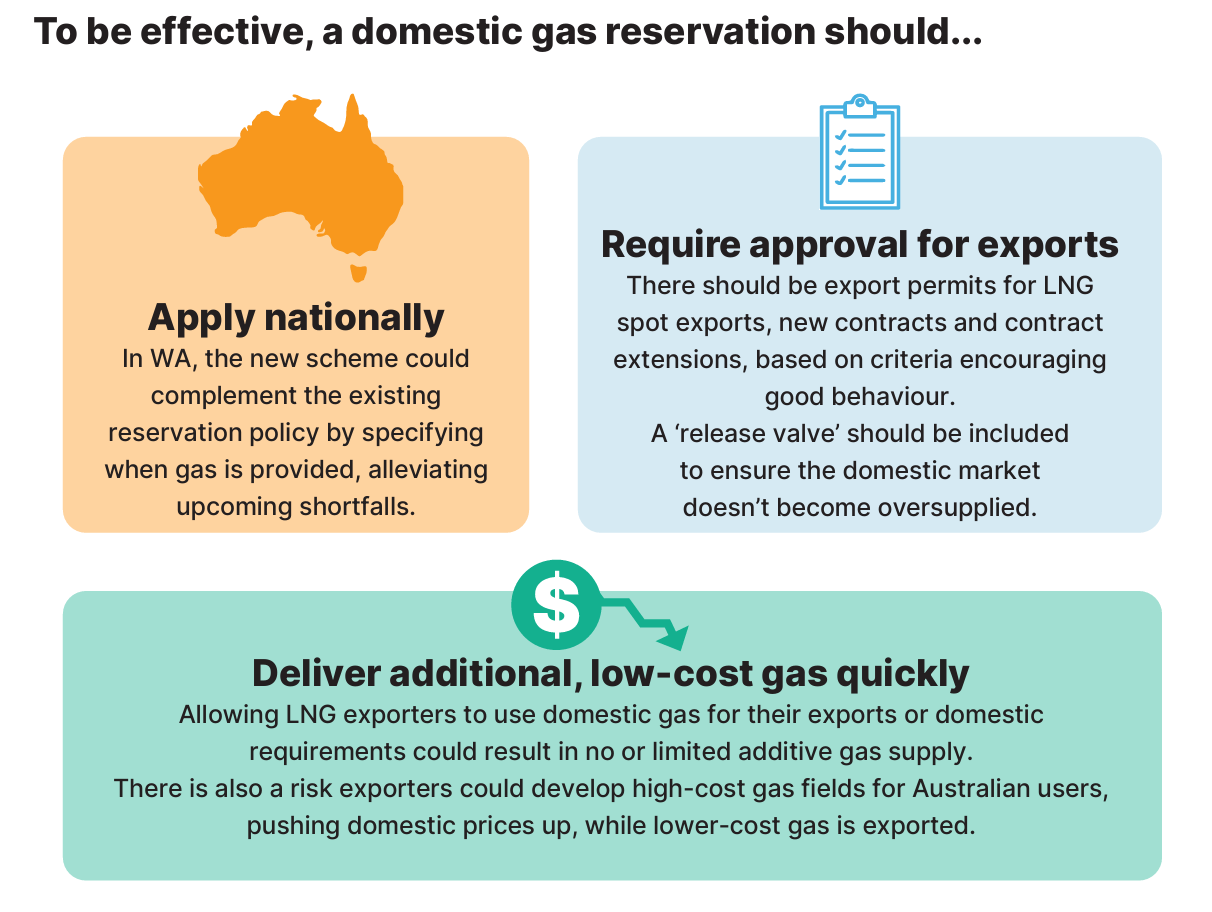

To avoid predicted gas shortfalls, the federal government’s proposed reservation scheme must ensure LNG exporters supply domestic gas when and where it is needed, and be applied nationally.

Allowing exporters to purchase domestic gas to meet export and domestic supply obligations could inadvertently undermine the reservation policy and incentivise the development of higher-cost gas reserves for domestic use, while cheaper gas is exported.

Export permits should be implemented to ensure LNG exporters comply with domestic supply obligations, and prevent new contracting that could affect domestic energy security.

