Key Findings

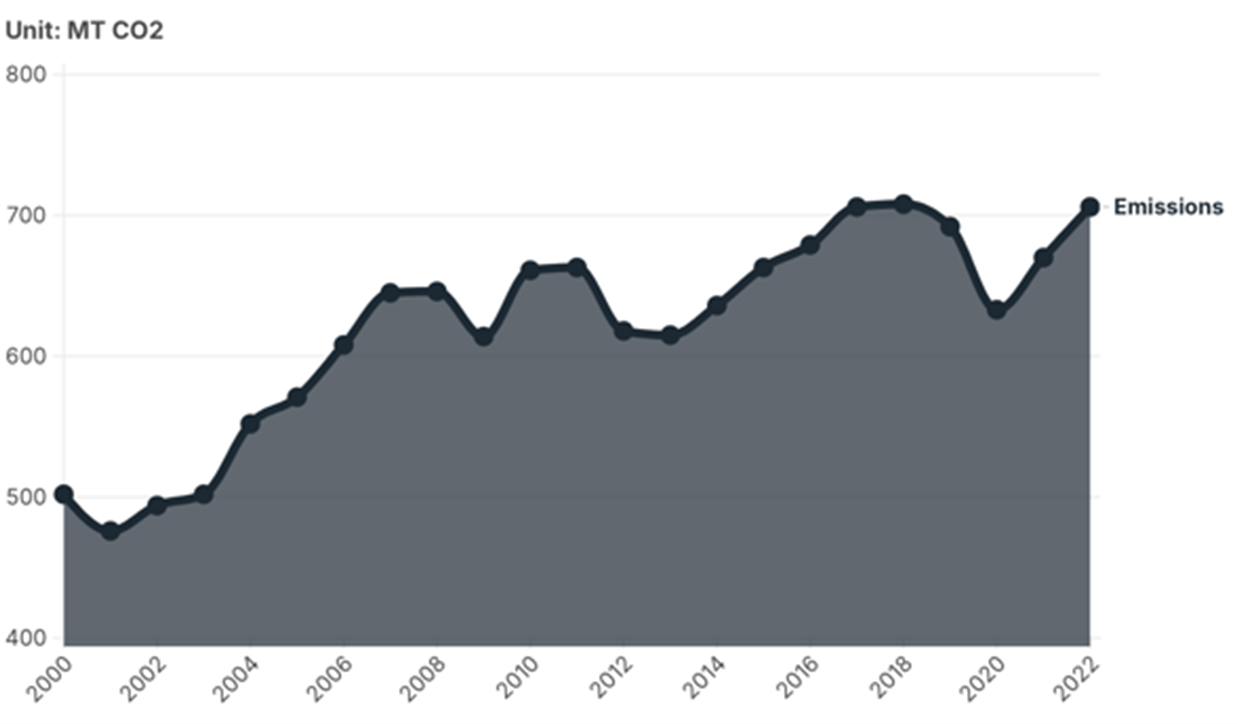

Fossil fuels currently power more than 99% of global shipping, and the sector produces more than 700 million Mt of CO2 annually.

Stakeholders are increasingly considering fossil fuel substitutes such as hydrogen.

Hydrogen, despite some potential uses, currently faces cost, infrastructure, and technological barriers to widespread maritime adoption.

A large-scale buildout of dirty hydrogen capacity risks undermining the sector’s (and planet’s) decarbonization goals.

Executive Summary

Maritime shipping is vital to the global economy, facilitating 80% of trade and enabling trillions of dollars in annual economic activity. It is also responsible for more than 700 million tonnes (Mt) of carbon dioxide (CO₂) a year—a larger carbon footprint, if taken alone, than all but about six of the world’s countries. And with its emissions forecast to continue growing under business-as-usual, the maritime sector’s misalignment with the energy transition is coming into ever-starker relief.

Recognizing the need for action, the International Maritime Organization (IMO) has committed to achieving net-zero emissions by 2050. Alternative energy sources, particularly hydrogen and its derivatives, have attracted attention for their potential to contribute to this goal. However, widespread adoption requires overcoming substantial economic, technological, and operational barriers—and a poorly-planned scaleup of maritime hydrogen could risk undermining net-zero goals in the long run. In this report, IEEFA summarizes the opportunities and hurdles facing hydrogen in shipping.

Figure 1: Historical Emissions From International Shipping

Source: International Energy Agency

Related Content