For Canada’s Teck Resources, a Tough Road on Oil Sands Investments

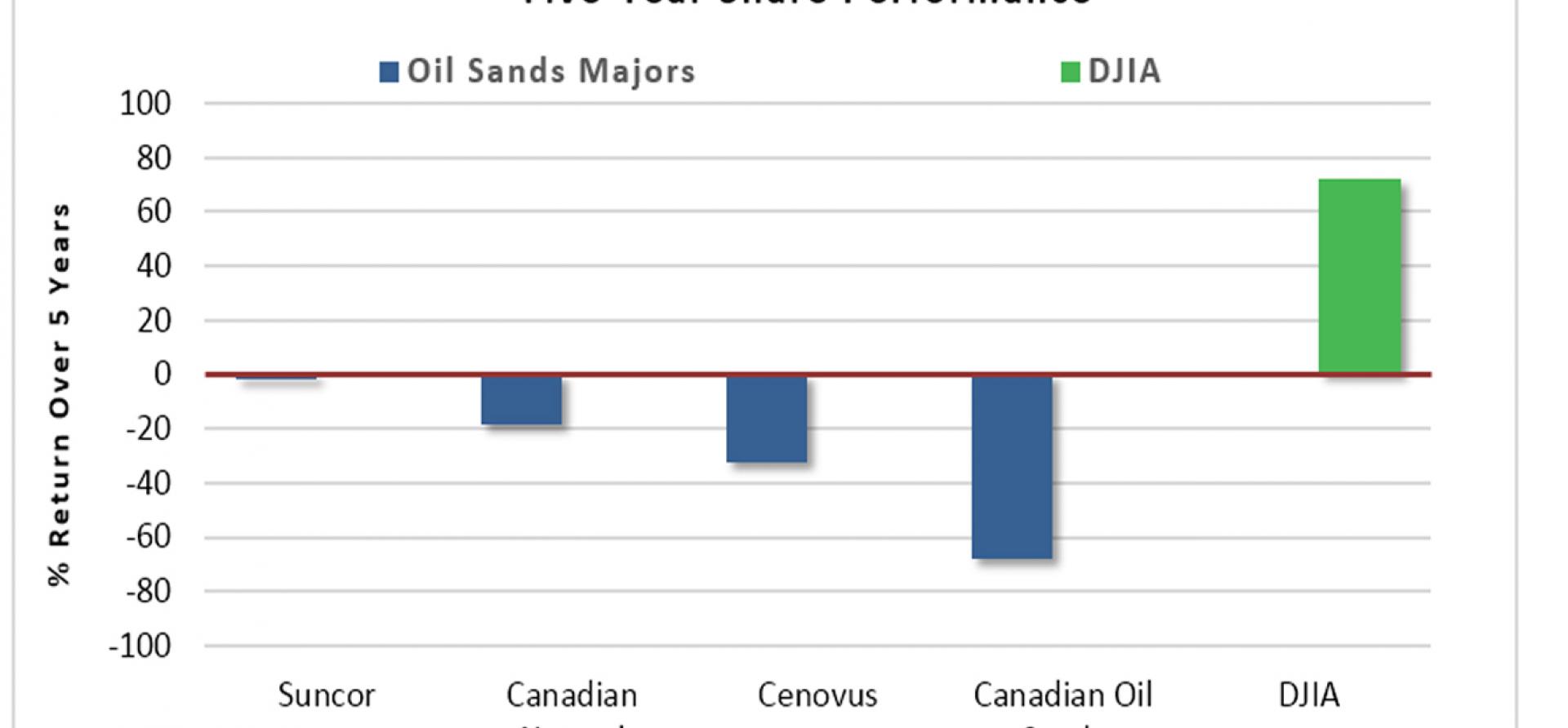

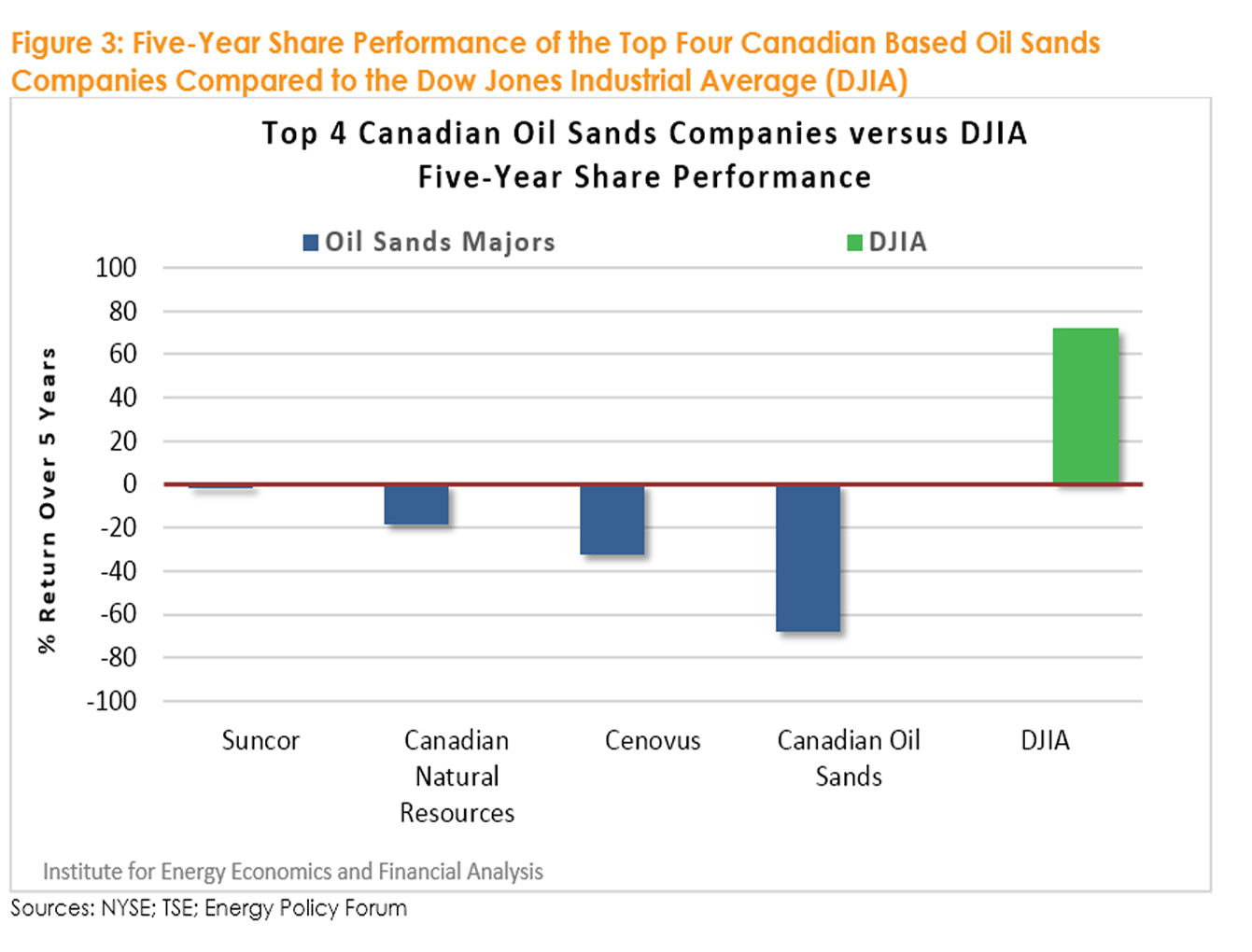

Click to see full chart.

There may be no better example of Canada’s deeply afflicted oil sands industry than Teck Resources, the long-established mining company that is on hard times today in part for its overly optimistic expectations regarding its venture in oil sands, an expensive source of energy.

