Sustained high prices may accelerate downward pressures on Asian LNG demand, clouding long-term industry outlooks

15 August (IEEFA): The global liquefied natural gas (LNG) industry has pinned its long-term hopes for growth on emerging markets in China, South Asia, and Southeast Asia. But a new IEEFA report finds that sustained high prices over the past year have eroded the economic case for LNG and hurt LNG sales in key Asian markets.

“Less than one year into higher prices, LNG markets are already seeing a major realignment of demand away from Asia. Should price spikes and volatility continue over the next several years, downward pressures on Asian LNG demand may accelerate, permanently impairing long-term regional demand growth,” said Sam Reynolds, author of the report. “Financiers and investors in new LNG projects must take note.”

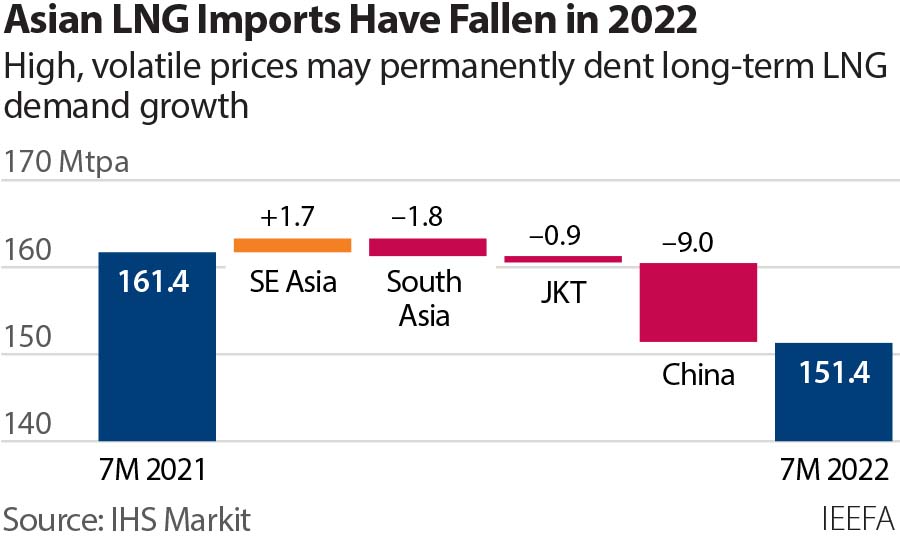

LNG sales in Asia through July 2022 have fallen more than 6% compared to last year. In China and India, two of the largest potential LNG growth markets, LNG imports have fallen 20% and 10% year-over-year, respectively.

Demand in Asia could fall further as competition for limited supplies intensifies during the winter heating season. Multiple countries have withdrawn or been forced out of LNG spot markets altogether.

Elevated LNG prices bite into demand forecasts

High, volatile LNG prices are unlikely to settle for several years due to myriad factors. For example, the threat of continued Russian cuts to European piped gas, outages at LNG liquefaction facilities, and increasingly unpredictable weather events due to climate change could all constrict an already tight global market.

“Exorbitant prices and unreliability of supply are undermining industry-driven narratives that LNG is a viable ‘bridge fuel’ from coal,” said Reynolds. “Continuous demand growth at persistently high prices will likely prove fiscally unsustainable for emerging markets.”

As a result, numerous forecasting agencies have begun cutting estimates for Asia’s medium-term LNG demand growth. The International Energy Agency’s (IEA) latest outlook for gas demand growth in Asia through 2025 is 65 billion cubic meters (Bcm) less than its forecast last year. Bloomberg New Energy Finance has cut its expectation for LNG demand in South and Southeast Asia in 2025 by 37 Bcm.

Other mainstream forecasting agencies, such as Rystad Energy and the Independent Commodity Intelligence Services, have also expressed the risk of permanent reductions in emerging Asia’s LNG demand.

