Australian thermal coal producers are losing their growth markets

Download Briefing Note

View Press Release

Key Findings

China has been the major growth market for thermal coal exporters, and alongside Southeast Asian markets has more than offset declining demand in more mature markets.

However, China’s energy transition has reached a major turning point, achieving a net decrease in emissions in the last year and a likely peak in coal use for power generation.

Thermal coal demand is facing many headwinds in China and Southeast Asia as renewable energy and battery costs continue to plummet, and investments in gas and nuclear increase. Increases in coal generation capacity will not necessarily lead to increases in coal demand.

Amid increasing domestic production, China’s national coal industry association expects that, compared with 2024, thermal coal imports will drop by 22% in 2025, and by more than one third by 2030. Australia will face increasing competition for those declining imports from closer suppliers.

Australia’s coal industry faces an increasingly bleak outlook amid faltering demand and shifting supply patterns among the key growth markets for its thermal coal exports.

In recent years, China has become the largest single driver of global coal demand, with significant growth also seen in Southeast Asian markets. This has offset declining demand in more mature markets such as Japan, South Korea and Taiwan. However, changes to the energy and supply mix in these markets will have profound implications for Australian thermal coal exporters.

China’s energy transition reached a major turning point in the first half of the year: its power emissions fell by 3%, as growth in solar generation counterbalanced the rise in electricity demand. Total coal consumption also dropped, with use of fossil fuels reaching plateaus in other areas too.

This is indicative of a pattern across the region, as renewable energy and battery storage become more cost-competitive than coal-fired power generation. Investments in gas and nuclear are also increasing in the region, further eroding demand for coal.

Despite a large pipeline of new coal power plants in China, utilisation rates are expected to drop, leading to a structural decline in coal demand. Average utilisation rates of coal power plants have already dropped to just around 50% in 2024 and are forecast to halve by 2050.

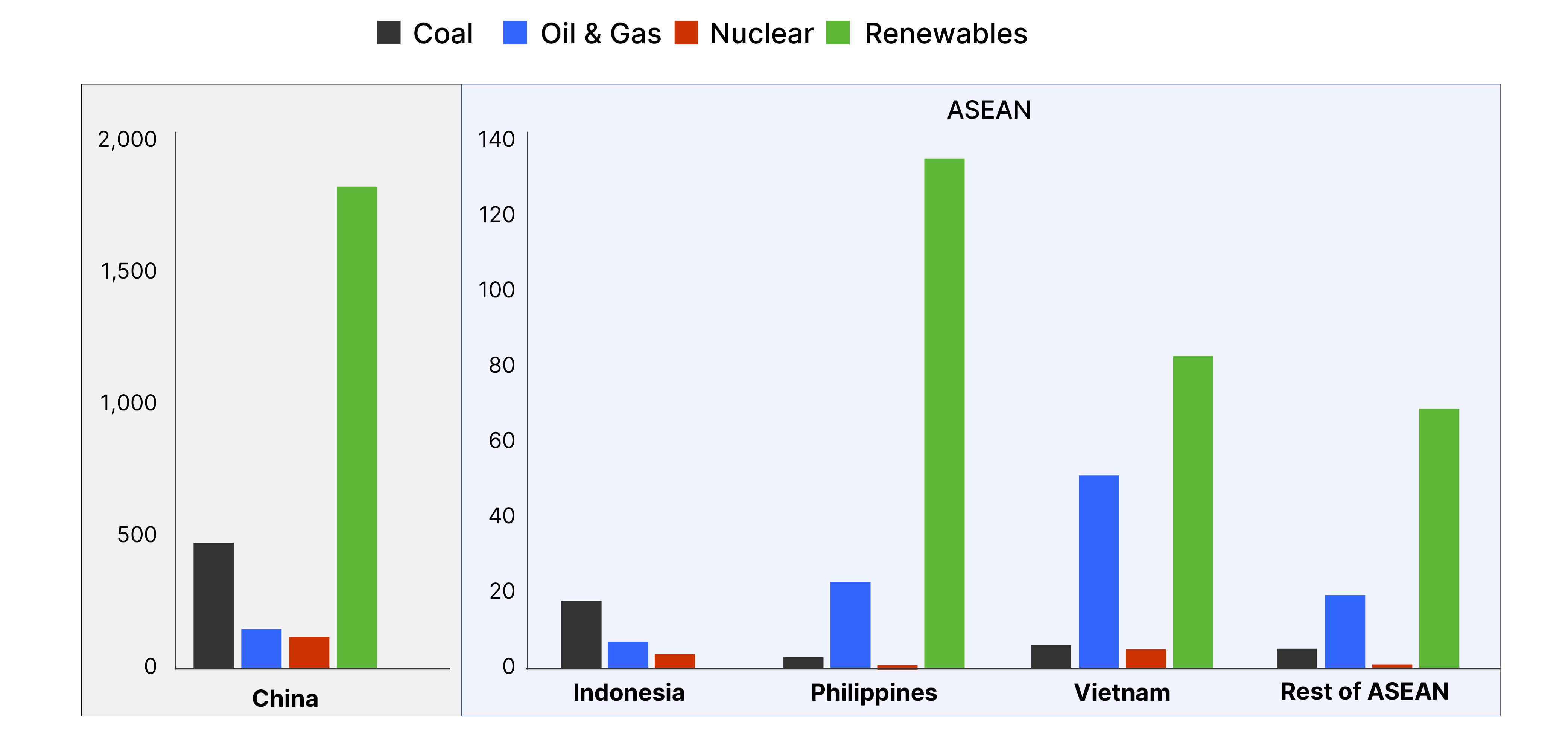

In Southeast Asia, the coal power plants pipeline has significantly declined in recent years as countries move away from coal towards renewables and gas. There is now 10 times more renewable capacity and three times more gas capacity in the pipeline than coal capacity.

