Potential implications of the Iran conflict for Canada’s fossil fuel sector

Key Findings

For Canada, a key question related to tensions in the Middle East is how the conflict and resulting market volatility could affect LNG and crude trade flows, investment decisions, and long-term exports.

Higher prices may boost investor sentiment towards oil and LNG assets, but translating a geopolitical premium into materially improved project returns is tricky—and risky.

An accelerated global shift from fossil fuels to renewables in response to the current energy crisis could end up limiting long-term growth prospects for oil and gas exporters, including Canada.

Elevated market conditions are threatened in the shorter term by a potential return to normalcy, the market glut waiting at the other end of the conflict, and the increasingly competitive economics of renewable energy.

Recent escalation of tensions in the Middle East has transformed a regional confrontation into a global energy shock. For Canada, a key question is how the conflict and resulting market volatility could affect liquified natural gas (LNG) and crude trade flows, investment decisions, and long-term exports. At first glance, this shock may appear to open up opportunities for the domestic energy sector. In the short term, higher global energy prices could benefit the Canadian fossil fuel sector and government coffers, as well as make Canadian LNG assets more attractive to investors. But these higher prices are tied to a geopolitical premium, not a structural trend—and increasing output and infrastructure buildouts in response could be risky in the longer term. Relying on price shocks related to geopolitical conflict is precarious, as these conditions are likely to remain volatile and unpredictable. While the conflict may enhance Canada’s appeal as a stable energy partner, the recorded disruptions, volatility, and market response may ultimately accelerate the global push to reduce dependence on imported fuels altogether.

Conflict-related disruptions have led to a sharp surge in global energy prices

The effective closure of the Strait of Hormuz—a narrow shipping route that carries about 20% of global oil and LNG trade—along with strikes on Qatar’s Ras Laffan complex, the world’s largest LNG production facility, has knocked out roughly 20% of global LNG export capacity (around 125 billion cubic metres) and severely disrupted 20 million barrels of crude oil per day. In response, LNG prices in Asia, measured by the Japan Korea Marker (JKM), and in Europe, measured by the Dutch Title Transfer Facility (TTF), have risen by more than 50%. JKM climbed from about $11–$12 per million British thermal units (MMBtu) before the conflict to roughly $18/MMBtu, and TTF followed a similar path. Crude benchmarks have also soared. Western Canadian Select (WCS) rose from about $50 to more than $90 per barrel—an increase of nearly 80%—before easing in recent weeks. Likewise, West Texas Intermediate (WTI) prices increased from $64 to $103 per barrel, while Brent prices rose from $69 to a peak of $113. Freight rates also spiked with spot charter rates for LNG tankers surging over 600% and reaching peaks of $300,000 per day.

