Middle Arm Gas and Petrochemicals Hub: Combination of problems makes it unprofitable for business and a red flag to the public

Download Full Report

View Press Release

Key Findings

A plan to boost the Northern Territory’s economy with a concentration of new industries at the Middle Arm Gas and Petrochemicals Hub is flawed.

Given the obstacles to the development of the Middle Arm Gas and Petrochemicals Hub, it is highly likely that a significant burden of the project’s costs will fall on those least able to afford it—Australian taxpayers.

The ambitious plan relies on too many unproven assumptions, including the viability of carbon capture and storage; a robust market for liquefied natural gas; partners who will agree to develop resources in the isolated region and significant infusions of public dollars over a long period that could upset Australia’s fiscal balances.

The territory’s plan to extract natural gas from the Beetaloo basin is based on using hydraulic fracturing (fracking), which has proved to be a poor investment in other countries. The plan also relies on the controversial Barossa gas field.

Spearheaded by the Department of Industry, Planning and Logistics (DIPL), the Northern Territory’s industrial development plan promises a thriving network of industries including natural gas extraction, liquefied natural gas (LNG) exports, carbon capture and sequestration, mineral refining, advanced manufacturing, and the production of ammonia, urea, methane, ethylene and hydrogen. The goal is to generate an abundant supply of natural gas from the Beetaloo and Barossa gas fields to support LNG exports, domestic electricity needs, and an array of new (and existing) agrichemical and petrochemical companies.

The Middle Arm Sustainable Development Precinct plan, which promises new industry and substantial infrastructure investment, is flawed. Its market assumptions are overly optimistic; infrastructure needs will stress federal and local budgets; and the plan is misaligned with global efforts to curtail greenhouse gas emissions. The plans for exports, new technologies and new industries face a series of market, infrastructure and technological challenges. Because the Northern Territory is undeveloped, it would take a level of support that the combined balance sheets of Australia’s federal government and several corporations cannot afford. A new supply of natural gas is not enough of a financial incentive to offset the costs of new agrichemical and petrochemical facilities, new roads, pipelines, ports, water systems, power plants, housing, schools and community facilities. The remote location puts the hub far away from businesses that can manufacture and service new product lines. The very real possibility exists that the plan will create fiscal imbalances between the states and territories, as well as budget pressures within the Northern Territory.

The business model underlying the plan is not viable. The development of the gas field relies on hydraulic fracturing (fracking) technology created in the United States. Fracking has been an economic failure even as it has produced an increase in oil and gas production. Investors have lost billions. It has also created water and land controversies resulting in civil penalties and criminal prosecutions. The companies leading the way in the Northern Territory – Santos, Tamboran and Empire Energy – each have strengths but are poorly positioned to take on these financial and logistical risks.

The plan also runs against Australia’s climate strategies. The nation is committed to curbing its carbon emissions. This plan adds a new natural gas field, contradicting international plans to lower the world’s greenhouse gas emissions. It also contradicts the many local and national climate solutions in which Australia – its people and businesses – is now engaged.

This report fundamentally looks at the financial risks to the redevelopment plan. Taken alone, any one of these risks is substantial but could be manageable. Cumulatively, these risks create a daunting set of problems that lower the potential for companies and investors to profit, and constitute a series of red flags to Australia’s leadership. The infrastructure needs are vast, and the policy changes must be executed with a level of co-operation and co-ordination that would be extraordinary. Most of the business assumptions in the plan rest on either failed or unproven technological innovations. After rushing headlong with policy and public dollars, the NT government faces a risk that the markets will fail to produce the jobs and profits required to make the plan a success. The failure will be seen in the destruction of public promises and investor dollars.

This report provides an introductory overview that will be supplemented in the months ahead by more specific analytical treatment of critical issues and discussions of new information that emerges.

