Key Findings

The proposed Amigo LNG offshore export facility would shortchange four gas-fired power plants serving northwestern Mexico.

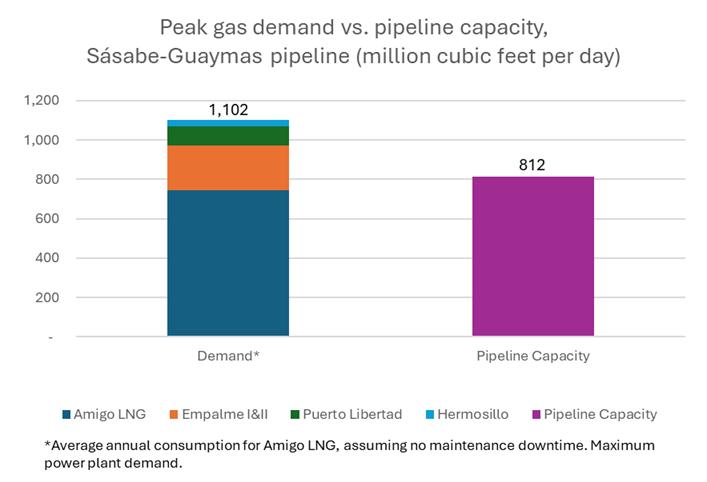

The four plants need up to 357 million cubic feet of gas per day from the Sásabe-Guaymas pipeline. The export facility would need another 745 million MMcf/d, but the pipeline can only carry 812 MMcf/d.

Besides leaving little or no gas for these electricity stations, Amigo LNG would jeopardize gas supplies to a proposed 400MMcf/d connector to the Sásabe-Guaymas pipeline that would serve other power plants and industries.

The gas supply issue poses a serious challenge to the project’s ability to obtain government permits and attract investors.

The company behind Amigo LNG, an offshore liquefied natural gas (LNG) export facility proposed for the Gulf of California, recently told Mexican regulators that the project would export 5.1 million tons of LNG per year (MTPA), making it the world’s largest floating LNG project.

According to the regulatory filing, the Sásabe-Guaymas pipeline, which leads from the Arizona-Mexico border to the Sonoran city of Guaymas, would provide feedgas to the LNG plant. There’s a huge problem with this plan: The pipeline can’t supply enough gas to Amigo LNG without shortchanging four gas-fired power plants that serve northwestern Mexico.

The Sásabe-Guaymas pipeline currently supplies gas to four Sonoran power plants:

- The Hermosillo plant, with power output of as much as 227MW.

- The Puerto Libertad power station, with a maximum output of 632 MW.

- The Empalme I and Empalme II power plants near Guaymas, Mexico, with a combined power output of roughly 1,561 MW.

At full capacity, and accounting for capacity limits on the pipeline serving the two Empalme stations, these four plants can consume up to 357 million cubic feet of gas per day (MMcf/d). Meanwhile, the Amigo LNG plant would consume an average of 745 million cubic feet of gas per day, including feedstock for the LNG, fuel for the liquefaction equipment, and a low-end estimate of natural gas processing losses.*

For all five facilities to run at full capacity, IEEFA estimates that the Sásabe-Guaymas pipeline would need to deliver 1,102 million cubic feet of gas per day to its customers. Yet according to IEnova, the subsidiary of energy giant Sempra Energy that owns the pipeline, the conduit’s maximum capacity is only 812 MMcf/d—300 MMcf/d short of what is needed.

It gets worse. Assuming that Amigo LNG’s annual output target includes two to four weeks of annual downtime for maintenance, the plant’s typical demand while in operation would be roughly 800 MMcf/d, which would leave just a trickle of gas to supply the four power plants.

What’s more, LNG plants’ gas demand rises and falls in regular cycles through the day, with feedgas consumption surging about 10 percent above baseline during daily peaks. Natural gas consultancy Enkon Energy Advisors notes: “These swings are not anomalies. They are a routine feature of how liquefaction plants operate.” So, at the times of day when Amigo LNG requires the most gas, there would be essentially no gas left in the pipeline to supply the two Empalme power plants near the Amigo LNG facility. Power plants farther from the Amigo LNG facility may also experience periodic pressure losses, affecting gas availability.

These numbers could be a best-case scenario, since they assume that Amigo LNG won’t suffer the same sorts of mechanical problems that have plagued other offshore projects. Mexico’s only operating LNG export project, New Fortress Energy’s Fast LNG off the coast of Altamira, has reported process losses of 11 percent of feedgas during its first 18 months of operation, rather than the 2 percent assumed in this analysis. With losses of that magnitude, Amigo’s daily gas requirements could exceed the full capacity of the Sásabe-Guaymas pipeline, leaving literally no fuel to power four major gas-fired electricity stations.

LNG Amigo’s gas demand would create additional challenges for northwestern Mexico’s energy plans. In particular, it could complicate gas supply for the proposed 400 MMcf/d Centauro del Norte pipeline, which would connect the Sásabe-Guaymas pipeline to power plants and industrial gas users in western Sonora and northern Baja California.

These conclusions aren’t a matter of politics, but of arithmetic. The math shows that Mexico’s Federal Electricity Commission (CFE), which controls the full capacity of the Sásabe-Guaymas pipeline, will face difficult choices if the Amigo LNG facility moves forward. When CFE needs power from the four generating plants that rely on the Sásabe-Guaymas pipeline, the agency would either have to divert gas from the Amigo LNG facility or find another power source to keep the lights on in northwestern Mexico. Either way, some of CFE’s customers would be disappointed.

Amigo LNG isn’t out of options for gas supply. Amigo could ask Sempra to build additional compressor stations to boost the throughput capacity of the Sásabe-Guaymas segment, provided the pipeline can handle the additional pressure and that CFE can source additional gas. It could delay construction, hoping that IEnova can provide additional gas to Guaymas by completing the El Oro-Guaymas pipeline, which has been stalled since 2017. Alternatively, Amigo could even propose to source gas from as-yet-unplanned pipelines connecting the U.S. to Guaymas.

All these options are expensive and would delay Amigo, potentially for years. And none of them have been formally proposed to U.S. regulators, Mexican officials, or investors.

It may seem difficult to believe that the applicants for a major LNG project could have forgotten to nail down adequate gas supplies. Yet there’s precedent for this sort of error. In filings with U.S. energy regulators, the backers of the Saguaro Energia LNG project—another LNG facility proposed for the Gulf of Mexico—simply forgot to ask for enough gas to run the liquefaction equipment. That error helped compound multi-year permitting delays that seem to have doomed the project.

Amigo LNG seems to have done something similar. Lingering gas supply challenges could spell serious trouble for the project’s ability both to obtain government permits and to attract investors. Potential lenders and equity partners would be well-advised to view gas supply as a serious, unresolved challenge for Amigo LNG.

*Factors for converting MTPA to MMcf/d are taken from the U.S. Energy Information Administration. “U.S. liquefaction capacity” for Q4 2025, accessed March 22, 2026. Low-end feedgas processing losses are estimated at 2%, given recent gas quality at the Ramal Empalme. See: “Informe Mensual Sobre las Especificaciones del Gas Natural,” accessed March 25, 2026.

Acknowledgment

Research assistance provided by Luis F. Pérez, GeoComunes, and Manuel Llano, CartoCritica

Related Research