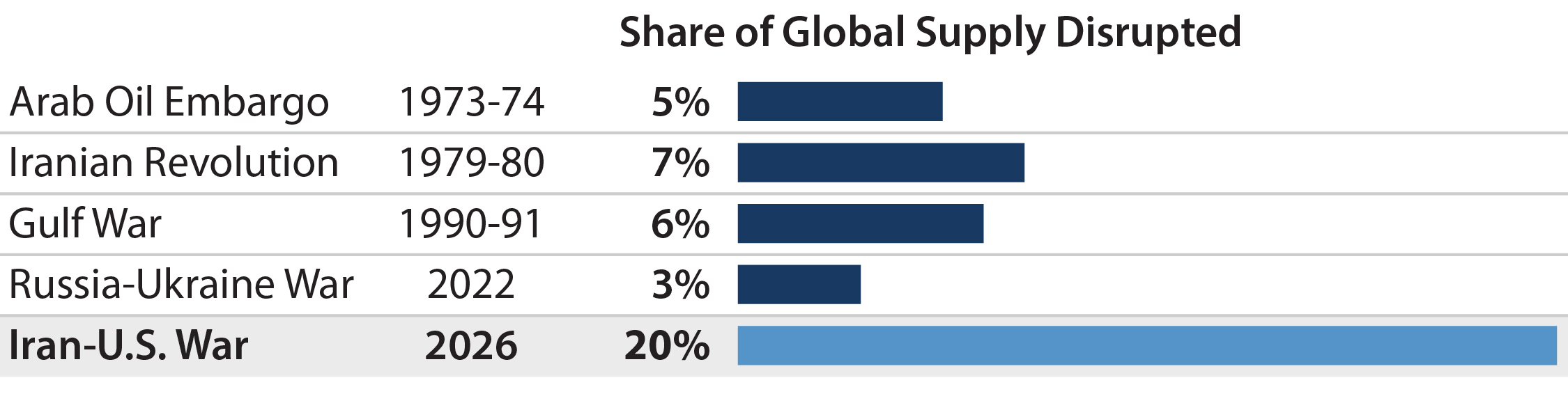

Figure 1: Historic oil shocks: Estimated share of global supply disrupted

Source: Federal Reserve Bank of Chicago, IEA, World Bank, Investing.com

LNG markets face greater structural vulnerability than oil

Although both crude oil and LNG markets are affected by the conflict, LNG appears more structurally exposed to sustained supply disruptions for a couple reasons. First, LNG production is more highly concentrated. Qatar’s Ras Laffan facility—now shut down due to repeated direct military attacks—normally plays an outsized role in global supply. By contrast, oil production is geographically dispersed across thousands of oil wells, fields, and flow stations with multiple export routes and pipeline alternatives. Second, the LNG sector has a relatively limited buffer system. Crude oil markets may benefit from coordinated inventory buffers by organizations such as the IEA, whose members are legally required to hold 90 days of import cover, or a supply coordinating producer group like OPEC. However, such regulating mechanisms are absent from the global LNG sector. Gas is also more expensive to transport and store with many LNG buyers holding limited reserves in storage relative to crude oil.

Price spikes will boost producer and public finances in the near term, but may weigh on consumers and households

In the short term, higher global energy prices will likely provide some upside to Canada’s LNG and crude oil exports. Assuming output remains constant, this geopolitical premium will translate to increased producer revenues and, all things equal, stronger operating cash flow, improved profitability, and potentially higher distributions to shareholders. Companies with downstream operations, such as crude oil refineries, may also benefit further as the prices of petroleum products rise faster than crude input costs. LNG Canada may see a weaker boost in the immediate term, as LNG export revenues are typically tied to long-term contracts priced with formulas that may lag real-time spot prices. Government coffers stand to benefit fiscally as royalties, corporate taxes, and other revenue streams tied to commodity prices and producer revenues rise. At the macroeconomic level, higher-value exports are starting to reflect in terms of trade data, with Canada reporting a trade surplus in March—the first in six months.

The ability for Canadian energy producers to materially increase output in response to higher prices is constrained in the short term by infrastructure and market limitations. Restricted nameplate capacity as well as long lead times required to permit, finance, and construct additional export infrastructure limit the ability of LNG Canada or other proposed projects to rapidly commence or scale production. Similarly, increasing oil sands revenue through meaningful output growth requires advance planning, material capital investment, and execution of complex expansion programs often laid out over a 12-24 month development period.

Consumers and households are unlikely to share in the immediate upside due to emerging inflationary pressures. A temporary suspension of the federal fuel excise tax may provide limited relief, but is unlikely to fully offset overall increases in energy-driven costs for food, travel, and transportation. Should price increases begin to seep into the consumer price index (CPI), the Bank of Canada may eventually respond with tighter monetary policy or delayed easing. This could translate into relatively higher interest rates, increasing mortgage, debt service, and business borrowing costs.

Geopolitical price spikes may not translate to improved long-term project returns

Higher prices may boost investor sentiment towards oil and LNG assets. But translating a geopolitical premium into materially improved project returns is tricky—and risky. Large-scale energy infrastructure projects are typically assessed over multi-decade time horizons, with return projections heavily dependent on long-term discounted cash flow assumptions and the ability to recover upfront capital expenditure over extended payback periods. For price shocks to materially alter project returns, developers must assume these market conditions persist for extended periods of time, e.g., decades—not just a few quarters or even a few years. While this cannot be excluded, it is deemed unlikely. Energy markets have a long history of rebalancing and sharp price spikes have often triggered measurable demand destruction, efficiency measures and fuel switching—which act to weaken demand growth. The current crisis is just a few months old, but there are already indications that a similar dynamic is at play.