Today we published a detailed report, “Teck Resources: Rough Road on Oil Sands Investments,” that documents Teck’s many troubles. Our work is supported by a series of weak financial metrics at Teck and by data on larger trends that make oil sands development increasingly untenable.

Here is some of what we discovered:

- Teck’s net income in 2014 plunged to $330 million, down from $951 million in 2013 and $1.145 billion in 2012.

- The company’s free cash flow, while still positive, is only marginal. It fell to $207 million in 2014 from $1.2 billion in 2012, a trend that suggests the company will report a negative free cash flow in 2015.

- Gross profits deteriorated from $3.5 billion in 2012 to $1.3 billion in 2014.

- Operating income fell to $905 million in 2014 from $3.2 billion in 2012.

- Net income plunged to $330 million in 2014 from $951 million in 2013 and $1.45 billion in 2012.

- Capital expenditures were scaled back from $1.7 billion in 2013 to $1.2 billion in 2014.

These numbers help explain why Teck’s stock price today is less than $14, down from almost $63 in 2011.

In addition to the drain on company resources from oil sands investments, we note that the company’s other core businesses are suffering from the general decline of commodity prices worldwide. Most notably, Teck’s metallurgical coal business, which typically accounts for more than a third of its revenues, has faltered and is likely to continue to do so for the next several years. Falling revenues at a time in which the company is venturing forth into new oil sands investments is hurting the company’s outlook.

A good part of Teck’s problems stem from its oil sands program. Teck’s Fort Hills oil sands project, in which the company has a 20 percent interest and in which it has made a capital commitment of $2.9 billion through 2017, is a serious drain on company resources. This commitment will consume a significant portion of Teck’s dwindling cash resources, and Moody’s has cited this draw on the company as a factor in its recent downgrade.

Its Frontier oil sands project, which is still in the planning stages, appears economically unviable in either the medium or long term. Estimates by Oil Change International are that the first phase of Teck’s Frontier oil sands project would require West Texas Intermediate oil prices of at least $140 per barrel to break even and that the project would not achieve a positive free cash flow anytime in the next 50 years. WTI prices today are well below $60 a barrel, and the long-term trajectory of oil prices is highly vulnerable to sluggish demand growth and the abundance of relatively light oil supplies that have contributed to the recent decline in oil prices.

While oil sands projects are a small part of Teck’s overall portfolio, they absorb a large and growing portion of the company’s shrinking resources. The company appears to be financially at risk even without taking its oil sands ventures into account.

Teck is not alone in its oil sands difficulties. Other major oil sands projects have been cancelled or delayed over the past year because of falling oil prices, challenging markets and public opposition to Alberta oil sands development and the pipelines that would be required to push the product to market.

We note in our report, for instance, that oil sands project have been cancelled or placed on hold by companies that include Brion Energy, Cenovus Energy, Canadian Natural Resources, Devon Energy, E-T Energy, Harvest Energy, Husky Energy, Murphy Oil, PTT Exploration and Production, Shell, Statoil and Total. Combined, these delays or cancellations involve potential production of 1.4 billion barrels of oil per day.

Teck, nonetheless, offers a telling snapshot of the bigger picture, and we raise a few points for Teck Energy investors to consider:

- What combination of market factors could turn the company’s finances and operations around so that it could begin to produce more robust returns, and what role would oil sands outlays and revenues play in this turnaround?

- Can Teck afford additional outlays for its Fort Hills project, given its own internal financial weaknesses and the oil industry’s current and projected weak revenues?

- What strategic rationale justifies the continuation of development of the Frontier project, given its long-term horizon, environmental problems and a financial profile that renders it unviable even if oil prices go up?

These are tough questions, to be sure, and our report suggests some tough answers.

Tom Sanzillo is IEEFA’s director of finance.