With global gas supplies now caught in the crossfire of the Iran conflict, the economic implications for Australia could be far wider than escalating oil prices and shortages.

Overnight, missiles struck major gas and liquefied natural gas (LNG) processing facilities in Iran and Qatar, which share the world’s largest gas reserve, the South Pars/North Dome field that spans the Persian Gulf.

Like oil, almost 20% of the world’s LNG supply must transit the Strait of Hormuz, where 20% of the world’s oil supplies are stranded. With global LNG supply near capacity, and unable to replace lost supply from the Middle East, LNG prices have almost doubled in Europe and Asia since the conflict began.

In Australia, this unfolding crisis adds a further layer of complexity and urgency for a government already grappling with how to rein in domestic gas prices – and an opportunity.

This is because Australia, as one of the world’s largest LNG exporters, has become intrinsically linked to global LNG market dynamics. This is particularly evident in eastern Australia, where domestic gas prices have tripled in the decade since LNG exports began.

A decade of reactive policy measures by the federal government has only increased regulatory uncertainty for the gas industry and failed to eliminate the risk of imminent gas shortfalls.

To address these issues, the government is designing a new regulatory framework, including a gas reservation scheme that will apply from next year. If not designed appropriately, it risks creating further energy security problems across Australia, rather than resolving them.

A reservation scheme must apply nationally

While the government’s proposed reservation scheme has been motivated by conditions in eastern Australia, both eastern and Western Australia (WA) face longer-term energy security risks because LNG exporters are not required to supply gas domestically when it is needed. The Australian Energy Market Operator forecasts gas shortfalls by 2030 despite WA already having a reservation policy.

There, LNG exporters are required to supply 15% of reserves domestically, but have complete flexibility over when they supply that gas. When domestic prices are lower than LNG prices (as in recent years), exporters have strong financial incentives to delay domestic supply to reduce the net present financial cost of selling into the lower-price domestic market.

This is why WA LNG exporters remain well behind on their obligations, with only 8% of gas production supplied domestically by 2023. Other risks associated with delaying domestic supply, include reserve downgrades (which would lower future domestic supply obligations) and the potential for LNG projects to become financially unviable. As a result, exporters could fail to meet their domestic supply obligations, such as Woodside’s Pluto project, which has supplied just 6% of its required domestic volumes.

The prospect of shortfalls in WA when LNG exporters already lag on their domestic supply obligations highlights the inherent limitation of WA’s reservation policy – it is unable to compel domestic supply when it is needed.

