Cambodia’s LNG plans face unanswered questions that are critical for energy security and cost

Key Findings

Cambodia's plan to integrate a 900-megawatt (MW) liquefied natural gas (LNG)-fired power plant into its electricity system is a risky proposal. Other countries in the region, reliant on LNG imports, have seen global market disruptions impair energy security and affordability.

As a potential new market entrant with limited bargaining power, uncertain gas requirements, and a lower demand profile, Cambodia could struggle to access affordable LNG supplies. Operating one 900MW LNG-fired power plant at baseload levels for a year could cost as much as US$722 million (KHR2.95 trillion) for the fuel alone.

LNG is seen as the only way to provide grid reliability. However, with wind and solar making up a mere 5% of Cambodia’s power mix, there is ample opportunity for renewables to expand without jeopardizing grid operations.

Cambodia’s energy objectives include maintaining an affordable power supply and generating 70% of the country’s power from renewable sources by 2030, up from 50% in 2023. Cambodia must scale its LNG aspirations so that LNG-fired power does not derail the achievement of these goals.

In October 2024, Cambodian conglomerate Royal Group broke ground on a 900-megawatt (MW) electricity generation project in Koh Kong province’s coastal Botum Sakor district. If completed on schedule by 2027, the project would become the country’s largest operational power plant and its first to run on natural gas.

However, Cambodia does not produce its own natural gas, so the project will also require infrastructure to import the fuel in cold, liquid form and reheat it for combustion in the power plant. Some analysts expect thatliquefied natural gas (LNG) could play a massive role in Cambodia’s energy future. This is a risky proposition. In recent years, other countries in the region that rely on imported LNG have struggled to maintain energy security and affordability due to global market disruptions and skyrocketing costs.

Therefore, Cambodia’s foray into LNG markets will require careful strategic foresight and planning to reduce energy costs, improve reliability, and support economic growth. However, numerous questions remain regarding LNG costs and procurement, the role of LNG-fired electricity in the country’s power mix, and the use of potentially cheaper alternatives. Without clear answers, Cambodia’s economy could be highly exposed to the high costs and volatility of global LNG markets.

How will Cambodia buy LNG and what will it cost?

New buyers like Cambodia typically acquire LNG in two ways. LNG can be purchased from spot markets or through multi-year contracts, which establish volumes and pricing methods over the contract term. Each option entails various risks for energy security and cost that are critical for Cambodia.

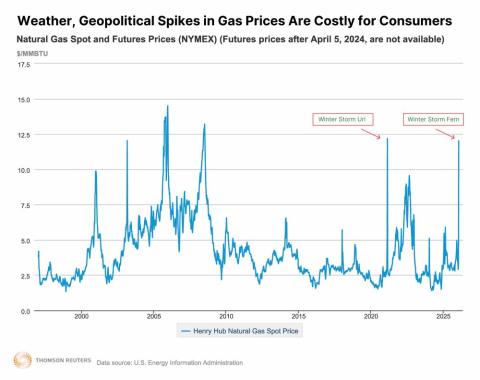

Buying from the spot market means Cambodia could import shipments whenever needed rather than committing to set contracts. The country would pay the prevalent global market price at the time of the purchase. This can be highly risky during periods of volatile prices. Since 2020, spot prices have fluctuated between US$1 per million British thermal units (MMBtu) and US$100/MMBtu – roughly US$4 million to US$375 million per shipment of a typical 72,000 tonne LNG cargo.

Contracts alleviate these concerns by setting a pricing formula, typically tied to a percentage of the global oil price. This reduces price volatility, narrowing the cost range of LNG cargo deliveries. However, contracts also stipulate rigid “take-or-pay” terms, meaning Cambodia must either “take” the LNG or “pay” a penalty if the LNG is not needed. Since LNG’s role in Cambodia’s energy system is still uncertain, the country could be obligated to pay significant penalties.

Importantly, LNG is likely to be expensive under both approaches. LNG prices under spot and contract arrangements are currently two to three times coal prices. A recent study by the Institute for Energy Economics and Financial Analysis (IEEFA) estimates that at current prices, operating one 900MW LNG-fired power plant at baseload levels could cost as much as US$722 million (KHR2.95 trillion) for the fuel alone. This exceeds Cambodia’s entire coal import bill in 2022.

As a potential new market entrant with limited bargaining power, uncertain gas requirements, and a lower demand profile, Cambodia could pay a premium to current prices and struggle to access affordable LNG supplies.

In 2022, the Russian invasion of Ukraine caused global LNG prices to skyrocket as wealthy European and Northeast Asian buyers outbid emerging markets for limited supplies. Pakistan and Bangladesh, for example, were often unable to afford LNG shipments, resulting in fuel shortages and power outages that devastated key economic sectors. In 2024, prices remain well above historical levels, and both countries are still struggling to finance their ballooning LNG import bills. Consequently, Pakistan announced it would no longer build LNG-fired power plants.

What impact will LNG have on electricity prices?

Integrating costly LNG into Cambodia’s power mix will have knock-on effects on electricity costs, hindering government efforts to reduce electricity rates.

At current spot market prices, LNG-fired electricity could cost more than five times that of recent solar projects in the country and about double the rate of current coal and hydro contracts. For example, IEEFA estimates that LNG-fired electricity could cost US$0.17 per kilowatt-hour (kWh) at current LNG prices. Meanwhile, Cambodia has attracted solar energy projects at just US$0.026/kWh.

LNG fuel prices would likely have to fall below US$4.8/MMBtu to compete with coal and renewables. However, global prices have rarely fallen this low because most producers require a selling price of US$8/MMBtu or more to service debt and earn a return. This means that LNG prices are unlikely to fall to competitive levels for the Cambodian power sector.

Other Asian countries, such as Vietnam and the Philippines, are grappling with the impact of uncompetitive LNG imports on electricity costs. This is slowing down LNG-to-power development and putting higher pressure on end-user tariffs.

Cambodian consumers already pay among the highest rates for power in Asia. With LNG prices unlikely to compete with renewables or baseload coal plants and the government prioritizing electricity affordability, the role of LNG plants in the power mix remains uncertain.

What is the alternative?

Cambodia needs to properly assess whether a baseload LNG-to-power project is necessary to achieve its energy objectives. These include maintaining an affordable power supply and generating 70% of the country’s power from renewable sources by 2030, up from 50% in 2023.

The current impetus for LNG development appears to be driven by the concern that wind and solar resources do not provide uninterrupted, dispatchable power. LNG is seen as an energy security necessity, the only way to provide grid reliability as electricity demand rises and the power grid relies on more renewable resources this decade en route to its decarbonization.

However, with wind projects fledging and solar making up a mere 5% of Cambodia’s power mix, there is ample opportunity for both wind and solar to expand without jeopardizing grid operations. Countries can typically integrate up to 15% of the electricity mix with wind and solar generation with only minor changes to the grid.

Moreover, achieving the 70% renewables target would limit the use of LNG-fired power plants, making it difficult to commit to long-term LNG contracts. The uncertain role of LNG power plants in Cambodia’s power mix will make it challenging to scale infrastructure and contracts in a way that ensures both energy security and affordability.

Cambodia must scale its LNG project aspirations so that LNG-fired power does not put the government’s energy goals out of reach. This would allow actors to pursue LNG contract procurement and infrastructure plans that are best suited to deliver its energy objectives.

This commentary first appeared in Dialogue Earth.