Key Findings

Despite featuring prominently in the narrative surrounding AEMO’s 2024 Integrated System Plan, gas is forecast to play a reduced role in power generation for the National Electricity Market, and there are risks and uncertainties surrounding increased investment in gas.

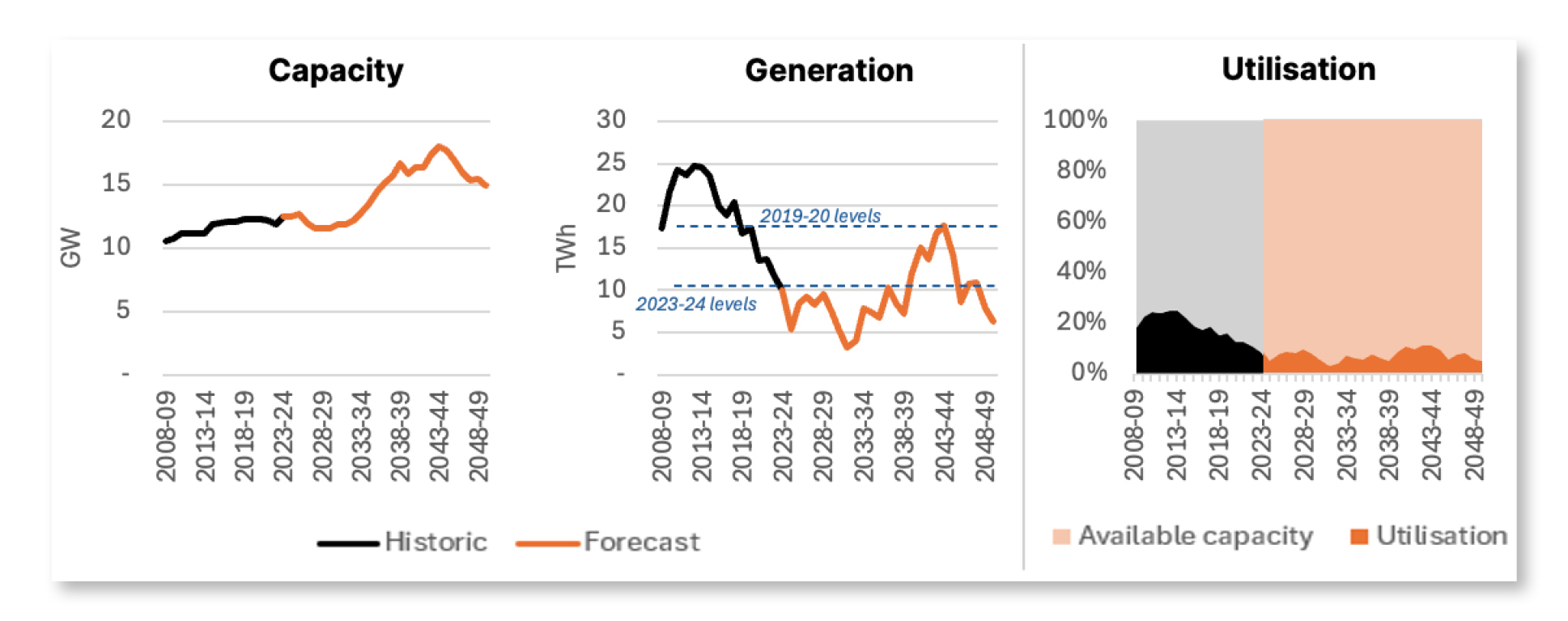

The need for gas power generation is expected to be below historic levels, and very small compared with the expansion of renewable generation and storage. As the role of gas narrows to focus on ‘peaking’ services, generators are expected to operate only 7% of the time on average.

Gas is an expensive form of generation, and low utilisation rates will likely require gas generators to increase their prices even further. Meanwhile, batteries are seeing rapid cost reductions and are outcompeting gas in many jurisdictions.

AEMO’s forecasts are based on rapidly evolving assumptions, and carry inherent uncertainties, including the future frequency of ‘low VRE’ [variable renewable energy] events. This could further erode the profitability of gas generators.

In the Australian Energy Market Operator (AEMO)’s 2024 edition of its Integrated System Plan (ISP), the role of gas received significantly more attention than it has in previous releases.

The 2024 ISP was released with the tagline: “Renewable energy connected by transmission and distribution, firmed with storage and backed up by gas-powered generation is the lowest-cost way to supply electricity to homes and businesses as Australia transitions to a net zero economy.”

In this tagline, AEMO is referring to the fact that, although renewable energy is the least-cost form of new generation, ‘firming’ technologies are expected to be necessary to support renewables at times when wind and solar power output is low. This version of the ISP identified a role for gas power generation (GPG) to fulfill part of this need.

The ISP is a key planning document that lays out a pathway for the future of Australia’s National Electricity Market (NEM). Some stakeholders have interpreted the 2024 ISP as affirming “the urgent need for investment in new gas supply and infrastructure”.

This briefing note seeks to unpack the analysis underlying the ISP, to understand just how much gas will be needed in the future grid, and the investments needed to support it.

Gas power generation forecasts in AEMO’s 2024 ISP

The briefing note identifies a considerable range of risks and uncertainties surrounding AEMO’s forecasts. As the niche for gas power generation steadily narrows to focus on ‘peaking’ services, its utilisation is expected to fall and become increasingly weather-dependent. A key driver of utilisation of gas generation is the frequency and severity of periods with low wind and solar output. However, AEMO has acknowledged that these events are highly uncertain and difficult to forecast.

The note also identifies broader risks around over-investment in new gas supplies in the east coast market, if overall demand were to fall faster than AEMO’s forecasts. On winter days infrastructure limits may occasionally constrain the amount of gas available to gas generators in southern regions, but AEMO’s analysis shows that the use of back-up liquid fuel – or in the longer term, alternatives such as biofuels – is likely to be a more economical option than expanding pipeline capacity.

READ THE FULL BRIEFING NOTE HERE

Related Content