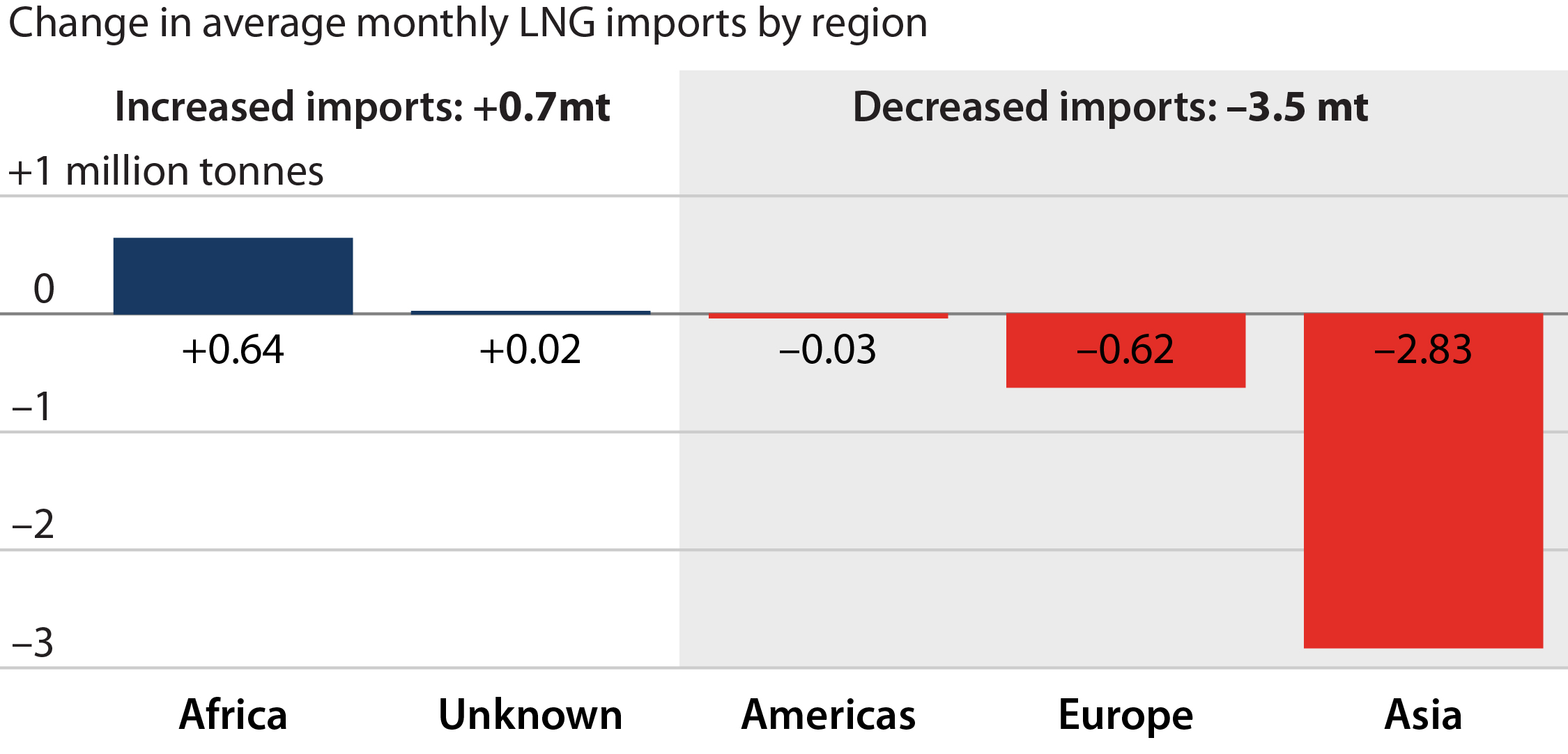

Figure 2: Net change in average monthly imports by region (March - May 2026)

Source: IEEFA calculations based on Kpler data

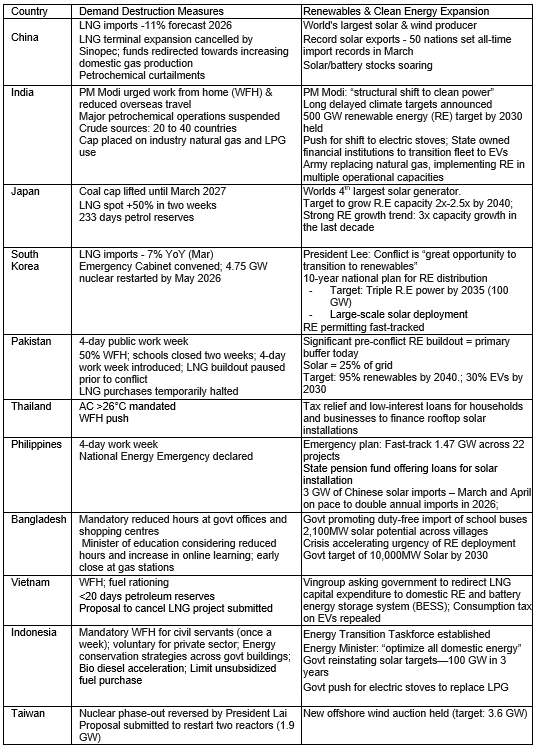

In Asia, where the impact of the crisis is being felt most acutely due to heavy dependence on the Middle East and limited storage, major importers such as India, Pakistan, China, and Japan have started taking action to reduce their vulnerability as seen in Table 1 below:

