Starting in late 2021—before its invasion of Ukraine—Russia began to manipulate Europe’s energy markets by trimming gas shipments and emptying gas storage facilities on the continent. To fill the supply gaps, Europe ramped up its purchases of liquefied natural gas (LNG). A global bidding war for LNG ensued. Wealthy European nations vied with buyers in Japan, South Korea, Taiwan, China, and developing nations for a limited LNG supply, and prices soared to previously unimaginable highs.

The gas price contagion quickly spread to American shores. U.S. LNG exporters bought all the gas they could handle, hoping to reap big profits by selling U.S. gas to overheated global markets. Surging exports, in turn, shortchanged U.S. supplies; domestic gas stockpiles fell to multi-year lows, and wholesale gas prices rocketed to their highest levels in more than a decade.

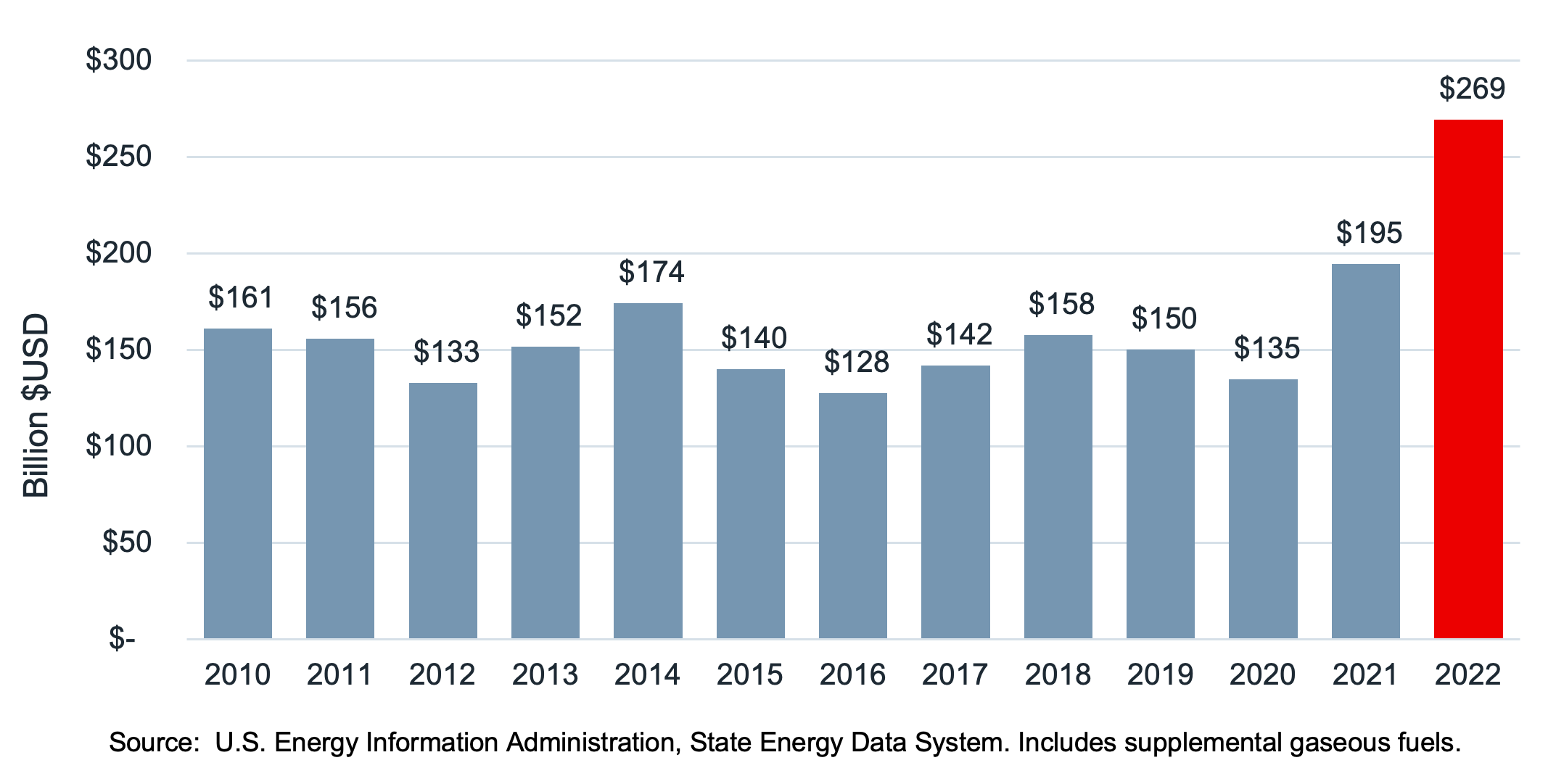

Those price spikes were largely passed on to U.S. consumers. According to the Energy Information Administration, total U.S. spending on natural gas soared to $269 billion in 2022, up from $150 billion in 2019, the last “normal” year before COVID-19 and Russia roiled U.S. gas markets.

US Spending on Natural Gas

It’s impossible to know exactly how much U.S. consumers would have spent if Russia hadn’t upended global gas markets. But there’s absolutely no doubt that surging LNG exports helped trigger the surge in U.S. gas prices.

Between 2020 and 2022, total gas production in the U.S. increased by 7 billion cubic feet per day (Bcf/d), while domestic consumption went up by just 4.6 Bcf/d. With domestic production rising faster than consumption, you might expect prices to stay muted. But exports changed the equation. LNG exports went up by 4 Bcf/d over the same period, and pipeline exports rose by 0.4 Bcf/d. All told, combining growth in bothdomestic consumption and exports, demand for U.S. gas went up about 2 Bcf/d faster than production.

With demand outpacing supply, prices soared. But if exports had grown more slowly, the U.S. gas market would have been in better balance, and prices would have been closer to—or perhaps less than—their long-term average.

