Key Findings

Australia has become highly vulnerable to oil price shocks due to its reliance on imports, and is highly exposed to Middle East supply disruptions.

Oil price shocks have been a key contributor to all six recent inflation spikes. Traditional monetary tools can only limit spillover impacts, often at a significant economic cost.

Central bankers are calling for the energy transition to accelerate for price stability. Transport electrification could halve Australia’s oil use by 2050 and blunt its impact on inflation.

Australia’s price stability toolkit should include policies to accelerate transport electrification and grid modernisation, and discounted interest rates for electric vehicles.

Executive summary

This report analyses recent changes in Australia’s oil demand and supply, the impact of oil shocks on Australia’s inflation, how those are addressed through traditional monetary tools, and the tools that could be added to Australia’s price stability toolkit to build more resilience to oil price shocks.

Australia has become highly exposed to oil shocks

Since 2000, Australia shifted from being mostly self-reliant for oil products to mostly import-reliant. In FY2024-25, Australia imported the vast majority of its three key oil products: diesel (90%), jet fuel (80%) and petrol (68%). During this period, the country’s use of diesel and jet fuel increased materially, multiplying by 2.5 and 1.8 times respectively. Australia’s diesel use growth is at odds with other countries. It is now the world’s largest importer of diesel, representing 10% of net global seaborne trade. Australia is also the third-largest importer of jet fuel and petrol, representing 8.3% and 6.7% of global seaborne trade respectively. This is well above the country’s share of global GDP.

Scale of Australian oil product imports

Australia imports 96% of its refined oil products from Asia, which is highly reliant on Middle East oil. Our two largest suppliers, representing half of our supply, source about 70% of their crude oil from the Middle East. Global trade of diesel, petrol and jet fuel is also dominated by Asia and the Middle East. As such, Australia has become highly vulnerable to any supply disruptions in the Gulf region. This is exacerbated by Australia’s relatively low oil stockpiles compared with similar countries.

Oil shocks have a large impact on inflation

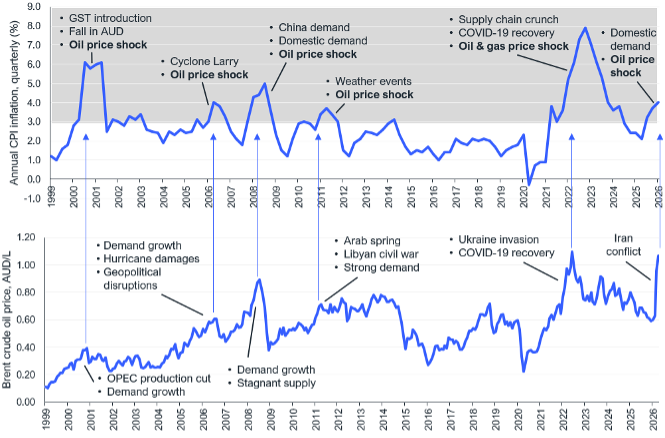

Since 2000, oil prices have become highly volatile, in part due to frequent geopolitical tensions as well as the low price elasticity of oil demand. In that period, oil prices increased by about 6.9% a year, and oil costs by about 8.9% a year, well above the annual Consumer Price Index (CPI) increase of 2.8%. The growth was not linear, with many oil shocks driven by a combination of supply- and demand-side factors.

This century there have been six main occasions when inflation exceeded the Reserve Bank of Australia (RBA)’s target of 2–3%, with oil price shocks a primary driver for each. Oil affects inflation in three ways. It has a direct impact through household transport expenditure, which contributed a one percentage point increase to the CPI in March 2026. It has an indirect impact by increasing the cost of goods and services: oil accounts for 2–2.5% of domestic costs, and could account for more through global supply-chain costs. Oil prices also have an outsized contribution to inflation expectations, which has flow-on effects.

Contribution of oil price shocks to spikes in Australian inflation

Traditional monetary policies have limitations

The RBA typically uses three main tools to maintain price stability: inflation targeting, increasing interest rates and forward guidance. In the case of oil price shocks, central banks focus on countering spillover impacts of high oil prices on broad-based inflation, using a graduated set of responses depending on the likely magnitude of the spillover. For small shocks, they may “look through” the event; for severe shocks with a high chance of unanchoring inflation expectations, they will take forceful monetary policy action. The RBA mentioned the risk of second-round effects from oil price increases as part of its decision to increase the cash rate by 0.25% in May 2026. In the case of an initial supply-side shock (as is the case with the Iran conflict), a forceful response can have high economic costs, potentially leading to a recession.

Given the increasing volatility of oil prices, and its recurrent impact on world economies, some central bankers in Europe are calling for a reduced reliance on fossil fuels to protect price and economic stability. However, monetary action to constrain the spillover of oil price shocks makes it harder and more costly to transition to the very technologies that can protect the economy from the impacts of future oil price shocks.

Technologies are now available to shift away from oil, and Australia doesn’t need to remain at the mercy of global oil markets. It now has the option to sever its exposure to oil price shocks — and the inflation that follows. But it needs to add new tools to its price stability toolkit to do so.

Three levers should be added to Australia’s price stability toolkit

1. Accelerate transport electrification

Transport is responsible for nearly three-quarters of Australia’s oil use, and is the biggest driver of inflation through its direct and indirect impacts on household costs. Electrification of road transport is the most promising opportunity to materially and cost-effectively reduce oil use in the transport sector. Not only can it reduce exposure to oil shocks, but exposure to energy price volatility overall. It also reduces exposure to energy imports by shifting to domestically generated electricity.

It is possible to more than halve road transport oil use by 2040 and reduce it to near zero by 2050, which would dramatically reduce oil use’s impact on inflation. However, trends point to more modest reductions. In particular, oil use in heavy transport is expected to increase to 2040. Government support is needed to accelerate the shift to electric vehicles (EVs).

2. Accelerate grid modernisation

Fully electrifying Australia’s road transport would require large volumes of electricity – equivalent to 42% of today’s electricity demand. A large scale-up of electricity generation, storage and transmission will be required. Accelerating transmission grid expansions (or innovative alternatives) is one of the most critical enablers to rapidly increasing electricity supply.

Grid planning and upgrades are also required to deploy EV charging infrastructure, with power needs particularly high for heavy freight charging. Ensuring EV charging is managed effectively will be key to reducing the cost of distribution network upgrades, and will require new data, analytics capabilities and technical standards. Innovative, cost-reducing solutions should also be investigated, such as co-locating charging stations with renewables and batteries. Bidirectional charging can deliver significant cost benefits to the electricity system and EV owners.

3. Reduce the cost of finance for EVs

EVs represent the largest investment required in the net zero transition, estimated at AUD1.3 trillion to 2050. EVs still carry a large price premium in most segments, and their business case worsens with increases in interest rates. The CEFC is limited in the scale and discount it can offer.

Related Content