Power plants in construction, pre-construction and announced, GW

Source: Global Energy Monitor, Global Integrated Power Tracker data set.

Source: Global Energy Monitor, Global Integrated Power Tracker data set.

While coal producers have flagged carbon capture and storage (CCS) as a potential lifeline in a decarbonising world, its persistently high costs and technological challenges make it an unlikely decarbonisation pathway for coal-based generation. It is likely to be more costly to install CCS in an existing coal power plant than to build new renewable and storage assets to replace the plant.

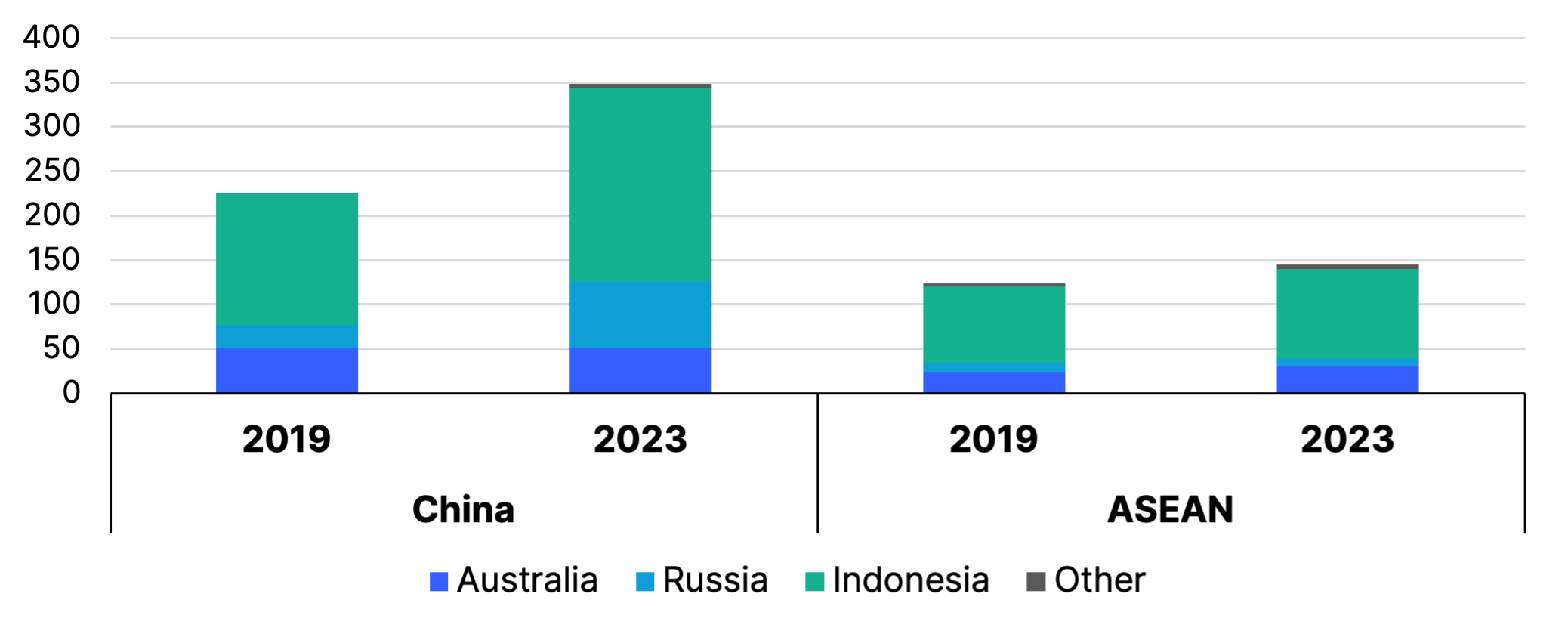

Meanwhile, China is increasing its focus on domestic coal production, as well as shifting to suppliers closer to home such as Indonesia and Russia. In June slowing coal demand growth combined with continued increases in domestic production led to Chinese coal imports slumping to levels not seen since 2023. Compared with last year, China’s national coal industry association expects imports to drop by more than 20% this year and by more than one third by 2030.

Indonesia, the leading supplier of thermal coal to China and Southeast Asia, has captured the majority of the growth in thermal coal imports into both markets. China also nearly tripled its imports of Russian coal following the invasion of Ukraine.

China and ASEAN’s main suppliers of thermal coal, Mt

Source: IEA, Coal 2020 and Coal 2024.

Hopes of these trends reversing with a shift to more advanced and efficient coal plants are likely to be met with disappointment, with financial drivers favouring the use of lower-grade coal such as that supplied by Indonesia and produced domestically. Coal’s dominance in Asia’s energy mix may soon plateau or even go into decline, while supply competition increases.

Ultimately, the changing landscape of energy generation in Asia paints a grim picture for seaborne thermal coal exporters like Australia.

Related Content