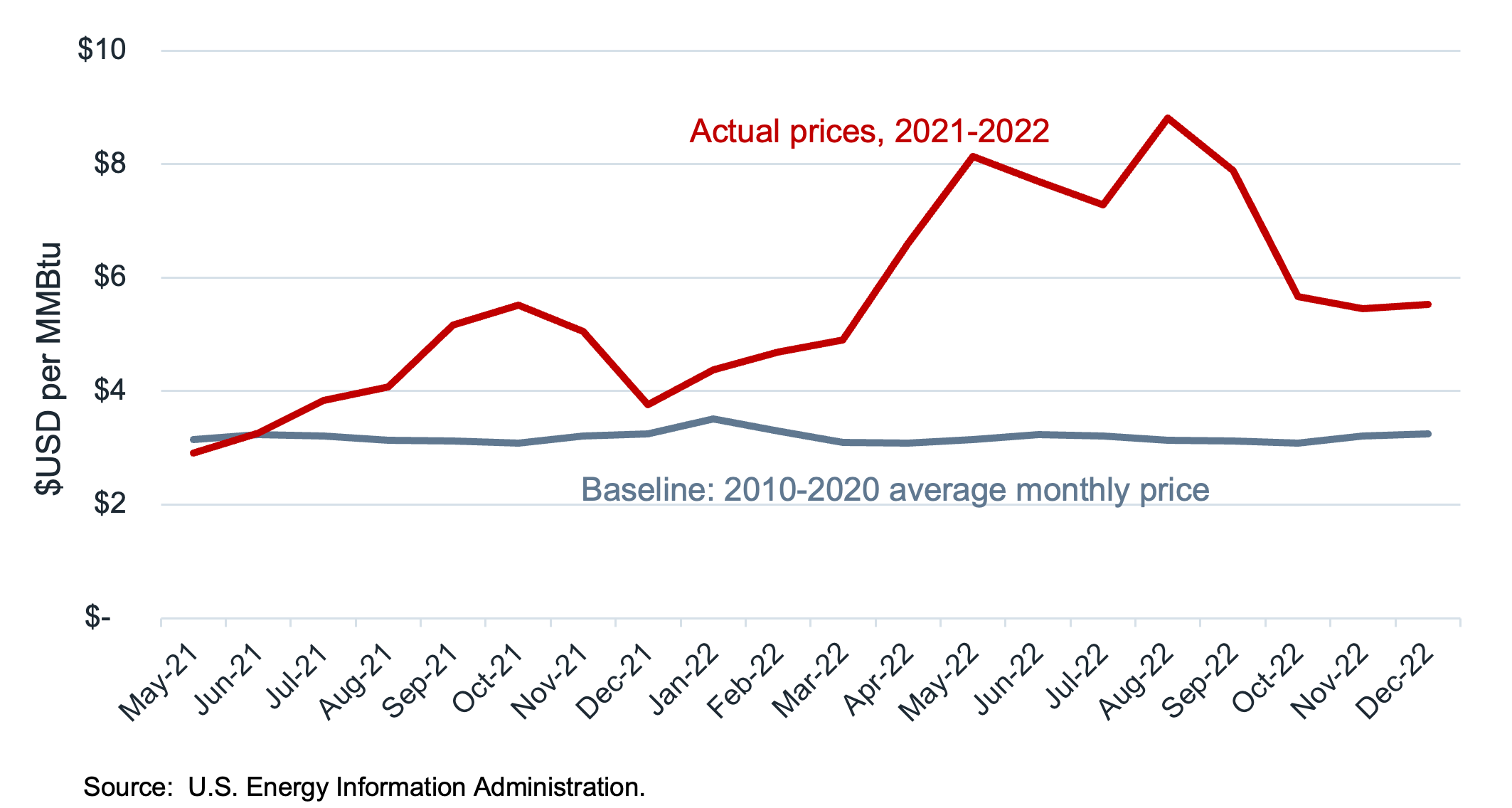

In the years before Russia upended the U.S. gas market, the average monthly wholesale price for gas hovered at just over $3 per million metric British thermal units (MMBtu). FromSeptember 2021 through December 2022—the years of Russian-induced gas market chaos—prices nearly doubled their long-term average.

Average Monthly Henry Hub Prices

Higher wholesale prices fueled inflation for all U.S. consumers, including families heating their homes, businesses, and industries. It became more expensive to keep the lights on, as well. Gas-dependent electric utilities saw their costs rise, and many passed the increased costs to their customers. Some people saw the price increases directly in their utility bills, but much was hidden in the overall increase in prices for goods and services.

