Renewable energy assets in India: A project finance perspective

Download Full Report

Key Findings

Supply chain disruptions, implementation of trade barriers and a tightening monetary policy pose fresh challenges for renewable energy companies.

Multiple levers remain with renewable energy companies to enhance returns and cushion against downside risks.

The rise in solar module prices is an aberration, and long-term average prices should revert to sub-US$0.20 (before duties and taxes) levels from the current US$0.28.

Executive Summary

The growth of India’s renewable energy sector is among the most successful energy transition efforts globally. In the early years of the renewable energy sector’s evolution, stakeholders perceived almost all business risks to be high. The equity returns for the initial projects were at a higher threshold – and >18% return on equity (ROE) expectations were commonplace. As business risks eased over the last decade, renewable energy technologies emerged as India’s lowest cost energy source.

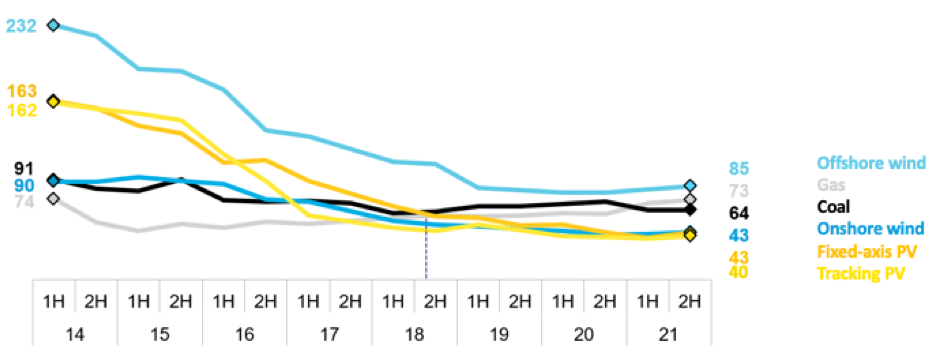

Figure 1: Global Levelised Cost of Energy Benchmarks for Bulk Power, 2014-2021 (US$/MWh)

Source: BNEF

Falling tariffs have resulted in renewable energy capacity in India increasing by nearly 10-fold in the last decade from ~12 gigawatts (GW) in 2010 to around 110GW in March 2022. Over the years, alongside tariffs, ROE expectations have also fallen. From a must-have 18% threshold, the ROE expected now hovers around the 12% mark.

However, fresh challenges have emerged for the sector. Global supply chains have been in tatters lately due to the disruption caused by the pandemic and, more recently, the Russia-Ukraine war. Both wind turbine generator producers and solar module manufacturers have been hiking prices as materials, freight, and labour needs coming out of the pandemic and geopolitical risk weigh down on critical raw material prices. Fresh trade barriers have emerged with the imposition of a basic customs duty (BCD) on the import of solar modules and cells in India. To top it all, sharp, seemingly uncontrollable inflation is making global central banks suck out the system’s liquidity, leading to a steep increase in interest rates.

In this context, a natural question is whether India will be able to continue its renewable energy capacity addition trajectory as witnessed in the past? We believe it will because current challenges will ease in the short-to-medium term, and the industry has enough cushion to absorb these downside risks. Interest in renewable auctions from the large sector players should not wither, even in these unprecedented times.

Module Price Hike – An Aberration in the Long-Term Deflationary Trend

Landed costs of solar modules in the country halted their downward trajectory, rising for the first time (on a sustained basis) in more than a decade. Module costs form ~65% of initial capital expenditure for a typical solar project, with project viability hinging on their trajectory.

Industry belief is that these are aberrations due to the Ukraine war and COVID-19 related supply chain disruptions, especially in China.

It would be fair to assume that long term average prices should revert to sub US$0.20 level (before taxes).

In the short-to-medium term, the presence of non-BCD stock of imported modules, importing cells that attract lower BCD (25% versus 40% on modules) and assembling locally, framework agreements with domestic suppliers, and backward linkages into module manufacturing will provide a good grip on capital costs. Further, even as BCD kicks in, domestic manufacturing capacities buoyed by policy initiatives such as PLI schemes will grow multifold, softening domestic prices.

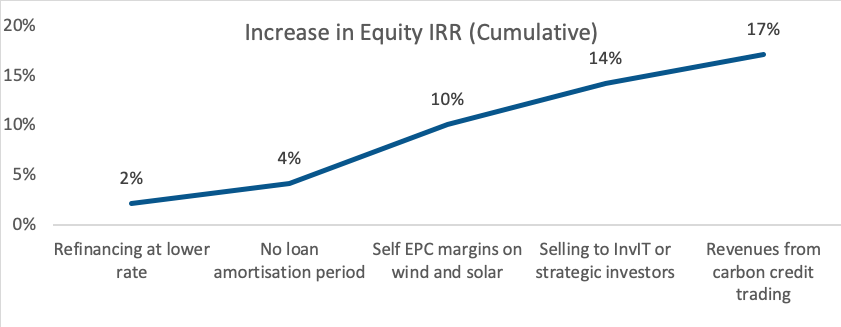

Multiple Levers Remain with Renewable Energy Players to Enhance Returns and Provide Cushioning Against Any Downside Risks

While the “nameplate” return expectations for renewable energy infrastructure assets remain in the ~12% ROE range, several developers have in the past jacked up equity returns through prudent financing improvements (or financial engineering) and capital management practices.

Besides the obvious gains to equity returns through procuring modules at lower rates (through any of the avenues listed above), several other returns enhancing practices cushion against downside risks.

Figure 2: Equity Return Kickers for a Model Wind-Solar Hybrid Project

Source: IEEFA Analysis

Bond market refinancing: Refinancing of project debt post commissioning is commonplace as construction risks subside and the project operationalises. Further, a non-amortising period of 3-5 years often accompanies a bond market refinancing, especially in offshore market issuances.

EPC margins: Most of India’s large renewable energy companies currently have their engineering, procurement and construction (EPC) divisions. Even when competitively considered, EPC margins of 10% (on non-module costs for solar) are a fair assumption in renewable energy projects today.

Stake sale in operational projects: Just as the cost of debt reduces for operational and de-risked projects, the cost of equity also reduces. India has been witnessing this churn with stake sales in operational projects to strategic and financial investors for a long time now. With the recent success of InvITs, much larger pools of such lower cost equity are accessible to developers today.

Carbon credits trading: Several players have started considering the revenues they earn from selling carbon credits as an important source of income. Carbon prices in India have ranged from US$1-10/tonne in the recent past. Currently, about 98% of the carbon credits generated in India go to developed economies. The government is trying to create a domestic marketplace. Carbon credits trading is one of the only enhancements that generate additional revenue for the project. It improves equity IRR as well as project IRR, thereby making it more viable. To be fair, these “return enhancements” might be available with only the top rung able to push returns to higher levels. Still, the reality is that a large proportion of India’s renewable energy capacity will be added by the largest players already operating in the industry, given the capital-intensive nature of the business and competition in the sector.