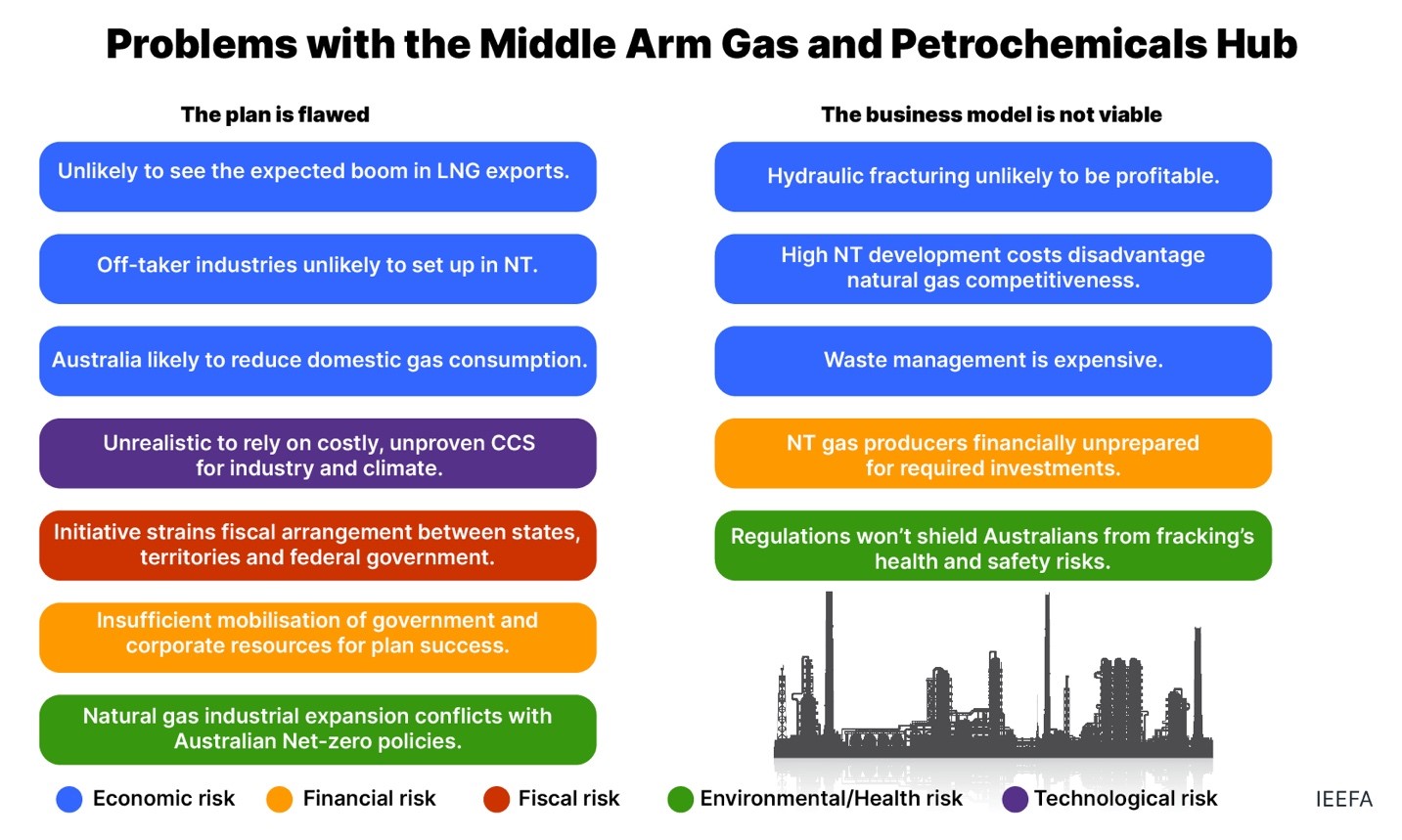

The risks we have identified are based on market, fiscal, governmental, and health and safety factors, viewed through a financial lens. They are organised around two basic headings: 1) The plan is flawed, and 2) The business model is not viable.

The Plan Is Flawed

- Risk 1: The robust market for LNG exports anticipated in the plan is unlikely to materialise. Markets are changing, and Australia will be less able to compete on cost as its traditional customer base shrinks. This will undermine the financial success of the Beetaloo and Barossa gas investments.

- Risk 2: The off-taker industries anticipated to become partners (hydrogen, ammonia, urea, methane, carbon capture, advanced manufacturing and mineral processing) are unlikely to locate in the Northern Territory.

- Risk 3: Relying on carbon capture and sequestration (CCS) – a costly and unproven technology – to become a thriving industry and climate solution is unrealistic.

- Risk 4: Australia’s domestic gas demand is likely to slow, and perhaps may even decline.

- Risk 5: DIPL’s Middle Arm plan would strain the existing fiscal arrangement between the states and territories and the federal government in ways that are unsustainable.

- Risk 6: Government and corporate resources are not likely to be mobilised at sufficient levels and over the period necessary for the plan to be successful. Policy changes to address significant infrastructure issues in education, environment, transportation, water management and electricity regulation are too numerous to be practical.

- Risk 7: Natural gas industrial expansion conflicts with Australia’s net-zero policy.

The Business Model Is Not Viable

- Risk 8: The use of hydraulic fracturing is not likely to be profitable. Fracking has destroyed investor value over the long term in the U.S. With a weak business sector at its core, the off-taker industries do not have a stable partner to produce a reliable, cost-competitive supply of natural gas.

- Risk 9: Leading gas producers in the Northern Territory are financially unprepared to address the significant investments needed to explore, drill, distribute and support infrastructure to create a hub for LNG, agricultural and petrochemical development.

- Risk 10: Development costs in the Northern Territory for natural gas are high. Australia and the Northern Territory are at a competitive disadvantage against robust competition globally, and within Australia, for the gas market.

- Risk 11: Regulations are not likely to protect the Australian public against the health and safety risks of fracking. In the U.S., public health and safety mandates failed, and pollution of drinking water led to civil and criminal actions.

- Risk 12: The management of solid waste and wastewater is likely to be costly.

The fatal flaw of the Northern Territory development plan is its dependence on fossil fuels. Once the world’s leading source of energy and financial growth, Australia now faces historically unprecedented competition. The plan is ambitious to the point of being prohibitively speculative. The risks will fall on the shoulders of the affected communities – who cannot afford to bear it – and Australia’s taxpayers.

Related Content