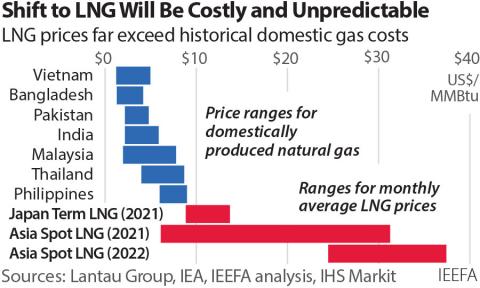

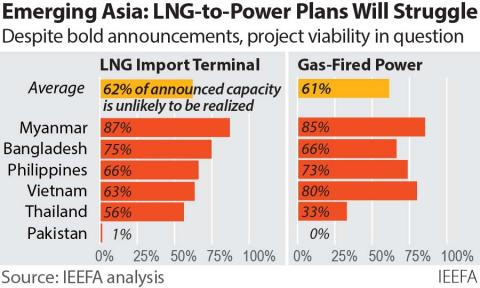

Unaffordability of LNG and fuel supply insecurity may cause new import terminals to go unused, potentially costing billions of dollars in stranded assets. As long as unaffordable LNG prices and procurement challenges continue, US$96.7 billion dollars of proposed LNG-related infrastructure projects in Pakistan, Bangladesh, Vietnam, and the Philippines will face a heightened risk of underutilization or cancellation.

Efforts to reduce LNG dependence are accelerating

Many analysts expect Asian demand growth to simply recover to pre-crisis levels once prices settle and new supplies come online. But countries are rapidly developing alternative energy sources that could permanently dent regional LNG demand growth.

In China, LNG demand is coming under significant price pressure from new coal and renewables. The country is on pace to deploy 120 gigawatts (GW) of new renewables capacity this year, 40% higher than the previous five-year average. Buyers will reportedly avoid spot market purchases for the rest of the year, while pipeline gas imports were up 60% through April. Moreover, plans to expand pipeline capacity from Russia and Turkmenistan by 100 Bcm per year could reduce the need for LNG imports.

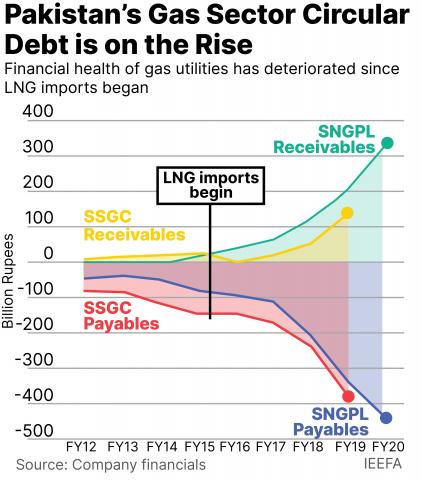

South Asian countries have tried to maintain LNG import levels when possible, but financially unsustainable prices have led to severe fuel shortages and load shedding. Pakistan and Bangladesh have begun to explore domestic alternatives, including renewables and indigenous gas resources. An uptick in India’s domestic gas production and ambitious renewables targets means that, according to the IEA, annual LNG demand may not surpass 2020 levels through 2025.

In prospective LNG markets like Vietnam and the Philippines, LNG import projects are facing delays, while policymakers are increasingly emphasizing the need to reduce dependence on imported fuels. Thailand has faced a perfect storm: high LNG prices, combined with declining domestic gas production and pipeline imports, are causing some of the highest gas and power prices ever.

In Northeast Asia, the current LNG market environment has accelerated pre-existing decarbonization plans, breathing new life into renewables deployment and controversial discussions surrounding nuclear power. A renewed focus on energy self-sufficiency in Japan and the election of a pro-nuclear administration in South Korea are expected to have permanent repercussions on LNG demand.

“These shifts away from LNG are in their early stages. Should high prices and volatility persist for the next several years, the narrative around LNG as a viable, affordable transition fuel is likely to erode further,” said Reynolds. “Ultimately, high prices now may undermine profits and exacerbate stranded asset risks for LNG projects targeting completion later this decade.”

Read the report: The Economic Case for LNG in Asia is Crumbling

Media contact:

US: Susan Torres ([email protected]), +1 (908) 331-1472

Asia: Alex Yu ([email protected]), +852 9614-1051