Deal or no deal: Five energy market lessons from the Middle East crisis

Key Findings

Fossil fuel volatility is an economy-wide risk, affecting household costs, public budgets, trade, industrial supply chains and investment decisions.

Import dependence and LNG reliance continue to expose countries to price spikes, geopolitical disruption and uncertain supply, even when buyers diversify suppliers.

The most durable energy security strategy is reducing exposure to volatile fossil fuel markets through renewables, grids, storage, efficiency and electrification.

Read and subscribe to IEEFA Market Signals on LinkedIn, IEEFA’s monthly newsletter connecting regional energy-market analysis to global trends, risks and opportunities.

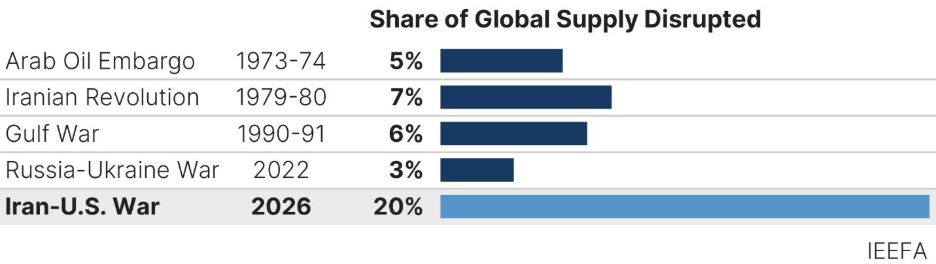

Amid on-again, off-again ceasefire deals and disruptions, the Middle East crisis is following a familiar script: prices swing, governments seek emergency supply, and companies and investors constantly reassess disruption risks. Even if hostilities ease, IEEFA estimates that oil flows through the Strait of Hormuz could take at least six months to return to pre-conflict levels, with LNG taking longer.

But the crisis is exposing a deeper weakness – the belief that another cargo, contract, or supplier can turn fossil fuel dependence into security. Oil and gas volatility spreads far beyond fuel markets, impacting households, public budgets, trade, industry, and investment. Whatever happens next, five lessons remain:

1. Imported fossil fuels are now an economic-security liability

The risk of prolonged escalation includes higher fuel costs, inflation, pressure on interest rates, trade-balance stress and slower growth.

Asia is the clearest example. IEEFA has calculated that Pakistan, Japan and the Philippines each sourced more than 90% of crude oil supplies from the Persian Gulf, leaving them exposed to disruption and price spikes. In South Asia, India imports about 90% of its oil, while also relying heavily on imported LPG and gas.

Australia shows that even indirect exposure carries risk: it depends on Asian refineries supplied by Middle East crude, while holding the IEA’s smallest petroleum stockpiles and producing far less oil domestically than 25 years ago.

It’s clear: energy security strategies built around imported fossil fuels also present industrial, fiscal, and inflation risks.

2. LNG isn’t passing its “secure transition fuel” test

The crisis is exposing LNG as a source of geopolitical and price risk, rather than a flexible, reliable transition fuel. Projects have already been cancelled in China and Vietnam, while other countries are taking steps to accelerate clean energy deployment and reduce imported fossil fuel dependence.

Europe’s move away from Russian pipeline gas has increased reliance on LNG, without removing geopolitical risk. From March to May, the U.S. supplied 60% of EU LNG imports, while Russian volumes rose 25% year on year. Yet combined EU and UK LNG imports fell 3%, reinforcing the case for cutting gas demand rather than simply switching suppliers.

In Australia, LNG cuts both ways. It is one of the world’s largest LNG exporters, yet it faces high gas prices because much of its gas is exported as LNG. That leaves households and businesses exposed to global price volatility.

LNG can diversify routes and suppliers, but it does not remove exposure to global commodity markets.

3. The costs are landing on consumers, taxpayers and exposed industries

Governments need short-term tools in a crisis. Fuel rationing, price caps, subsidies and emergency supply deals may limit immediate damage. But temporary protection may reinforce long-term fossil fuel dependence.

Japan shows the fiscal pressure. IEEFA research notes that Japan spent more than USD77 billion on fuel subsidies between 2022 and 2024. That level of support is hard to sustain and even harder for lower-income importers to copy.

In the U.S., the risk lands more directly on consumers. The rush to build gas power plants means consumers face significant risks from natural gas price spikes caused by weather and geopolitical events, and that rising LNG exports could add both price volatility and persistent increases in gas costs. And in Europe, gas still has a disproportionate influence on electricity prices.

South Asia shows the same strain more acutely. India's oil marketing companies are absorbing over USD4 billion in losses on cooking fuels alone, while Bangladesh could pay over USD1 billion in LNG subsidies over three months just to meet power demand.

Relief today can become exposure tomorrow if it keeps economies locked into volatile fuel markets.

4. The shock is spreading beyond oil and gas

The crisis has also tested supply chains. Disruption can affect food, manufacturing, technology and heavy industry.

The Strait of Hormuz accounts for one-third of global seaborne fertilizer trade and 7–8% of global fertilizer supply. The region also supplies a large share of helium – critical for semiconductor manufacturing – and polyethylene, polypropylene and aluminum.

In India, petrochemical shutdowns that put roughly 5 million jobs across 30,000 plastics MSMEs at risk, while steel producers face gas shortages. In Bangladesh, high spot LNG prices and rising freight costs are adding pressure to the energy sector and the garment export industry.

For investors and policymakers, fossil fuel volatility is an economy-wide risk – not just an energy-sector one.

5. The durable response is demand reduction, electrification, and clean energy

The durable response is to reduce exposure to volatile fossil fuel markets, not simply find other suppliers.

We are already seeing that in South Korea, which has framed the crisis as an opportunity to accelerate renewables.

In South Asia, IEEFA has argued that renewables can act as a natural hedge against fossil fuel shocks. In India, electric cooking can be 37% cheaper than non-subsidized LPG and 14% cheaper than piped natural gas. Pakistan’s rapid solar buildout has helped reduce exposure to imported fuel shocks.

Australia’s lesson is similar. IEEFA analysis maintains electrification is the most promising solution for longer-term resilience because it can reduce oil imports at scale. Oil shocks have contributed to recent inflation spikes, exposing the limits of monetary policy.

Whatever happens next, the market lessons remain: economies are more secure when they rely less on volatile imported fuels.

This article is adapted from the first edition of IEEFA Market Signals, IEEFA’s new monthly LinkedIn newsletter connecting regional energy-market analysis to global trends, risks and opportunities. Read and subscribe to IEEFA Market Signals for future editions.

Related Research