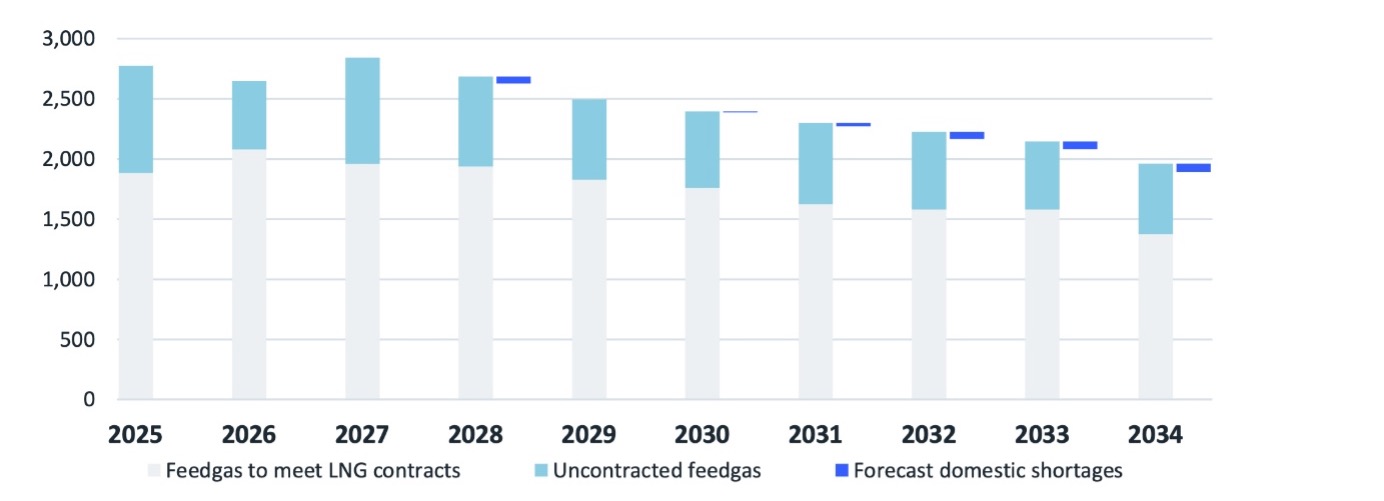

Therefore, it is crucial the new federal reservation works alongside WA’s policy to ensure the state’s LNG exporters supply gas to the domestic market when it is actually needed, by imposing annual supply obligations. However, a federal scheme is unlikely to require WA exporters to supply more than the 15% required under the state policy. IEEFA analysis finds that diverting just 4% of expected LNG feedgas in WA would be enough to address shortfalls to 2034, meaning shortfalls could be resolved within the existing 15% domestic supply requirement (Figure 1).

Figure 1: Domestic shortfalls (WA) vs expected volumes of uncontracted gas, PJ

Source: IEEFA. Browse gas: Expensive, emissions-intensive, unnecessary. November 2025. Page 19.

Reservation must deliver additional, low-cost gas quickly

The reservation scheme will only be effective in addressing shortfalls and challenging gas market conditions if it quickly results in additional domestic supply of lower-cost gas. In practice, LNG exporters will be best placed to quickly increase domestic supply, including by diverting excess gas that otherwise would have been exported. This is because exporters produce more gas than required to meet export contracts, have access to the majority of gas reserves, and often have existing infrastructure in place to facilitate domestic supply (although there may be a need for additional infrastructure investment in WA).

In eastern Australia, Queensland exporters control 90% of reserves, with these reserves being low cost, particularly compared with major new gas basins (such as the Beetaloo or Narrabri).

The government has flagged the importance of exporters having flexibility to enter into commercial arrangements to meet their domestic supply obligations, including purchases from domestic producers. However, this may result in LNG exporters purchasing gas that would otherwise have been supplied domestically, resulting in no or limited additive gas supply. Similar risks arise if exporters are allowed to purchase existing tenements outright; while this may increase the exporter’s domestic supply, it would not necessarily increase overall supply.

Such commercial arrangements may also lead to the development of higher-cost gas reserves, underpinned by contracts with exporters, driving up prices for Australian gas users (given the marginal-cost producer effectively sets market prices) while lower-cost gas is exported.

For this reason, the government should require exporters to supply sufficient gas to offset any purchases from domestic suppliers and to meet their domestic supply obligations. For example, a producer with purchases of 20 petajoules (PJ) would need to supply an additional 20PJ above any reserve obligation.

Approvals should be required for new contracts and spot exports

The Australian government should implement a mandatory export permit framework for all LNG exports (beyond those required to meet existing firm supply commitments), including for discretionary LNG spot exports, new contracts and/or contract extensions. For extensions, approval should be required where the exporter has the right to not extend the contract and instead increase their domestic supply.

As part of this framework, government should develop detailed assessment criteria for new permits, which could include criteria designed to incentivise good selling practices by exporters (such as good faith bargaining and longer-term contracting).

This type of framework would have several benefits, including:

- Providing a mechanism to effectively punish non-compliance with domestic supply obligations (which could sit alongside a broader enforcement regime)

- Allowing government to prevent future sovereign risks concerns due to “overcontracting”

- Tying future export permits to historic and future supply commitments and selling practices.

An export permit framework, alongside a domestic supply obligation, could risk artificial domestic oversupply at times, meaning the government will also need to carefully design a “release valve” to allow higher exports when the domestic market is well supplied. This mechanism could allow exporters to export a defined portion of their annual domestic supply obligation (say 20%) in a given year when specified supply criteria are satisfied. Criteria could include domestic pricing levels and whether gas storage facilities are at or near capacity (including facilities not offering third-party access).

The government will, however, need to be cognisant of the clear risks of strategic gaming of any such mechanism, underscoring the need for effective enforcement.

After a decade of failed policy interventions, the government has an opportunity to implement effective policy settings that will address gas market issues permanently. The key question is whether it will get it right this time.

Related Content