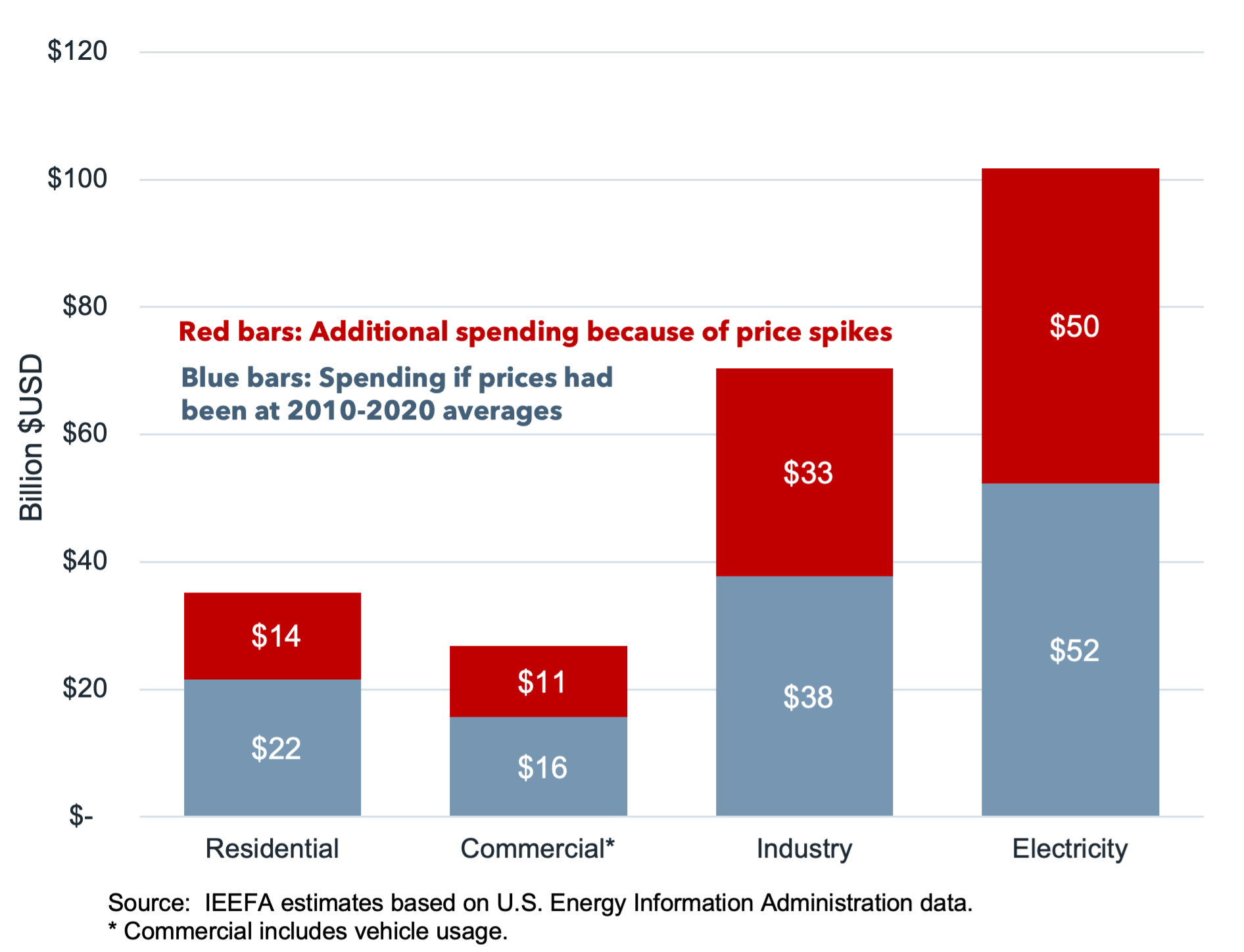

If domestic gas prices had remained at their long-term average, U.S. consumers would have spent roughly $111 billion less on wholesale natural gas purchases from September 2021 through December 2022. Or, said differently, the Russia-induced price spikes cost U.S. households and gas buyers $111 billion, but led to a $111 billion windfall for the gas industry.

The transfer of wealth from gas consumers to gas producers varied by sector. All told, homeowners and renters paid gas companies an additional $14 billion during the market havoc. Office buildings and other commercial users spent an additional $11 billion. U.S. industrial gas users transferred about $33 billion to oil and gas companies. And electric utilities paid a whopping $50 billion more for their fuel.

U.S. Spending on Natural Gas by Sector, September 2021-December 2022

It's high time for the consumer effects of LNG exports to receive the attention they deserve. After all, what’s happened before could happen again. When the circumstances are right—a cold snap in Asia, a pipeline explosion in Europe, unrest in the Middle East—overseas buyers will once again ramp up their demand for LNG and compete directly with U.S. consumers for a limited supply of U.S. gas. The more export capacity we have, the more likely it is that a gas supply disruption anywhere in the world will trigger a price spike here at home. It’s a twist on the old adage: When the world sneezes, the U.S. will catch cold.

Related Content