Some stock analysts say the problems afflicting ExxonMobil are cyclical, which would mean that a spike or increase in oil prices are on the horizon and that the company will move back into the black across the board when that happens.

But the fact is that a rebound in oil prices is unlikely. Independent assessments—from a diverse group that includes the U.S. Energy Information Administration, the World Bank, the International Monetary Fund and the Economist—agree on this point. None of their outlooks show a dramatic, long-term rise anytime soon. International imbalances in supply and demand, new political alliances and low-carbon initiatives will foster a realignment of global energy priorities and will mitigate against a dramatic, long term rise in oil prices.

Granted, oil prices may go up somewhat, the level, type, and basis for the increases are likely to be insufficient to keep ExxonMobil’s investments afloat or to spur a new round of investment or increases in share distribution.

Granted, oil prices may go up somewhat, the level, type, and basis for the increases are likely to be insufficient to keep ExxonMobil’s investments afloat or to spur a new round of investment or increases in share distribution.

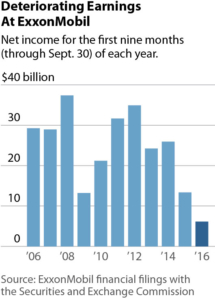

ExxonMobil’s third-quarter earnings, released on Oct. 28, showed a continued downward financial spiral. Although the company reported a modest improvement in profits as compared to the second quarter (in line with the modest increase in the price of oil during that time), overall profits were 54 percent below the first nine months of 2015, which itself was a very poor year for the company.

In its third-quarter filing to the SEC on Nov. 3, ExxonMobil reported a 20 percent drop in revenues compared to the first three quarters of 2015. This suggests the company may be on track to produce $215 billion in revenue in 2016, down from its peak of $486 billion in 2011.

Over the past decade, the company’s revenues are down, profits are down, capital expenditures are down, long-term debt is up, and distribution to shareholders is down a troubling set of metrics we explored last month in our report, “Red Flags on ExxonMobil.”

In a response it issued to IEEFA’s report, ExxonMobil implicitly acknowledged that it can no longer rely on the old business cycles, where rising oil prices produced more cash for new investments:

“ExxonMobil believes that its operations will exhibit strong performance over the long term as a result of disciplined investment, cost management, asset enhancement programs and application of advanced technology.”

The operative phrase here, “will exhibit strong performance,” is a signal to investors that they can expect better in the future, but the company—to pull that off—is going to have to figure out a new way forward. We noted in our report that ExxonMobil’s recent cost cutting, capex reductions and new technology advances have not kept pace with the rapid decline in oil prices.

The modest rise between the second and third quarters of this year (from the low $40s to the high $40s) was well below what is needed to stimulate new investment.

ExxonMobil has now reported almost two full years of diminished profitability, a rare phenomenon for the company. And it has been lagging the S&P 500 Index for 10 quarters—after having led it for decades.

The company—indeed the entire oil industry itself—is destined to be smaller in the future. And although it may be able to manage modest growth even as it endures prolonged financial stress, its long-term prospects are diminished significantly.

Investors should ask management tough questions, as recommended in our report, about how the company will produce returns for shareholders.

In its third-quarter earnings release, the company said it will likely de-book some of its reserves in Canada, and telegraphed the potential for a more generalized asset impairment when it concludes its fourth-quarter evaluations.

We’ll delve further into these balance-sheet issues in a commentary tomorrow.

Tom Sanzillo is IEEFA’s director of finance.

RELATED POSTS:

IEEFA Report: Red Flags on ExxonMobil: Core Financials Show a Company in Decline

Related Content