Table 1: Asian energy security responses to the 2026 Iran conflict*

Source: IEEFA, IEA, CREA, Carbon Brief

*Several countries—notably Japan, South Korea, Thailand and Bangladesh—have reactivated existing coal capacity as a stop gap measure. This is expected to be temporary, and no new investments or commitments have been announced in response to the conflict. However, some experts in Japan argue that the crisis could lengthen the country’s embrace of coal.

A potential future scenario in which the hostilities cease, renormalizing transit through the Strait of Hormuz, would return significant stranded supply to the market, support production restarts, and enable repairs on damaged infrastructure. Combined with fuel switching and demand destruction already underway, the resulting increase in supply could trigger a mean reversion in price levels. The market also has to contend with a tidal wave of new LNG supply expected to come online which, though delayed by the conflict, is still expected to materialize in coming years. Transitory price spikes, by themselves, may be insufficient to materially alter project economics. Accelerating long-duration, capital-intensive export infrastructure in response to disruptions caused by an international conflict is difficult to justify.

The crisis may create a stability premium for Canadian energy exports—while eroding long-term demand

A range of competing factors are likely to shape long-term structural outcomes of the crisis. On one hand, repeated conflicts that expose the fragility of energy supply chains tied to unstable regions may push countries to rethink their entire supply architecture, with a focus on diversification and reliance on more geopolitically stable sources of energy. In this context, Canada may become relatively more attractive to energy markets due to its reserves and supply infrastructure largely insulated from conflict zones and removed from contested shipping lanes. This could provide tailwinds to proposed LNG projects looking to sign deals with off takers.

On the other hand, the adjustments and policy thrusts triggered by the current crisis may, over time, structurally erode the role of imported oil and gas in key demand centres. Historically, the twin oil crises of 1973 and 1979—both caused by conflict driven disruptions to global energy supply—triggered market responses that permanently altered the trajectory of fossil fuel consumption globally. Ember documents that following the second conflict in 1979, annual growth in fossil fuel use reversed considerably, and global oil demand per capita peaked. Oil’s share of global electricity generation fell from roughly 25% in 1973 to about 10% decades later and has plummeted to just 2% today.

The impact of today’s crisis may prove to be even more transformative, as the scale of the disruption is unprecedented and the potential for future disruptions may have increased. The emergence of low-cost drones and precision missiles may have lowered the threshold for actions that create supply shocks, making energy security an even more critical priority. Asia, which has long been expected to be a major growth engine for future LNG and crude oil exports from Canada, today has some of the strongest incentives to build out domestic energy systems—including renewable power—to reduce reliance on imported fuels. Similar realizations are also being reached across Europe.

Unlike the 1970s, countries today have more choice in energy options and are significantly less dependent on fossil fuels to keep their economies running. Renewable energy technologies such as wind and solar are widely available, cost-competitive, and readily deployable at scale within most power systems. As the economics of renewables become increasingly competitive, they may be difficult to reverse—even after the conflict eases. While some barriers to full adoption exist, global investment in renewables is running at double that of oil, gas, and coal combined; thus it is not unreasonable to expect that material breakthroughs will continue to emerge in the long run. An accelerated global shift from fossil fuels to renewables in response to the current energy crisis could end up limiting long-term growth prospects for oil and gas exporters, including Canada.

Conclusion

Current strength in LNG and oil markets driven by the conflict may obscure underlying and potential deterioration in long-term market fundamentals. When taking similar historical conflicts into consideration, the current market conditions may prove transitory, while structural demand risks and accelerating energy transition dynamics remain intact. Elevated market conditions are threatened in the shorter term by a potential return to normalcy, the market glut waiting at the other end of the conflict, and the increasingly competitive economics of renewable energy. Fast-tracking capital-intensive fossil fuel infrastructure in response to market disruptions tied to international conflict is not a reliable long-term energy strategy. While the crisis may strengthen Canada’s standing in global energy markets, it may also intensify efforts to reduce reliance on internationally traded fuels altogether, limiting long term demand growth for fossil fuel exports.

Related Research