While the International Energy Agency this week is promoting the line that Southeast Asia will save the global seaborne coal industry, the big-picture data suggests otherwise.

A more reality-based outlook than what IEA published on Monday would consider the likely impact of what’s happening in the three largest coal-import nations: China, Japan and India. Together, the big three accounted for 51 percent of all globally traded thermal coal in 2014. Southeast Asia, by comparison, accounted for just 6 percent.

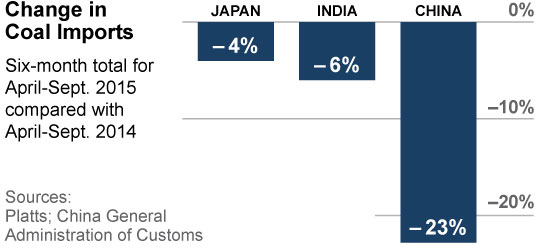

Change in Coal Imports – Japan, India, China

We don’t think Southeast Asia will save global coal markets. Our view is rooted in different approach than what IEA adheres to—we read actual markets, actual production levels, actual shipments and actual prices. IEA, by contrast, runs on assumptions that can be useful for establishing consensus forecasts but often miss the many-faceted interplay between markets and public policy.

THIS IS A TIME OF TREMENDOUS CHANGE IN ENERGY MARKETS AND IN THE COAL INDUSTRY, and while old-school modeling exercises like what IEA produces have a certain academic rationale, they are increasingly removed from prices, profits, policy and people—the real forces shaping the new energy economy.

A few reality-check data points:

- On China, Reuters notes that coal imports for the month of September were down 16 percent year over year year and that from January to September 2015, coal imports were down 29.8 percent year over year (open that window wider and look at April 2014 through September of this year, and the trend is just as apparent, with the China General Administration of Customs reporting a year-over-year drop of 23 percent). China’s economy is transitioning toward a less energy-intensive service/consumer-oriented demand profile, as seen in the 11 percent year-over-year growth in the Golden Week 2015 Chinese retail sales figures. Regardless of how you parse it, the data suggests a bloodbath, especially given that coal imports into China fell 11 percent in 2014 and that coal imports into China peaked in 2013.

- On Japan, Platts reports this week that coal imports for utilities from April 2014 through September of this year were down 4 percent year over year, marking a faster rate of decline than the corresponding 2.3 year-over-year drop in electricity consumption. The data suggests thermal coal imports into Japan peaked in 2014.

- On India, thermal coal imports for utilities in September 2015 were down 14 percent year over year, and down 6 percent in the first six months of this year (this data is only for roughly a 40 percent subset of total Indian thermal imports, as reported by the Central Electricity Authority of India). These numbers follow six years of 20-30 percent year-over-year growth in coal imports, suggesting that mid-2015 was a turning point in India’s coal-import appetite. Coal India this week also reported domestic coal dispatches for the month of September up 15 percent year over year. Record domestic production growth plus a surge in renewable investment (Bridge to India puts traffic in the solar-project pipeline in India at 12 gigawatts, up from virtually zero at the start of 2015) in fact means reduced coal-import demand.

So the actual data from the three largest coal-import markets, in short, tells a rather different story from what IEA is putting forth. Peak import coal has happened in China and Japan and it will happen this year in India.

Total global thermal coal demand peaked in 2013, declined marginally in 2014 and has declined at an accelerating rate this year. Structural changes and electricity-market transitions are unfolding fast. Coal mines, more and more, are stranded assets in the making.

Tim Buckley is IEEFA’s director of energy finance studies, Australasia. Tom Sanzillo is IEEFA’s finance director.